Digital products are now one of the most scalable means to set up streams of income. This digital products ventures requires little capital to launch. It may not require physical inventory but only need freelancer to be creative in their writing. Moreover, they are also to use strategy and the right tools.

For me, my story in freelancing changed when I began to use ChatGPT not just as a writing assistant, but as a business partner.

With the strength of ChatGPT to produce content and ideas, I was able to transformed what take me a week into a repeatable system.

The outcome was pleasant to me over time, while I used ChatGPT as a helper. Because of my dependent on this tool, I was able to develop a high-selling digital products that I sell today on several platforms including eBooks, Online Training courses, Fiverr services, and Gumroad.

To benefit fully from this article, just keep reading to see how I achieved this feat and how you can too in your freelancing career.

1. I Packaged My skills

The first mindset I had was to ensure my product solves problems, not just to generate information for my audiences. You need take note, that people don’t pay for the information you share; they are interested in paying for the solutions you provide.

Every freelancers have knowledge in a different capacity, which others may be willing to pay for in dollar. Except the product is package properly, the audiences my not value it.

One way to make digital products create value and easy to buy is to ensure they are well packaged. Based on this understanding, I packaged some of my past work on accounting, data analytics and entrepreneurship into several formats.

Instead of starting from scratch, I enlisted ChatGPT as my business strategist to create contents with a solid foundation. These packages were developed to meet the specific needs of various social media platforms such as Medium, Facebook,Linkedin and with the right Call to action.

2. How ChatGPT Helped Me Achieve My Objectives.

I want to show you how ChatGPT becomes my creative tool for all my digital products:

• eBooks Creation: I will log on to my ChatGPT account and submit the right prompt to produce the content of my eBooks. Once that is done, I paraphrase and polish them to ensure they meet the aim of the eBooks. Then, I will publish them on the Amazon Kindle or Gumroad marketplace.

• Develop Online Courses: With the help of ChatGPT, I was able to get a lesson script that helped me deliver my classes. Then I will paraphrase it to remove the plagiarism so I can own it. This helps me capture video lessons faster with a good structured that makes the class flow well.

• Canva Templates. ChatGPT has helped me create several template such as banners, background pictures and so. The attachments from canvas are placed on my eBook covers and even on my thumbnails of my articles.

3. I Sell My Digital Products on a Platform That Works

It’s good to create a product, but employing the right distribution channel is even better. I have some of my digital products on Book Shop, Fiverr, Amazon Kindle and Gumroad. Am showing you this process because I want you to succeed also. You can also follow this if you are not there yet. These platforms already have a vast audience who are looking for a solution to their problems. As soon as I upload my new digital products, I start receiving sales. Even while I’m sleeping, I continue to receive sales.

4. The Key Lessons Anyone Can Learn

1. Start simple with the product. Since you are starting now, you may not be able to make your work excellent. But one thing I am sure of is that the products have solved someone’s problem.

2. Have a Specific Niche. It is better to focus on a specific niche than to target a product that serves “everyone”. A particular target will sell more than a general target.

3. Let ChatGPT become your helper. Although AI may accelerate the process, incorporating voice and expertise can make the product more authentic.

5. Conclusion

The emergence of ChatGPT has completely transformed how people utilise it to create digital products. Although I have discovered that ChatGPT alone is insufficient for delivering high-quality content, combining it with my unique expertise makes such content possible. If you’re struggling to develop your ideas, consider using ChatGPT as a helper, not a replacement.

Thanks for Reading

Check out my Gumroad for a custom business plan to kickstart your entrepreneurial journey.

Also, I’m available on Fiverrif you need an Excel financial model, forecasts, budget, or projections as an entrepreneur.

