How accountant use Drone technology to achieve their task depends on the sectors or schedule of activities. In addition, drones are unmanned aerial vehicles (UAVs) that can fly remotely.

The global drone market predicts to increase from $26.3 billion in 2021 to $41.3 billion by 2026. Also, in 2020, both US and the UK used drones to deliver drugs during the COVID-19 pandemic (Appelbaum et al., 2020).

Drone technology has proven helpful in war zones and intelligence gathering and also in a civilian role, such as:

Countries that make use of drone technology and require permission for all aerial drones through regulation.

Moreover, the regulation addresses different types of civil drone operations and their respective levels of risk as stated by European Union Aviation Safety Agency

In Germany, there are limited zones outside protected areas with high urban density or people conglomerations.

Also, all EU Member States, including Norway and Liechtenstein.

Switzerland and Iceland are also expected to apply this regulation soon.

In United States for example, they used drone technology for their operation(Ovaska-Few, 2017).

In 2013, Poland passed a law allowing the commercial operation of drones, which led to the birth of Drone Powered Solutions.

South Africa that has entirely established drone regulations in place which was carefully integrated into existing aviation law.

Lastly, in Australia, Rio Tinto who has its facility in a remote area planned in 2016 to start using drone to monitor mine sites including the staff.

Companies that have used drone in their workplace and in others area of operations.

It was recorded that PwC completed its first stock count audit using drone technology. With the assistance of a drone, they were able to capture images at a coal reserve in South Wales and used them to measure the volume of the coal, based on the measurement of volume.

Amazon and Google are already testing ways to deliver packages with drones.

Facebook has started using drones to provide internet connections in remote locations.

Basin Electric’s utilization of drones has enhanced efficiency and safety while concurrently reducing costs.

Furthermore, Ford Motor Company filed a patent to start the use of drones for dead bateries. The patent was filed on 3rd February, 2017 and circulated on March 8th, 2022, and assigned serial number 11271420.

How Accountant Use Drone Technology to the Accounting Profession.

Source: Naira Technology

With the help of drone technology, however, accountants can now complete their work in a shorter amount of time. Technological advancements have significantly changed the accounting and auditing profession in recent years.

In 2017, the emergence of drone technology has revolutionized the accounting and auditing profession. Drones have opened up new possibilities for accountants to perform their tasks more efficiently and effectively.

Emerging technologies like AI, blockchain, big data, the IOT, and drone technology have revolutionized accounting profession (Qasim et al., 21).

For example, accounting and audit firms that work with clients in mining and inventory can utilize drone technology to take thousands of pictures and measurements of a site (Ovaska-Few,2017).

Also, this can aid in accurate assessments of holdings, making tasks like physically measuring coal a thing of the past. An estimated volume can be obtained in less time with just a two-meter GPS Tracking pole.

What are the Benefits of Drone Technology to the Accounting and Audit profession.

Perform physical inventory: Drone could recount inventory if required-data feed repeatedly into audit app that re-performs the process. Using drones to automate livestock inventory count reduced count time from 681 hours to 19 hours (Qasim et al., 21).

Time-efficiency and effectiveness: Drone devices help to improve and increase effectiveness and efficiency in the accounting and auditing profession.

Accuracy: Produce accurate data that can be relevant for future forecast and planning. It depend on how accountant use drone technology to collect insight into the condition of assets. This is faster, cheaper, safer and more accurate than traditional methods (Johnson, 2022).

Save Cost: Drones may save money for accounting clients, who can use them for stock takes, mapping, safety monitoring and to inspect bridges and building.

Productivity: It can enhance productivity

Also, Reduce the risk of injury: he benefit in health and safety as the need for someone to climb over the coal pile are removed.

Speed: Helps speed up some business and accounting processes.

Monitoring strategies . Help monitor staff, operation and some dangerous zone. For instance, drones can assist the firm or staff to take account area difficult to reach.

Storage of Long-term data: Moreover, drone methods allow for storage of long-term data. This is useful to account for physical factors (like weather, light conditions and geomorphology of the beach) for more spatio-temporal analysis.

Automate and accelerate repetitive accounting tasks (Qasim et al., 21).

The technology produces massive amounts of data that require interpretation and translation into meaningful information for informed business decisions.

