Digital products are now one of the most scalable means to set up streams of income. This digital products ventures requires little capital to launch. It may not require physical inventory but only need freelancer to be creative in their writing. Moreover, they are also to use strategy and the right tools.

For me, my story in freelancing changed when I began to use ChatGPT not just as a writing assistant, but as a business partner.

With the strength of ChatGPT to produce content and ideas, I was able to transformed what take me a week into a repeatable system.

The outcome was pleasant to me over time, while I used ChatGPT as a helper. Because of my dependent on this tool, I was able to develop a high-selling digital products that I sell today on several platforms including eBooks, Online Training courses, Fiverr services, and Gumroad.

To benefit fully from this article, just keep reading to see how I achieved this feat and how you can too in your freelancing career.

1. I Packaged My skills

The first mindset I had was to ensure my product solves problems, not just to generate information for my audiences. You need take note, that people don’t pay for the information you share; they are interested in paying for the solutions you provide.

Every freelancers have knowledge in a different capacity, which others may be willing to pay for in dollar. Except the product is package properly, the audiences my not value it.

One way to make digital products create value and easy to buy is to ensure they are well packaged. Based on this understanding, I packaged some of my past work on accounting, data analytics and entrepreneurship into several formats.

Instead of starting from scratch, I enlisted ChatGPT as my business strategist to create contents with a solid foundation. These packages were developed to meet the specific needs of various social media platforms such as Medium, Facebook,Linkedin and with the right Call to action.

2. How ChatGPT Helped Me Achieve My Objectives.

I want to show you how ChatGPT becomes my creative tool for all my digital products:

• eBooks Creation: I will log on to my ChatGPT account and submit the right prompt to produce the content of my eBooks. Once that is done, I paraphrase and polish them to ensure they meet the aim of the eBooks. Then, I will publish them on the Amazon Kindle or Gumroad marketplace.

• Develop Online Courses: With the help of ChatGPT, I was able to get a lesson script that helped me deliver my classes. Then I will paraphrase it to remove the plagiarism so I can own it. This helps me capture video lessons faster with a good structured that makes the class flow well.

• Canva Templates. ChatGPT has helped me create several template such as banners, background pictures and so. The attachments from canvas are placed on my eBook covers and even on my thumbnails of my articles.

3. I Sell My Digital Products on a Platform That Works

It’s good to create a product, but employing the right distribution channel is even better. I have some of my digital products on Book Shop, Fiverr, Amazon Kindle and Gumroad. Am showing you this process because I want you to succeed also. You can also follow this if you are not there yet. These platforms already have a vast audience who are looking for a solution to their problems. As soon as I upload my new digital products, I start receiving sales. Even while I’m sleeping, I continue to receive sales.

4. The Key Lessons Anyone Can Learn

1. Start simple with the product. Since you are starting now, you may not be able to make your work excellent. But one thing I am sure of is that the products have solved someone’s problem.

2. Have a Specific Niche. It is better to focus on a specific niche than to target a product that serves “everyone”. A particular target will sell more than a general target.

3. Let ChatGPT become your helper. Although AI may accelerate the process, incorporating voice and expertise can make the product more authentic.

5. Conclusion

The emergence of ChatGPT has completely transformed how people utilise it to create digital products. Although I have discovered that ChatGPT alone is insufficient for delivering high-quality content, combining it with my unique expertise makes such content possible. If you’re struggling to develop your ideas, consider using ChatGPT as a helper, not a replacement.

Thanks for Reading

Check out my Gumroad for a custom business plan to kickstart your entrepreneurial journey.

Also, I’m available on Fiverrif you need an Excel financial model, forecasts, budget, or projections as an entrepreneur.

Why do small businesses need Excel financial models? This is a question that requires an answer from experts like us. Many small businesses tend to underestimate the importance of Excel financial modeling, assuming it is a tool exclusively designed for large corporations or investment banking professionals. However, this perception overlooks the significant benefits that financial modeling can provide to smaller enterprises.