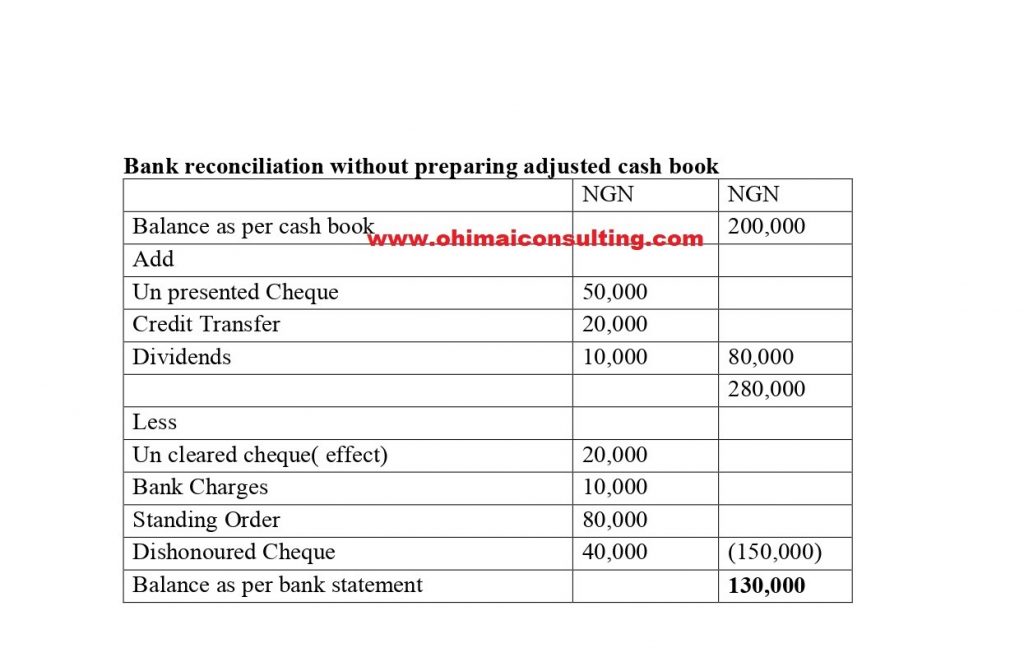

Bank Reconciliation Statement is the verification of all the entries in the bank statement with the bank book of the business. First, let understand what bank statement and cash book mean. A bank statement is the financial statement showing the details of all the transactions that the business had made through the bank account. Cash book is subsidiary book that record all cash transactions of receipts and payments.

Definition of Termssee when conducting bank reconciliation statement

Bank charges: This is money deducted from the entity account by the Bank to cover the cost of looking after the account.

Unpresented cheque: Is a cheque draw but not yet been presented at the drawer’s bank.

Uncleared cheque/ effect: Are bank cheque that passed through the clearing system but not yet cleared. It appears on the debit side of the cash book.

Dividend: This is direct dividend receive into bank account.

Standing order: This is an order to the bank to pay payee a fix sum of money at regular intervals from one’s bank account. e.g. paying rent, paying utility bill etc.

Advantage of standing order

It helps to save the repeated drawing cheque;

They help to save spending money on stationery and postage and

it is certain that payments are made on the due date.

Disadvantages of standing order

There are bank charges for such services.

Dishonoured Cheque as you conduct bank reconciliation statement:

This is cheque rejected by Bank. Top 11 of what will give rise to dishonoured cheque

When cheques are not signed or signed incorrectly (i.e. Irregular Signature)

No date shown on the cheque

When the cheque is mutilated

Insufficient funds in the account to meet the cheque

Alteration on the cheque without endorsement by the drawer’s signature.

Stale cheque: This is one that is more than 6months old. But is still valid after 6months if confirm from the drawer by the bank.

The death of the drawer

Non-existing account

Frozen account

Posted dated cheque: When the drawer of a cheque has insufficient funds to meet the amount of the cheque but expects to have sufficient in the future date the cheque in advance of the drawing date.

When government stop payment on the bank account.

Top 5 discrepancies between cash book and bank statements?

Pay-as-you-earn is a tax deducted from employee salary account. The remittance of this tax is on or before the 10th day of the month following the month in which salaries were paid. See relevant sections of the Personal Income Tax Act (PITA). (S.81 of Personal Income Tax Act Cap P8 LFN 2011). S. for details

Taxable Entitlement (Gross)

This is the total amount your employer pays their employee as salary, including all benefits arising from employment. Another name to call taxable entitlement is Gross Emoluments. These include wages, salaries, allowances including benefits in kind, gratuities, superannuation and any other incomes derived solely because of employment. Regardless, it is essential to note that all allowances are taxable except those reimbursements of employee expenses. However, if such reimbursements are carried out through the employee payslip, they must be subjected to tax in Nigeria. Such reimbursements include training costs, transport to attend training, etc.