Also, as accountants keeping up to date with new technologies and understanding their potential to enhance efficiency and effectiveness is essential. Developing the necessary skills to interpret and present data will enable them to add value to their employers. Since the drones technology are control by expert . However, drones are prone to making mistakes just like any other technology, which is why one can exempt them from errors.

Furthermore, competent accountants who are conversant with latest technology, play a crucial role in helping companies thrive and maintain a competitive advantage. It is imperative that organizations have skilled accountants on their team to achieve these goals.

Implications of How Accountant use drone Technology to the Accountants and Auditors

Be part of the at least 95% that will accept this new technology if they must prepare for the future.

Develop a new skill that is all-encompassing for them to be relevant every time and drive the development of accounting profession.

For companies to successfully transform, there will be a great demand for individuals with fundamental knowledge and expertise. For instance, such individuals must possess the necessary skills and understanding to support the company’s transformational goals.

Also, become a consultant in the field to remain relevant and being in change of the world where we live by data.

Become a strategic thinker.

Apply professional judgement whenever is necessary and obtain a better results

Establish Drone-focused department that enable accounting firms to handle all matter related to drone.

Check the impact of drones on client’s business operations.

Lastly, it is vital for every accountant or auditors to be familiar with the present drone regulations in their countries.

Conclusion

In this article, the writer examined how accountant use drone technology and to achieve their work on daily basis. Similarly, drones can improve the accuracy and efficiency of audits. However, how they can use it to collect data and perform inspections in hard-to-reach areas.

Consequently, the article highlighted the potential impact of commercial drones on the accounting profession, with predictions that this technology will revolutionize traditional accounting procedures (Ovaska-Few, 2017). Accounting professionals and academics need to recognize the significance of drone technology and patronize the suppliers as it is here to stay. In addion, the sooner we adapt to this technology and use it to their advantage, the better. Accountants and auditors are condition to embrace this new technology and see it as an improvement to their jobs instead of threat.

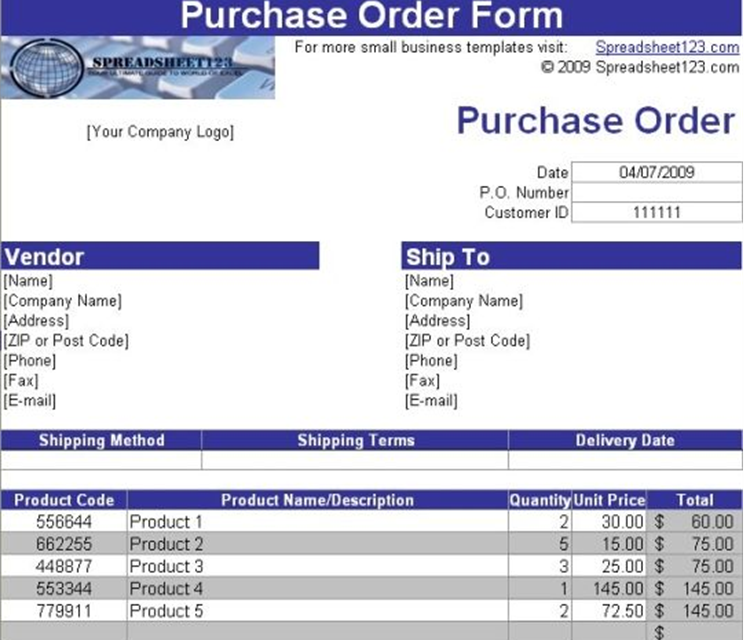

Purchase orders (PO) are essential for an accountant to help achieve financial goals and is one of the key Source Documents in Accounting. The buyer sends these orders to the vendor or sellers or suppliers, outlining what they expect for the order and when it should arrive. In contrast, a sales order generated by the supplier and sent to the buyer. Additionally, the supplier generates an invoice to show the buyer how much they owe for the purchased goods.

Benefits of Purchase Orders (PO)

Controlling the procurement of products and services from external suppliers is easier with purchase order.

The inventory process is more accessible with the help of PO. Once the supplier receives the PO, they will retrieve the items listed in the PO from their inventory.

The Purchase Order acts as a legal document that helps prevent future transaction disputes.