Excel financial modeling enables small business owners to create detailed projections, analyze cash flow, and assess potential financial scenarios. By utilizing spreadsheets, they can visualize their financial data, track expenses, forecast future revenue, and make informed decisions about investments and budgeting.

Moreover, Excel is a cost-effective solution, as most small businesses already have access to it, making it an accessible resource for analyzing their financial health and planning for growth. Embracing this powerful tool can enhance their strategic planning and ultimately contribute to their long-term success.

I have taken time to list why small businesses need Excel financial models.

1. Cash Flow Management

Small businesses live or die by cash flow.

A financial model in Excel can project when money will come in and go out, helping owners avoid liquidity crises or issues.

Example: Anticipating cash depletion by the sixth month is vital for financial planning. Evaluating spending and income helps avoid shortfalls and maintain smooth cash flow.

2. Budgeting & Cost Control

With a excel financial model, businesses can set a budget and track actual results against it.

Helps to identify where money is leaking (e.g., high overhead, unnecessary expenses).

Enhances decision-making by utilizing data to inform choices instead of relying on guesswork.

3. Decision Making (What-If Scenarios)

Excel financial model makes it easy to run scenario analysis:

What if sales drop 20%?

What if raw materials cost increase?

What if we expand to a new location?

What if labour cost increase by 10%?

This helps business owners test strategies before spending money on any project.

4. Investor & Bank Readiness

If the business owner needs funding as a start-up or exiting business, investors and lenders will want to see projections, break-even analysis, IRR, XIRR and repayment ability.

A clean Excel financial model communicates professionalism and builds trust.

5. Good for Growth Planning

Excel Financial modeling reveals when the business can afford to hire staff, expand operations, or launch new products.

Helps avoid over-expansion or underinvestment.

6. Performance Tracking

Performance tracking is one of its key applications of the model.

By updating the excel financial model monthly, small businesses can track actual vs. forecast.

This creates discipline and accountability.

7. Flexibility & Affordability

Unlike expensive software, Excel is:

Cheap (often already available).

Customizable (can be tailored to any business type such as co-operative society, consulting, manufacturing etc).

Easy to update as the business grows.

In conclusion, Excel financial modeling helps small businesses stay alive, grow smart, and attract funding—all with a tool they already have. Check out these examples in https://www.efinancialmodels.com/.

You will receive a free Excel financial model template you can download and customise for your business if you drop your email on the comment section.

Pay-as-you-earn is a tax deducted from employee salary account. The remittance of this tax is on or before the 10th day of the month following the month in which salaries were paid. See relevant sections of the Personal Income Tax Act (PITA). (S.81 of Personal Income Tax Act Cap P8 LFN 2011). S. for details

Taxable Entitlement (Gross)

This is the total amount your employer pays their employee as salary, including all benefits arising from employment. Another name to call taxable entitlement is Gross Emoluments. These include wages, salaries, allowances including benefits in kind, gratuities, superannuation and any other incomes derived solely because of employment. Regardless, it is essential to note that all allowances are taxable except those reimbursements of employee expenses. However, if such reimbursements are carried out through the employee payslip, they must be subjected to tax in Nigeria. Such reimbursements include training costs, transport to attend training, etc.

Moreover, Section 33(2) of finance-act-2020 defined “gross income” as income from all sources, less non-taxable income, and tax-exempt items.

Table 1 showing the comparison of old PITA and Proposed PITA of an employee who earn N5,775,000 as gross salary.

TAX RELIEF (TAX ALLOWANCE)

This is amounts that can be deducted from a person’s annual income to reduce the amount on which tax is paid. Or the amount of youThese amounts can be deducted from a person’s annual income to reduce the tax paid. In other words, it is the amount of your income exempt from tax aside from other statutory deductions.

Maximum of Personal relief ₦ 800,000.00

Rent Relief of lower of N200,0000 or 20% of actual rent paid.

Table 2 shows that Tax relief of old and proposed method

Tax Exempt

The tax law provides certain payroll deductions as tax exempt or non-taxable deductions. Tax exempt amount has to be removed from Gross taxable Income (earnings) before applying the tax rules to determine tax. The following deductions are not Taxable (.i.e. Tax Exempts):

Union due is 2% of the basic salary.