Moreover, Section 33(2) of finance-act-2020 defined “gross income” as income from all sources, less non-taxable income, and tax-exempt items.

Table 1 showing the comparison of old PITA and Proposed PITA of an employee who earn N5,775,000 as gross salary.

TAX RELIEF (TAX ALLOWANCE)

This is amounts that can be deducted from a person’s annual income to reduce the amount on which tax is paid. Or the amount of youThese amounts can be deducted from a person’s annual income to reduce the tax paid. In other words, it is the amount of your income exempt from tax aside from other statutory deductions.

Maximum of Personal relief ₦ 800,000.00

Rent Relief of lower of N200,0000 or 20% of actual rent paid.

Table 2 shows that Tax relief of old and proposed method

Tax Exempt

The tax law provides certain payroll deductions as tax exempt or non-taxable deductions. Tax exempt amount has to be removed from Gross taxable Income (earnings) before applying the tax rules to determine tax. The following deductions are not Taxable (.i.e. Tax Exempts):

Union due is 2% of the basic salary.

Pension Deductions (employer 10% and employee 8% of Basic salary, transport and housing allowance).

National Housing Fund Deductions (Employee 2.5% of basic salary).

Life Assurance Payments (this is obtained from the employee life policy document and monthly premium payment receipt is sufficient evidence to earn the tax exempt. Section 33(3) of Finance Act 2020 added that any premium payment. stated that there shall be allowed a deduction of annual amount of any premium paid by the individual during the year preceding the year of assessment to an insurance company in respect of insurance on his life or the life of his spouse or of a contract for a deferred annuity on his own life or the life of his spouse (finance-act-2020). This is addition to the Act.

The National Health Insurance Scheme (Government 10% and employee 5% of basic salary) but employer 5% has not be implemented yet in the federal government MDAs due to Labour objections.

Gratuity.

Table 3 showing the tax exempts for both the old and proposed.

Table 3 shows same amount since the figures are based on same sources

Tax Table

After the relief allowance and tax exemptions have been granted, the income balance shall be taxed as specified in the tax table below. Moreover, the Nigerian Payroll tax table comes in annual gross bands in six rows. Each band has a percentage tax value attached to it. The tax table rates must be applied to the Net Taxable Income to get Tax Payable.

Tax table and Rates from November 2024 tax year (As amended)

First N800, 000 @ 0 per cent

Next N2,200, 000 @ 15 per cent

Next N9,000, 000 @ 18per cent

Next N13,000,000 @ 21 per cent

Next N25,000,000 @ 23 per cent

Above N50, 000,000 @ 25 per cent

Taxable Income (Net)

This is derived after deducting the following from Gross Taxable Income. Some are extracted from payslip.

Gross Entitlement,

Tax Exempts, and

Tax Relief (Tax Allowance).

Apply tax table to the net amount as stated above

Table 4 showing the tax band of the old and the proposed method

Residency Rule

Assuming the Senior Manager who stay in Rivers State but work in Abia State. By residency rule, an employee’s PAYE is payable to the tax authority of the state of his/her residence (Rivers State). It is therefore the duty of the employer to deduct and remit it to the tax authority where the employee is resident. However, if the employee is resident in Rivers State, the tax authority that is entitled to his PAYE is the Rivers State Board of Internal Revenue.

Usually, non-residents are not liable to pay taxes in Nigeria. However, an expatriate employee may be liable to tax in Nigeria if;

Penalty for Failure to Deduct PAYE

Section 74(1) of Personal Income Tax Act, 2011 states “ any person or body corporate who fails to deduct, or having deducted, fails to remit such deductions to the relevant tax authority within 30days from the date the amount was deducted or the time the duty to deduct arose, shall be liable to a penalty of an amount of 10% of the tax not deducted or remitted in addition to the amount of tax not deducted or remitted plus interest at the prevailing monetary policy rate of Central Bank of Nigeria.

Exemption of Minimum Wages Earners

Section 37 of Finance Act 2020 “provided that minimum tax under this section or as provided for under the Sixth Schedule to this Act shall not apply to a person in any year of assessment where such person earns the National Minimum Wage or less from an employment (finance-act-2020).