It prevent duplicate orders by keeping track of order and from whom, which can be challenging when a company decides to scale its business.

Overall, a well-organized purchase order system helps simplify the inventory and shipping process by keeping track of incoming orders.

The process of initiating a purchase order should begin with:

When a buyer needs goods, they start by creating a purchase requisition. This document helps to keep track of the items ordered and is sent to the purchasing department within the company. It also helps the company keep track of expenses. The acountant can only create purchase order once an authorized manager has approved the purchase requisition.

Once the buyer has confirmed the goods they wish to purchase, they will initiate a PO. This document will include the date of the order, FOB shipping information, discount terms, buyer and seller names, a description of the goods under process, item number, price, quantity, and the PO number as shown in the attachment.

The seller can accept or reject a PO with all the transaction and buyer’s requirements. If the seller agrees with the PO, it becomes a legally binding contract.

Keeping a record of the purchase order is crucial for buyers. The demand remains active until the company receive all or part of the goods.

Goods Receive Note (GRN) is issue after successful delivery from suppliers. Each order has an assigned unique number associated with the Purchase order number. The accountant can use this number to ensure that the goods received match those ordered and listed on the GRN.

Before company accountant make payment, they will verify that the Purchase order number matches the invoice. This ensures that the charges to pay by the buyer are the correct amount for the goods before processing the payment.

Businesses today operate within a vast network of service partnerships, making their environment fast-changing and complex. As a result, accounting has begun utilising IT for collecting and storing data and developing management information technology services to handle heavy calculations. The cloud computing has become the solution of choice for this need. However, despite significant advances in computing capabilities, the low usage of installed systems has contributed to the “productivity paradox.” To avoid this, organizations must adopt cloud-based business models to gain a competitive advantage and achieve growth. This essay aims to critically analyze cloud computing’s significance in accounting and its impact on accounting systems by exploring various authors’ perspectives on the subject. Specifically, it will focus on general considerations of cloud accounting, its features, and the effect of cloud computing in accounting.

General Consideration of Cloud Computing

Definitions of cloud computing:

NIST definition

The earlier version of the cloud computing definition was developed by The National Institute of Standards and Technology of the United States Department of Commerce in November 2009. They had gone through several versions while consulting other professional bodies before arriving at a more acceptable definition. In July 2009, on the NIST cloud computing website, that earlier version was posted. It was published In January 2011 for public observation as public draft SP 800-145. The National Institute of Standards and Technology of the United States Department of Commerce defined cloud computing as:

“model for enabling ubiquitous, convenient, on-demand network access to a shared pool of configurable computing resources (e.g., networks, servers, storage, applications, and services) that can be rapidly provisioned and released with minimal management effort or service provider interaction. This cloud model is composed of five essential characteristics, three service models, and four deployment models’’. The NIST definition outlines five vital characteristics of cloud computing:

On-demand self-service,

Broad network access,

Resource pooling,

Rapid elasticity or expansion, and

Measured service.

It also outlines three “service models”

Software,

Platform and

Infrastructure

Some “deployment models” like private, public and hybrid classify ways to deliver cloud services to Stakeholders.

Plummer, D. C., et al. (2008), defines cloud computing as:

“a style of computing where massively scalable IT-enabled capabilities are delivered ‘as a service’ to external customers using Internet technologies.”

If we take a detailed look at that definition, what we discover is a set of mutually supportive concepts. First, is the concept of delivering services (results is contrary to components)? Implementation is irrelevant in as much as the results of the implementation can be defined and evaluated in the area of service with correlated service-level conditions. The payment in this concept is based on usage and not on physical assets. The payment can be subsidised, for instance, in advertising or customers can pay directly. Second, this concept is that of large scalability. Economies of scale contract the cost of the service. Inherent in the concept of scalability is flexibility and reduced level of impediment to entry for customers. Third, delivery via Internet technologies indicate that definite standards that are made open in a universal basis are used. Finally, these services are provided to several external customers, influencing shared resources to boost the economies of scale.