Pension Deductions (employer 10% and employee 8% of Basic salary, transport and housing allowance).

National Housing Fund Deductions (Employee 2.5% of basic salary).

Life Assurance Payments (this is obtained from the employee life policy document and monthly premium payment receipt is sufficient evidence to earn the tax exempt. Section 33(3) of Finance Act 2020 added that any premium payment. stated that there shall be allowed a deduction of annual amount of any premium paid by the individual during the year preceding the year of assessment to an insurance company in respect of insurance on his life or the life of his spouse or of a contract for a deferred annuity on his own life or the life of his spouse (finance-act-2020). This is addition to the Act.

The National Health Insurance Scheme (Government 10% and employee 5% of basic salary) but employer 5% has not be implemented yet in the federal government MDAs due to Labour objections.

Gratuity.

Table 3 showing the tax exempts for both the old and proposed.

Table 3 shows same amount since the figures are based on same sources

Tax Table

After the relief allowance and tax exemptions have been granted, the income balance shall be taxed as specified in the tax table below. Moreover, the Nigerian Payroll tax table comes in annual gross bands in six rows. Each band has a percentage tax value attached to it. The tax table rates must be applied to the Net Taxable Income to get Tax Payable.

Tax table and Rates from November 2024 tax year (As amended)

First N800, 000 @ 0 per cent

Next N2,200, 000 @ 15 per cent

Next N9,000, 000 @ 18per cent

Next N13,000,000 @ 21 per cent

Next N25,000,000 @ 23 per cent

Above N50, 000,000 @ 25 per cent

Taxable Income (Net)

This is derived after deducting the following from Gross Taxable Income. Some are extracted from payslip.

Gross Entitlement,

Tax Exempts, and

Tax Relief (Tax Allowance).

Apply tax table to the net amount as stated above

Table 4 showing the tax band of the old and the proposed method

Residency Rule

Assuming the Senior Manager who stay in Rivers State but work in Abia State. By residency rule, an employee’s PAYE is payable to the tax authority of the state of his/her residence (Rivers State). It is therefore the duty of the employer to deduct and remit it to the tax authority where the employee is resident. However, if the employee is resident in Rivers State, the tax authority that is entitled to his PAYE is the Rivers State Board of Internal Revenue.

Usually, non-residents are not liable to pay taxes in Nigeria. However, an expatriate employee may be liable to tax in Nigeria if;

Penalty for Failure to Deduct PAYE

Section 74(1) of Personal Income Tax Act, 2011 states “ any person or body corporate who fails to deduct, or having deducted, fails to remit such deductions to the relevant tax authority within 30days from the date the amount was deducted or the time the duty to deduct arose, shall be liable to a penalty of an amount of 10% of the tax not deducted or remitted in addition to the amount of tax not deducted or remitted plus interest at the prevailing monetary policy rate of Central Bank of Nigeria.

Exemption of Minimum Wages Earners

Section 37 of Finance Act 2020 “provided that minimum tax under this section or as provided for under the Sixth Schedule to this Act shall not apply to a person in any year of assessment where such person earns the National Minimum Wage or less from an employment (finance-act-2020).

Books of Accounts

Section 12 of PITA 2011 stated that the keeping of bools of accounts is very important but if any taxable person fails or refuses to keep account, such a person shall be liable on conviction to a penalty of N50,000 for individuals and N500,000 for corporate entities.

Employer File Tax Returns on Behalf of Their Staff.

Every employer is to file annual forms on behalf of their employer called Form H1 and Form A. Also, form H1 is an annual employer’s tax return that shows the names, annual gross income and PAYE taxes of employees in the past tax year together with Form G. Meanwhile, Form G gives information of the annual PAYE paid and the corresponding receipts. The tie to fill Form H1 is on the 31 January of the following year. Therefore, Form A is an annual statement of individual income and claims for allowances and reliefs form. Moreover, the right time to submit is on the 31st of March of the current year.