Books of Accounts

Section 12 of PITA 2011 stated that the keeping of bools of accounts is very important but if any taxable person fails or refuses to keep account, such a person shall be liable on conviction to a penalty of N50,000 for individuals and N500,000 for corporate entities.

Employer File Tax Returns on Behalf of Their Staff.

Every employer is to file annual forms on behalf of their employer called Form H1 and Form A. Also, form H1 is an annual employer’s tax return that shows the names, annual gross income and PAYE taxes of employees in the past tax year together with Form G. Meanwhile, Form G gives information of the annual PAYE paid and the corresponding receipts. The tie to fill Form H1 is on the 31 January of the following year. Therefore, Form A is an annual statement of individual income and claims for allowances and reliefs form. Moreover, the right time to submit is on the 31st of March of the current year.

Conclusion

As an employer, you are responsible for ensuring full compliance with the guidelines set forth by the relevant tax authority concerning calculating your employee’s PAYE (Pay As You Earn). This applies accurately choosing the amount of PAYE to be deducted from each employee’s salary based on their earnings and applicable tax rates.

Furthermore, your civic duty is to remit the PAYE amounts deducted from your employee’s wages to the relevant tax authority promptly and within the specified deadlines. This not only sustains government services but also helps in fulfilling your legal obligations as an employer. Additionally, you must pay any other taxes owed to the relevant tax authority on time to avoid penalties and ensure that your business remains in good standing. Maintaining correct records and staying informed concerning tax regulations will enable you uphold these responsibilities effectively.

Cooperative accounting is the applications of financial accounting principles, concepts and policies to cooperatives in order to ascertain its financial position, promote accountability, efficient management and ensure viable operations of co-operative financial resources.

In other words, the accounting system and bookkeeper accurately record and report the cooperative’s daily business transactions.

Furthermore, the cooperative law makes the keeping of proper sets of accounting records and the preparation of the final accounts compulsory for every registered cooperative society and sets of information that must be disclosed in the final account.

Moreover, the cash books and receipts are source documents, while income and expenditure accounts and balance sheets are final accounts.

ACCOUNTS AND RECORDS OF COOPERATIVE ACCOUNTING.

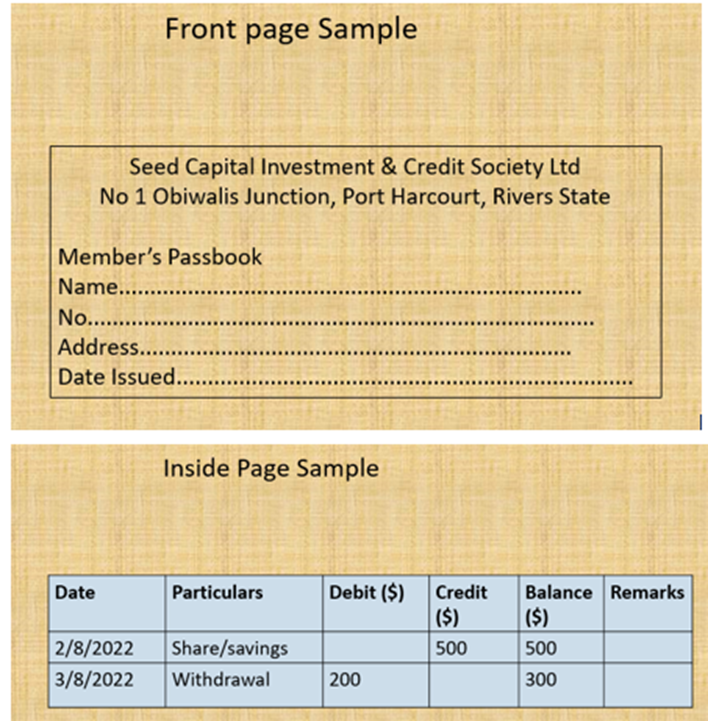

1.MEMBER’S PASSBOOK

Member’s passbook is opened for every member which serves as a personal account on which all transactions between a member and the society are recorded. Moreover, below is the front- and back-page sample of members passbook.