Scalability vs. Elasticity

The issue of scalability is frequently deliberated as regards to the cloud. Plummer, D. C., et al. (2008), definition acknowledges large scalability but the concept of elasticity is not specifically mentioned. Scale is a facet of efficiency and the capacity to support the needs of customer. The concept of elasticity is greatly connected to the ability to render those needs in a considerable scale at will. In term of elasticity, a system should sustain the ability to scale both in an upward direction (for instance, large number of users) and in a downward direction (for instance, single user) without discomposing economics of the business ideal connected with the cloud service. Ideal business-class systems are scaled in the upward direction, but the cost of operating that scaled complex for single or multiple users would be restricted on the basis of cost of running and maintaining the context. Howbeit, Google, eBay or Zoho as a global-class provider have a model that is not predominantly based on the cost of the support and operations or maintenance and software licenses, but influences revenue and other systems to support their existence. This means that the number of users and what they are doing, while extremely relevant, can be detached from the operating economics of the cloud provider.

In addition with the problem of elasticity is the question of whether something that does not support large scalability should be regarded as cloud or not. The definition does not signify to be an opening that dictates admittance in the cloud model (Plummer, D. C., et al. 2008). Howbeit, it is determined as a procedure for the relative “cloudiness” of a specific solution. This entails that large scale is not the highest characteristic for cloud-computing providers it is a pointer of where they are in the relative breadth of their cloud solutions. As cloud computing continues to evolve, very small number of large IT providers will surface aiding large workloads, massive data manipulation and common purpose services. Their distinction will basically be economies of scale. Howbeit, there will also be a long part of midsize and even relatively small providers contrasting on front-edge and special-purpose technologies, advancing on continued IT innovation and maintaining price pressure on even the largest providers.

Modifying How Services Are Delivered

For the past 15 years, a sustaining trend as regard industrialization of IT has increase in universality (Plummer, D. C., et al. 2008). IT services provided via hardware, software are becoming repeatable and usable by a large number of customers and service providers. This is decentralized because of commoditization and standardization of technologies, virtualization and the increase of service oriented software architectures, and, ultimately, the impressive development in vogue/use of the Internet and the Web. These things collectively comprise the basis of a discontinuity that result to a new opportunity to form the relationship between those who adopt IT services and those who market them. What the discontinuity indicates is that the capacity to provide specialized services in IT can now be combined with the capacity to provide those services in an industrialized and pervasive way. The actuality of that incrimination is that users of IT-related services can concentrate on what the services provide to them instead of how the services are executed or hosted. Utility companies sell power to subscribers and telephone companies sell voice and data services, similarly, IT services such as network security management, data center hosting or even departmental billing can now be easily provided as a legal service. The purchasing decision then changes from purchasing products that authorise the delivery of some function (like billing) as regard dealing with other person to provide those functions. Unquestionably, this is not strange, but it portrays a different model from the license based, on-premises models that have been prevalent in the IT industry for long. The names giving to this type of operation have trended at different times. Utility computing, software as a service (SaaS) and application service providers (ASPs) do have their position in the pantheon of industrialized delivery models. Howbeit, none has amassed widespread recognition as the focal theme for how IT-related services can be provided globally.

The fundamental elements following cloud computing are not new. According to Plummer, D. C., et al., (2008) this definition can be criticized by querying what delivering “as a service” means, but the focal idea of the definition is that service delivery is when a provider authorise a business relationship between itself and a consumer to deliver in a small or large capacity. This definition is not based on physical performance but as regard results. Hence, the interruption that was brought about by this phenomenon is not one of technology implementation but one of relationships and interfaces. The connection between the user and the provider of an IT service provides the framework of the service to be delivered. So the question of which service to purchase or how to pay for it is answered based on price, performance, quality of service, trust, disaster recovery, security guarantees or even reputation, but not entirely on implementation. Just like the concept of the Internet, the concept of a cloud, will profit from the awareness that just one public cloud exists. Customers that are members of a company are served through the public incorporation of this cloud. The concept of multiple public clouds indicates that a user must select its preferred cloud to use. Also, given that the technologies for delivering IT services generally must be the same for everybody in a public context, the mindset that one cloud will be distinct from another loses potency. Services are just services eventually, and while a customer may decide to use Google services vs. eBay services, one can access those services through the same mechanisms regardless of vendor. Just as in the early days of the Internet, the cloud definition is better defined as it includes a public cloud (external, like the Internet) and private clouds (internal, like intranets). Private clouds will be adopted by companies that do not want the general public to have access to their IT-related services but do want to take advantage of the delivery and acquisition model the cloud enables.