Conclusion

As an employer, you are responsible for ensuring full compliance with the guidelines set forth by the relevant tax authority concerning calculating your employee’s PAYE (Pay As You Earn). This applies accurately choosing the amount of PAYE to be deducted from each employee’s salary based on their earnings and applicable tax rates.

Furthermore, your civic duty is to remit the PAYE amounts deducted from your employee’s wages to the relevant tax authority promptly and within the specified deadlines. This not only sustains government services but also helps in fulfilling your legal obligations as an employer. Additionally, you must pay any other taxes owed to the relevant tax authority on time to avoid penalties and ensure that your business remains in good standing. Maintaining correct records and staying informed concerning tax regulations will enable you uphold these responsibilities effectively.

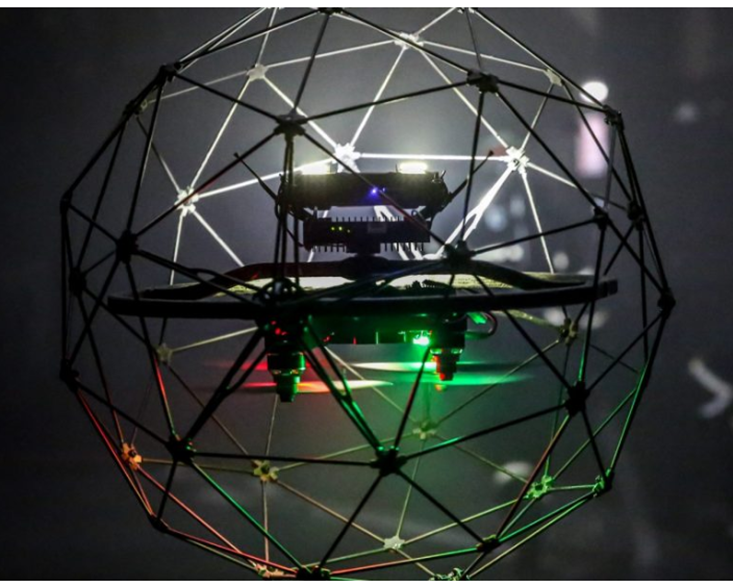

How accountant use Drone technology to achieve their task depends on the sectors or schedule of activities. In addition, drones are unmanned aerial vehicles (UAVs) that can fly remotely.

The global drone market predicts to increase from $26.3 billion in 2021 to $41.3 billion by 2026. Also, in 2020, both US and the UK used drones to deliver drugs during the COVID-19 pandemic (Appelbaum et al., 2020).

Drone technology has proven helpful in war zones and intelligence gathering and also in a civilian role, such as:

Countries that make use of drone technology and require permission for all aerial drones through regulation.

Moreover, the regulation addresses different types of civil drone operations and their respective levels of risk as stated by European Union Aviation Safety Agency

In Germany, there are limited zones outside protected areas with high urban density or people conglomerations.

Also, all EU Member States, including Norway and Liechtenstein.

Switzerland and Iceland are also expected to apply this regulation soon.

In United States for example, they used drone technology for their operation(Ovaska-Few, 2017).

In 2013, Poland passed a law allowing the commercial operation of drones, which led to the birth of Drone Powered Solutions.

South Africa that has entirely established drone regulations in place which was carefully integrated into existing aviation law.

Lastly, in Australia, Rio Tinto who has its facility in a remote area planned in 2016 to start using drone to monitor mine sites including the staff.

Companies that have used drone in their workplace and in others area of operations.

It was recorded that PwC completed its first stock count audit using drone technology. With the assistance of a drone, they were able to capture images at a coal reserve in South Wales and used them to measure the volume of the coal, based on the measurement of volume.

Amazon and Google are already testing ways to deliver packages with drones.

Facebook has started using drones to provide internet connections in remote locations.

Basin Electric’s utilization of drones has enhanced efficiency and safety while concurrently reducing costs.

Furthermore, Ford Motor Company filed a patent to start the use of drones for dead bateries. The patent was filed on 3rd February, 2017 and circulated on March 8th, 2022, and assigned serial number 11271420.

How Accountant Use Drone Technology to the Accounting Profession.