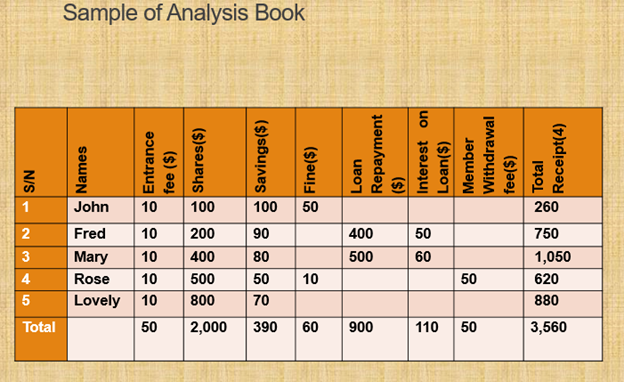

2. ANALYSIS BOOK

Also, analysis book is use for recording members’ contributions, loan disbursed and repayment, membership withdrawal, fine and other incomes on monthly basis. However, this book helps to analyse the transaction on a monthly basis. In addition, this book help cooperative to always spread open in front of members at any general meeting of the society.

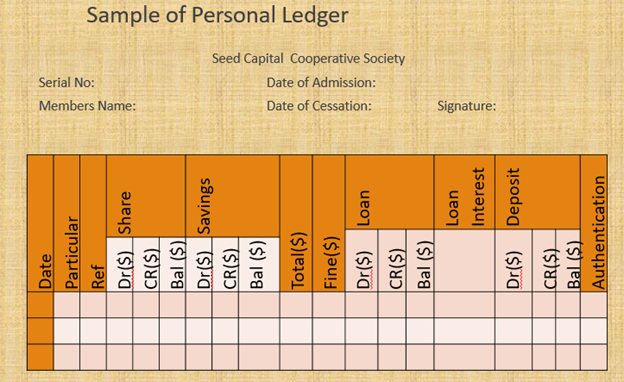

3. PERSONAL LEDGER

Personal ledger helps to record member’s contributions of shares, savings, deposits, withdrawals, loan and refunds. In addition, the entries into this book are from the individual’s entries in the analysis book which is also entered in the passbook. With proper recording of transaction, individual cash balances can be seen at a glance.

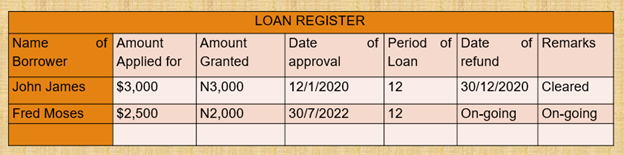

4. LOAN REGISTER

Obviously, Loan register is a source document containing information regarding all loans granted at any time. In addition, such information includes membership personal number; member identity number; committee meeting minute number; cheque number. Also, includes amount authorized and approved; amount applied for and granted; date of approval and refund; period of the loan.

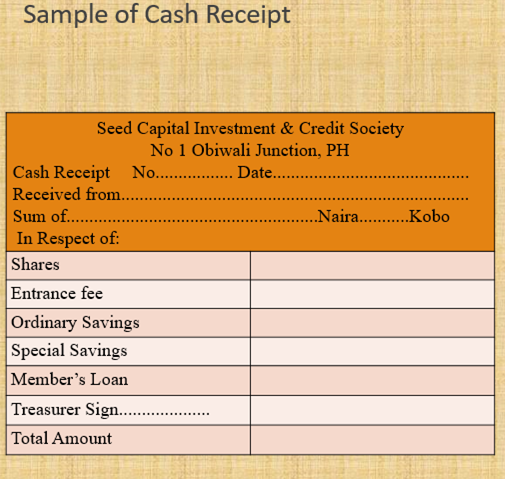

5. CASH RECEIPT

Also, cash receipt helps to record all money received in cash or in cheque. Also, it is financial transactions used as supporting evidence that money have been received on behalf of the society. Moreover, all receipts must be serially numbered and used in that order.