According to Plummer, D. C., et al. (2008) this has several implications:

The cloud is more than just SaaS, instead everything as a service (SaaS) would be a more appropriate designation. Via the cloud, one can access services that are basically hardware based where the software is an essential component of the delivery, not a specialised value proposition in itself. An example of this is storage as a service. SaaS is an ADM and can be provided via the cloud just as any other service can. It would have been limited to say that SaaS and the cloud were the same.

The Internet and probably the Web are essential for the existence today of the cloud but are not entirely definitive of it. There must be an intentional delivery of service to integrate cloud computing. (In time to come, some other globally distributed network may replace the Internet in this magnitude to support cloud computing.)

Internal clouds can exist via Internet/Web technologies but must also contain the intentional ADM of SaaS to in-house customers and private partners. This is what differentiated these internal clouds from the one public cloud.

Zaigham, A. Muhammad, M. & Arslan, J., (2022) definition of cloud computing

The authors were brief and concise in their definition. They defined cloud computing as:

“the delivery of hosted services over the internet as a whole”.

If we take a close look at this definition, we discover that the authors’ emphasis is more on delivering the various types of cloud computing services. Infrastructure as a service, platform as a service, and software as a service are the three main types of cloud computing services (SaaS). A cloud can be either private or public, base on your preferences. Any person with internet access can purchase services from a public cloud. It is a private network or data center that delivers hosted services to a restricted number of people with definite access and permission settings. Cloud computing, whether private or public, target to make computing resources and IT services seamlessly accessible and scalable.The hardware and software components needed to implement a cloud computing model perfectly consist cloud infrastructure. For instance, cloud computing can be called utility or on-demand computing, respectively (Zaigham et.al., 2022).

Cloud Storage

Inclusive in their work is cloud storage. Zaigham et al. (2022) defined it as “a model of networked enterprise storage that uses virtualized pools of storage hosted by third parties to store data”. Hosting company can lease storage spaces to those who need data to be hosted by them. Customer-specific storage pools are provided by data centre operators so that customers can store files or data items. Physically, the resource can be expanded across multiple servers and locations around the world. Base on the hosting companies and the applications that use cloud storage, data security is a matter of choice.

Web-based content management systems, cloud desktop storage, cloud storage gateways, as well as other API-based applications can all make use of cloud storage services to their maximum potential (Zaigham, A. Muhammad, M. & Arslan, J., 2022), citing (Armbrust, 2010).

Icloud

iCloud was launched on October 12, 2011 by Apple Inc. It is a cloud computing and storage service. An estimated 850 million people used the service in 2018, up from 782 million in 2016 (Zaigham, A. Muhammad, M. & Arslan, J., 2022). About 4,444 Users can store data such as documents, photos, and music on iCloud servers that can be downloaded to iOS, macOS or Windows devices. One can also send and receive data with other users and keep track of your Apple devices in case they’re stolen or lost.

Drive in the cloud by Google

Google Drive was release in 2012. Users have gained access to save files to the cloud (on Google’s servers), sync files across devices, and share files. Additionally as regards the web-based interface, Google Drive also delivers desktop and mobile apps for Windows, macOS, and Android and iOS devices with offline functionality. One of the most essential features of the Google Docs Editors office suite is its capacity to grant multiple people to edit the same document, spreadsheet or presentation at once. Google Drive is where all of your Google Docs files are saved after you are done working on them (Armbrust, 2010).

OneDrive for Microsoft

Microsoft OneDrive (formally SkyDrive), provide file hosting and synchronization, which is incorporated into the online version of Office. Files and personal data, such as Windows settings and BitLocker recovery keys, can be stored in the cloud with OneDrive. This was first introduced in August 2007 and is now available on Android, Windows Phone and iOS mobile devices, Windows PCs and macOS as well as Xbox 360 (Grossman, 2009).

Dropbox

Some features of Dopbox include loud storage, file synchronization, a personal cloud and client software. The company is based in San Francisco, California. It was founded in 2007 by Drew Houston and Arash Ferdowsi founded Dropbox as a start-up company with funding from the Y Combinator startup accelerator.