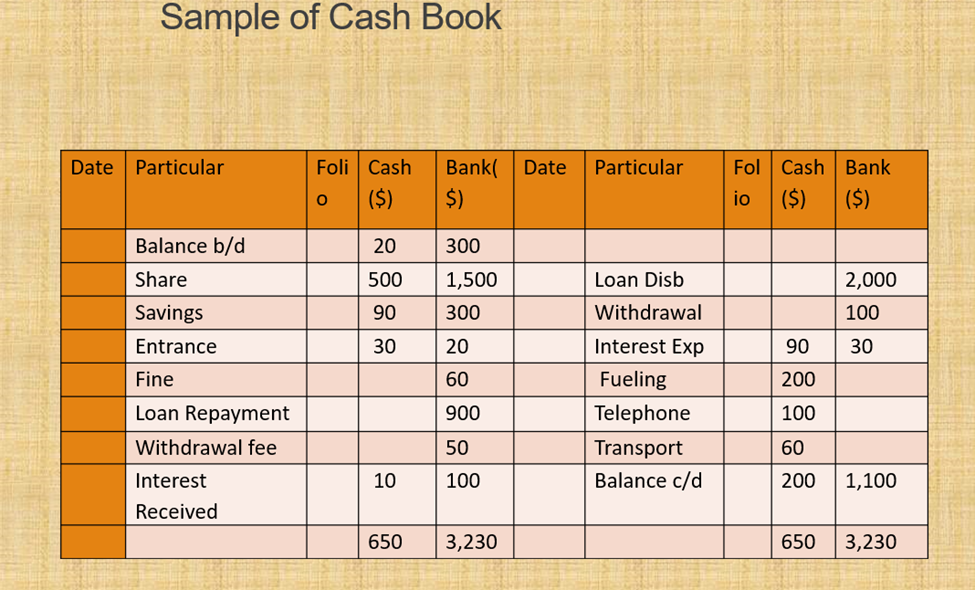

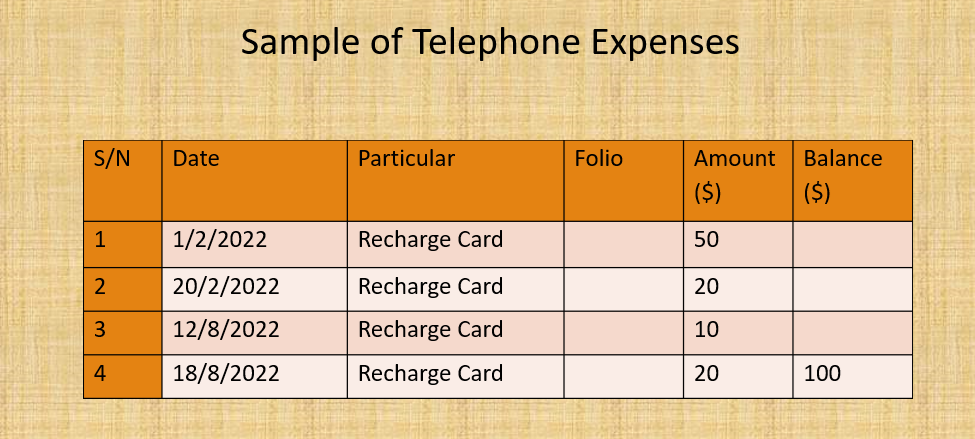

6. CASH BOOK

Moreover, a cash book is a financial record that shows all cash receipts and disbursements, including bank deposits, withdrawals, and balances.

7. INDIVIDUAL MEMBERS’ CONTRIBUTION

Additionally, in co-operative management, recording all transactions and producing financial statements on time is important. Clearly, these statements are the output based on each member’s contributions. By tabulating each member’s share and savings contributions in the individual contribution table, it’s easy to see the breakdown of each member’s contributions. Column A shows the fraction of each member’s share contribution, while column B shows their savings contribution.

8. GENERAL LEDGER

A general ledger is a cooperative financial record-keeping system that uses debit and credit account records. It can validate a trial balance, such as bank charges, telephone, and travelling expenses and asset account.