Amazon’s third-generation streaming media player

Web service interface-based object storage service Amazon S3, or Amazon Simple Storage Service, is delivered by Amazon Web Services. The same scalable storage infrastructure that Amazon.com depend on to power its global e-commerce network powers Amazon S3 (Zaigham, A. Muhammad, M. & Arslan, J., 2022).

Figure 1: Cloud computing modelSource: Google.com

Typical Features of Cloud Computing

Infrastructure-as-a-Service (IaaS) is an on-demand service, the basic computing infrastructure of servers and network equipment are covered by the IaaS, and consequently a platform can be established to develop and execute applications.

Platform-as-a-Service (PaaS) is an on-demand service which provides the computing platform. It incorporates the operating system and databases, and consequently applications can be developed and deployed.

Software-as-a-Service (SaaS) means that one or more applications, including the computational resources to run them, are provided for use on demand as a service. It is frequently used to access desktop apps through a web browser.

Business-Process-as-a-Service (BPaaS) is the delivery of business process outsourcing services that are sourced from the Cloud and constructed for multi-tenancy.

Figure 1: Different Cloud service modelSource: Google.com

Cloud Accounting

This section defines the cloud accounting phenomenon, and outlines the various benefits of cloud computing in accounting. Boban and Stipić, (2020) as citing Christauskas and Miseviciene, (2012) define a cloud based accounting system as a way to manage business accounts completely online and attained as a service, on-demand, acting like accounting software installed on users’ computers, but performed on servers and accessible by users via their web browsers.

Benefits of Cloud Computing In Accounting

Boban and Stipić, (2020) outlined befits of cloud computing as follows:

Access: Employees, partners and clients can access and update information from any location, no need to return to work.

Lower costs: Lower costs for hardware and software, network management, and IT in general. Since the applications are in the cloud, with few large programs that the computer’s memory Occupy, users can more performance from their PC.

Security: Most cloud application servers offer a high level of security. Network-based systems are equally or even more secure and in most cases have better internal controls when compared to similar local software.

Business suitability: It is very easy to add new software. The server upgrades applications more frequently than small businesses can afford. In terms of expansion businesses can quickly access the resources they need when necessary.

Easy administration: Only network access is required to access accounting. All users have the same version of the software allowing real-time data backup.

Compliance: Compliance with a variety of requirements is paramount, which include accounting standards and internal controls.

Some cloud accounting software.

Sharma, S., (2020) outlined cloud accounting software as follow:

Sage 100cloud: this cloud accounting software was provided by Sage Group. It is more suitable for small and medium companies that require automating their operations. Some of the functions are as follows:

▪ Accounting and Finance

▪ Inventory and warehouse management

▪ Purchasing and Vendor management

▪ Light assembly and production

▪ Automated rental management (a kind of inventory automation)

QuickBooks Online: It is the cloud version of QuickBooks accounting software. It is cloud base and does not need an offline installation on the desktop. Some of the functions are as follows:

▪ Manage sales and income

▪ Keep track of bills and expenses

▪ Gain key reporting insights to the business

▪ Profit and loss report

▪ Balance sheet report

▪ Statement of cash flows

▪ Run payroll

Xero: It is a SaaS based accounting software developed by Xero. IIt was founded in New Zealand in 2006. It also supplies a mobile version of its software to enhance access and operate accounts from anywhere. It provides the following functions:

▪ Invoicing

▪ Managing inventory

▪ Payroll access across 50 countries

▪ Bank connections and reconciliations

▪ Cash management dashboard

ZapAccounting Software: The purpose of zap accounting software is to manage book keeping records for individuals, sole proprietorship firms. ItZap is designed in Google Sheets. It is double-entry Book Keeping Software Solution. The Zap accounting software is an Open-source and cloud based. Some of the functions are as follows:

▪ Charts of Accounts, Ledgers and Reporting

▪ Balance Sheet

▪ Cash management

▪ Deposit preparation

▪ Year-end financial summary

Cloud Accounting – Advantages & Disadvantages

All technology has some benefits and defects within themselves. Cloud accounting is not an exception. The advantages and disadvantages of cloud accounting are discussed below as follows:

Advantages:

Ease-of- Access: Cloud Accounting enables seamless access to the company’s account. Xero, one of the SaaS providers, also develop software for mobile phones. This makes possible for report to be accessed from anywhere. Data can be updated by users from any location and anytime! As a result, cloud accounting has made a lot easier managing and accessing accounting information.