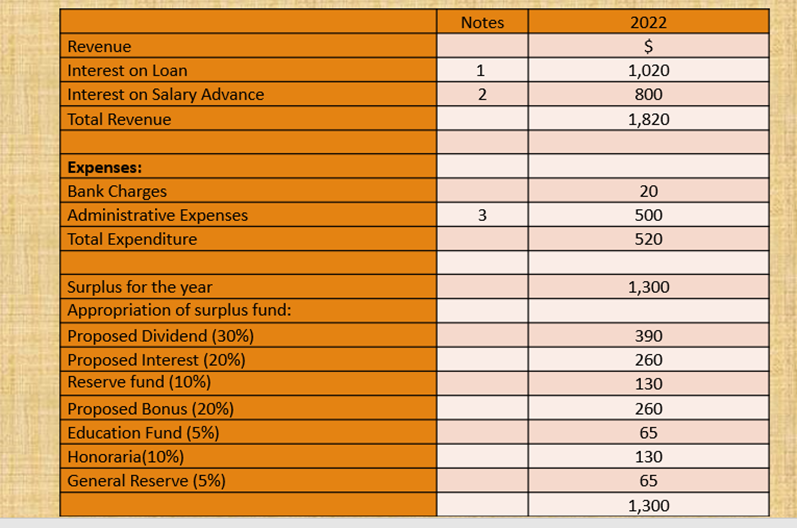

9. INCOME AND EXPENDITURE ACCOUNT

The Income and Expenditure Account summarises all the income and expenses incurred during the current accounting year. Its primary objective is to calculate the surplus or deficit. However, cooperatives only declare surplus or deficit, not profit or loss, since they are exempt from paying taxes.

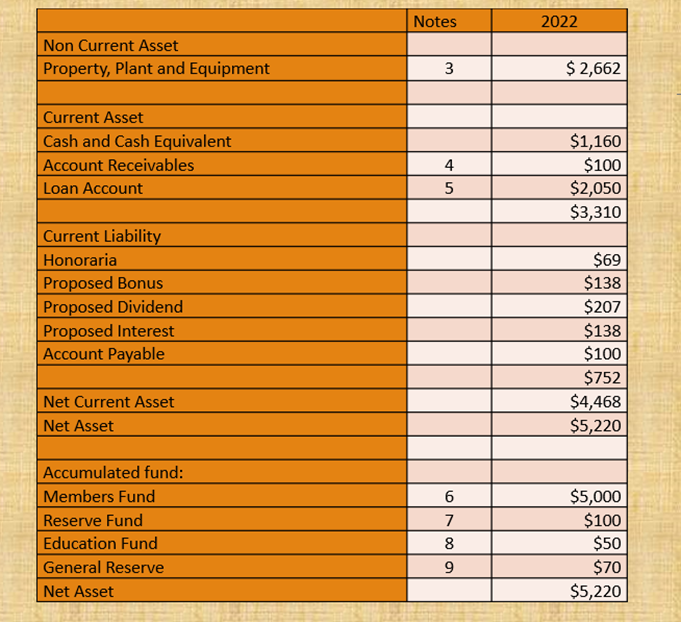

10. STATEMENT OF FINANCIAL POSITION

A balance sheet is a financial statement that shows a company’s assets, liabilities, and equity on a specific date. It summarises the business’s overall value at a particular time, like a snapshot.