Better Security: Cloud accounting softwares are accessed from various locations by users hence the software providers offer multiple security levels for full protection of the data of a company. Thus, by utilising cloud accounting, users can depend on the security made available by the host. In SaaS, all maintenance is done by the vendor, which includes security. Hence, the security of the data is guaranteed for the user.

Platform-agnostic: Cloud Accounting is completely platform agnostic, for instance, it can be accessed in any kind of platform. Even if a user is using Windows or Mac OS, it does not prevent its access, as it can support in any type of web browser. It can also be access with a google chrome via android devices.

Auto backups: Automatic data backup of the user is guaranteed by the vendor of cloud or SaaS. Hence, the issue of saving of data is minimized while utilising cloud accounting softwares.

No capital expenditure: Since it is cloud based no extra charges are requires except monthly subscription charges to use cloud base accounting softwares. Hence, no capital expenditure is needed for installation of softwares.

Disadvantages:

Internet access: One can access cloud accounting only when there is an active Internet connection. Without internet connection, user cannot have access to their vendors. Hence, this becomes one of the biggest disadvantages.

Security breach: Cloud accounting gives access via the Internet. Thus, it becomes risky as someone may have access to the data unauthorised.

Conclusion/Recommendation

This essay has focused on the relevance of cloud computing in accounting. The advantage of using information technology in accounting is irrefutable, but accountants must be acquainted with the new possibilities and benefits of cloud accounting. Enhancements in technology result to the rapid development and improvement of accounting information systems. Most accountant are not familiar with the benefits of cloud storage, while younger people exhibit more confidence and a sense of security as regard to cloud accounting and accountants working in bigger companies (Boban & Stipić, 2020).

Hence, it is suggested that the accounting system Steps in this direction, accounting and security systems Audit in compliance with the design and enhancement of new technologies, accounting and financial reporting with the rapid changes in the world keeps the business generated. Cloud accounting is more and more being developed and utilized, and accountants need to adjust to these changes. (Mohammadi, S. & Mohammadi, A., 2014).

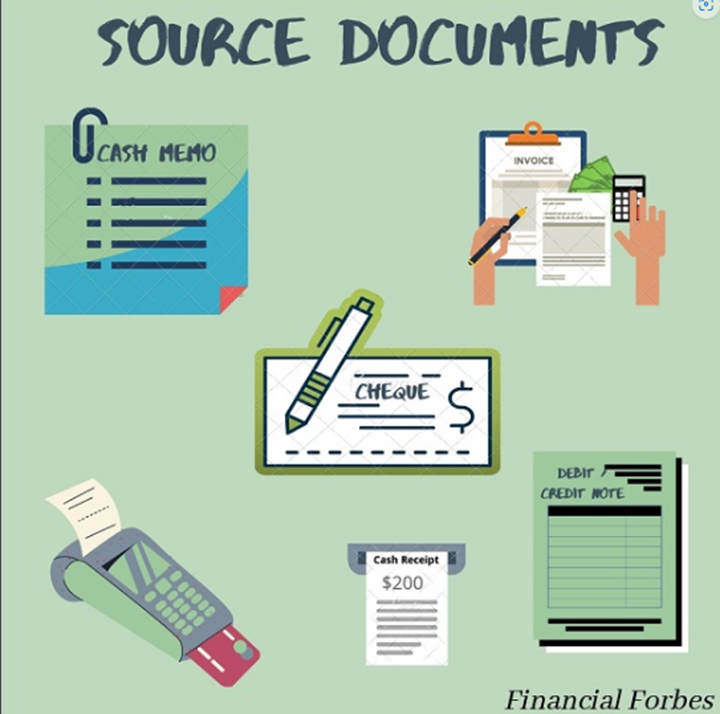

Top 35 Source Documents in Accounting are relevant to help accountant to help accountant in their job. Also, it is a document that serves as proof of transactions that is available in apps that provide such services.

Top 35 Source Documents in Accounting stated below:

The buyer sends this to the vendor. They will then outline exactly what the order should contain and when it should arrive.