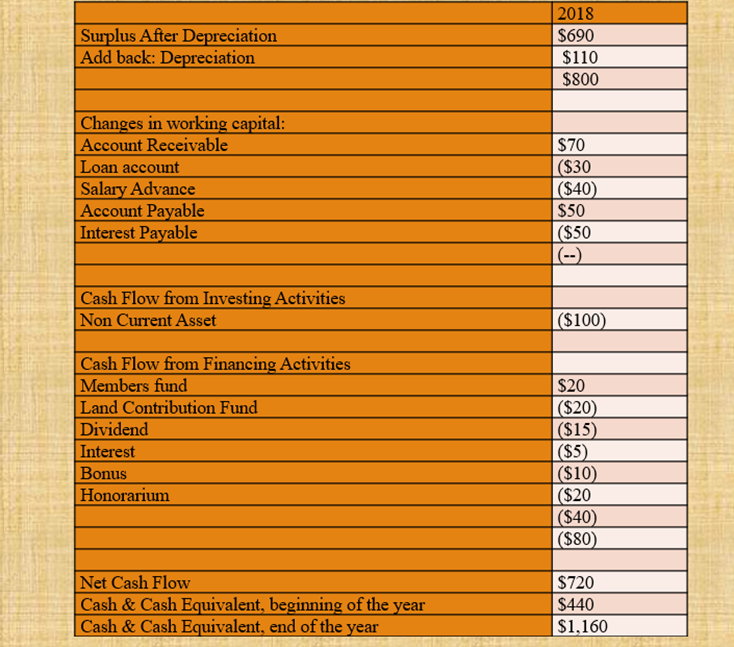

11. CASH FLOW STATEMENT

In addition, a cash flow statement is a financial record that presents a company’s incoming and outgoing cash for a specific period. This document shows the cash flows, the money that comes in and goes out of the business. Cooperative uses these statements to keep track of, document, monitor, and report these transactions.

CONCLUSION

Therefore, cooperative laws around the world require the maintenance of proper accounting records. However, seeking assistance from experts with practical experience can help improve your cooperative accounting system. Furthermore, if you are looking for the best way to manage a cooperative society, consider purchasing a revised cooperative book from our book-shop or at Amazon.com.

Download free Excel financial model designed for cooperative accounting management.

Alternative Dispute Resolution in Nigeria is practiced within Nigeria at the institutional and individual level with and without the involvement of the court system.

The list of institutions that practiced ADR in Nigeria, namely, The Chambers of Commerce, private enterprises, industry groups etc. In the case of individuals are judges, specially trained practitioners (i.e. arbitrators, mediators, accountants), elders, traditional rulers, chiefs, religious leaders.

The practitioners involved in ADR is industry-specific that have technical expertise in specific areas like environmental disputes, labour disputes, family law, etc.

Furthermore, the current Nigerian laws have sufficient provisions that have addressed Alternative Dispute Resolution in Nigeria and the methods in resolving disputes.

These provisions of the laws are discussed below.

(1) The 1999 Constitution

The Constitution is the supreme law of the land that endorses arbitration. Section 19(d) of the Constitution states that part of Nigeria’s foreign policy objective is respect for international law and treaty obligations. Nigeria also seeks for settlement of international disputes by negotiation, mediation, conciliation, arbitration and adjudication.

(2) Arbitration Laws

Nigeria, like other progressive countries, has subscribed to many international ADR Laws and Rules. The United Nations Commission on International Trade Law (UNCTRAL Model Law of 1985) and UNCITRAL Arbitration Rules domesticated in Nigeria under the Arbitration and Conciliation Act (ACA).

(3) Other Federal Acts

Nigerian body of laws is replete with several statutes that provide for arbitration or other ADR mechanisms. However, a fewer list is mentioned below of the law and the applicable sections:

Sections 11 and 30 (4) of the Matrimonial Causes Act (Cap. M7 LFN 2004). This section talks about reconciliation between the husband and wife or parties. As they can get the Marriage conciliator to take an oath of secrecy to settle out of court.

section 2, Consumer Protection Council Act, (Cap C25 LFN 2004),

sections 29 and 33, of the Environmental Impact Assessment (EIA) Act (Cap. E12 LFN 2004),

Sections 4, 8, 9, 20, 22 of the Trade Disputes Act (Cap. T8 LFN 2004),

section 11 of the Petroleum Act(Cap. PI0 LFN 2004),

section 26 of the Nigerian Investment Promotion Commission Act, (Cap. N17 LFN 2004);

section 27 of the Public Enterprises (Privatization and Commercialization) Act, (Cap. P38 LFN 2004),

section 22 of the Nigerian LNG (Fiscal Incentives, Guarantee and Assurance) Act (Cap. N87 LFN 2004),

Section 49 of the Nigerian Co-operative Societies Act (Cap. N98 LFN 2004);

section 5 of the National War College Act (Cap N82 LFN 2004);

sections 3 and 6 of the National Boundary Commission, Etc. Act; (Cap. N10 LFN 2004),

section 3 of the Advisory Council on Religious Affairs Act (Cap. A8 LFN 2004);

section 4 of the National Office for Technology Acquisition and Promotion Act( Cap. N62 LFN 2004),

section 4 of the Nigerian Communications Commission Act (Cap. N97 LFN 2004) etc.

(4) Court Laws and Rules

Lastly, Court laws and rules govern procedures and proceedings for the conduct of business in the court.