2. Sales Invoice

This is a process for managing account receivables. When the seller gives out goods, they will provide a document containing all relevant sale details.

3. Purchase Invoice

This is made for account payables. The seller will enter this as sales invoice while the buyer will enter it as purchase invoice.

4. Debit Note

This is evidence of reduction in purchases and can be useful to support purchases return journal. Furthermore, in customer books, debit note will reduce how much they owe to the seller.

5. Credit Note

This is evidence of reduced sales and support sales return journal. In addition to supplier’s books, credit note reduces the amount owed by the customer.

6. Cheque

This is a special bank note that represents the cash paid by the customer.

7. Revenue receipt

This is used to record the receipt of cash which is a proof that the payment is made.

8. Cash register receipts

This is a business paper that listed the money coming in from customers.

9. Bank or Credit advice

They are debit or credit bank advice. Bank credit advice is bank documents informing the business of an increase made in the business’s bank account. Unlike bank debit advice that is opposite to bank credit advice.

10. Deposit slips

When one receives cheque or cash from customer, the seller will take it to the bank and present.

11. ATM cards

The production of receipt from ATM machine can serve as evidence that money has been taken from the bank account.

12. Bank statements

This is a summary of financial transactions that occurred at a certain institution during a specific time period. For example, a typical bank statement may show your deposits and withdrawals for a certain month.

13. Bill of exchange

This is an unconditional order in writing, addressed by one person to another, signed by the person giving it. It also require the person to whom it is addressed to pay on demand.

14. Payroll report

This can also refer to the list of employees of a business and the amount of compensation due to each of them.

15. Cancelled Cheque

This is a check that has been paid or cleared by the bank

16. Cheque Stubs

This is the check kept by the payee with information such as the check number, date, and amount.

17. Employee Timecard

This is a method for recording and tracking the amount of an employee’s time spent on each job

18. Board minutes or minutes of meetings

The secretary of the board usually takes minutes during meetings.

19. Goods Dispatched Note (GDN)

This a document of the company that lists the goods sent out to a customer. Without a doubt, the company will keep one record of goods dispatched notes.

20. Goods Issues Note (GIN)

This is a physical record of the movement of goods or materials from the warehouse or store to production department.

21. Stock take Records

This is also called stock counting. It is when you manually check and record all the inventory that your business currently has on hand

22. Stock Record

A Bin Card is a card indicating quantitative records of the receipts, issues and balances etc.

23. Goods Received Note (GRN)

This is source document that shows the goods that a business has received from a supplier.

24. Remittance advice

This source document can confirm the amount paid and shows discrepancies that can easily be investigated.

25. Insurance Endorsement Certificates

This is where one party will add the other party as an “additional insured” on their commercial liability insurance policy.

26. Point of Sales Summaries

This can be used to record a number of sales at a cash register.

27. Memorandum

Memo is a written document businesses use to communicate an announcement, policy changes, price increases or notification to take an action, such as attend a meeting, or change a current production procedure.

28. Computer-generated Receipts

This is the kind of receipts is to be generated by the computer.

29. Lease Agreement or Rental Agreement

Lease contracts are formal documents that identify the lessor, lessee, what’s being leased, whether it’s an asset or a property.

30. Sales Tax Returns

This is the taxpayer’s document of declaration. This will enable the taxpayer to furnish the transaction details during a tax period and deposits his Sales Tax liability.

31. Cash Register Tapes

This allowed one to keep a record of all customer transactions and/or provide them with a receipt.

32. Adjustment Notes

This are issued to customers due to damaged, returned or undelivered goods

33. Employee Pay Advice

This source document that can helped to provide written evidence concerning employee income.

34. Payroll Advice Report

This payroll reports helped small businesses understand payroll costs and summarize payroll data.

35. Evidence of Sale or Disposal of Assets

This is the removal of a long-term asset from the company’s accounting records.

Conclusion

Indeed, all these top 35 source documents in accounting are integrated in several apps that offer such accounting services. Moreover, this App made it possible to have all these source documents in one place to make the accountant job easier and simple.

Kindly add your own source documents to the Top 35 Source Documents in Accounting listed above. This will help us to update our records accordingly.

Watch several videos of how to prepare financial statements from source documents