Source: Naira Technology

With the help of drone technology, however, accountants can now complete their work in a shorter amount of time. Technological advancements have significantly changed the accounting and auditing profession in recent years.

In 2017, the emergence of drone technology has revolutionized the accounting and auditing profession. Drones have opened up new possibilities for accountants to perform their tasks more efficiently and effectively.

Emerging technologies like AI, blockchain, big data, the IOT, and drone technology have revolutionized accounting profession (Qasim et al., 21).

For example, accounting and audit firms that work with clients in mining and inventory can utilize drone technology to take thousands of pictures and measurements of a site (Ovaska-Few,2017).

Also, this can aid in accurate assessments of holdings, making tasks like physically measuring coal a thing of the past. An estimated volume can be obtained in less time with just a two-meter GPS Tracking pole.

What are the Benefits of Drone Technology to the Accounting and Audit profession.

Perform physical inventory: Drone could recount inventory if required-data feed repeatedly into audit app that re-performs the process. Using drones to automate livestock inventory count reduced count time from 681 hours to 19 hours (Qasim et al., 21).

Time-efficiency and effectiveness: Drone devices help to improve and increase effectiveness and efficiency in the accounting and auditing profession.

Accuracy: Produce accurate data that can be relevant for future forecast and planning. It depend on how accountant use drone technology to collect insight into the condition of assets. This is faster, cheaper, safer and more accurate than traditional methods (Johnson, 2022).

Save Cost: Drones may save money for accounting clients, who can use them for stock takes, mapping, safety monitoring and to inspect bridges and building.

Productivity: It can enhance productivity

Also, Reduce the risk of injury: he benefit in health and safety as the need for someone to climb over the coal pile are removed.

Speed: Helps speed up some business and accounting processes.

Monitoring strategies . Help monitor staff, operation and some dangerous zone. For instance, drones can assist the firm or staff to take account area difficult to reach.

Storage of Long-term data: Moreover, drone methods allow for storage of long-term data. This is useful to account for physical factors (like weather, light conditions and geomorphology of the beach) for more spatio-temporal analysis.

Automate and accelerate repetitive accounting tasks (Qasim et al., 21).

The technology produces massive amounts of data that require interpretation and translation into meaningful information for informed business decisions.

Also, as accountants keeping up to date with new technologies and understanding their potential to enhance efficiency and effectiveness is essential. Developing the necessary skills to interpret and present data will enable them to add value to their employers. Since the drones technology are control by expert . However, drones are prone to making mistakes just like any other technology, which is why one can exempt them from errors.

Furthermore, competent accountants who are conversant with latest technology, play a crucial role in helping companies thrive and maintain a competitive advantage. It is imperative that organizations have skilled accountants on their team to achieve these goals.

Implications of How Accountant use drone Technology to the Accountants and Auditors

Be part of the at least 95% that will accept this new technology if they must prepare for the future.

Develop a new skill that is all-encompassing for them to be relevant every time and drive the development of accounting profession.

For companies to successfully transform, there will be a great demand for individuals with fundamental knowledge and expertise. For instance, such individuals must possess the necessary skills and understanding to support the company’s transformational goals.

Also, become a consultant in the field to remain relevant and being in change of the world where we live by data.

Become a strategic thinker.

Apply professional judgement whenever is necessary and obtain a better results

Establish Drone-focused department that enable accounting firms to handle all matter related to drone.

Check the impact of drones on client’s business operations.

Lastly, it is vital for every accountant or auditors to be familiar with the present drone regulations in their countries.

Conclusion

In this article, the writer examined how accountant use drone technology and to achieve their work on daily basis. Similarly, drones can improve the accuracy and efficiency of audits. However, how they can use it to collect data and perform inspections in hard-to-reach areas.

Consequently, the article highlighted the potential impact of commercial drones on the accounting profession, with predictions that this technology will revolutionize traditional accounting procedures (Ovaska-Few, 2017). Accounting professionals and academics need to recognize the significance of drone technology and patronize the suppliers as it is here to stay. In addion, the sooner we adapt to this technology and use it to their advantage, the better. Accountants and auditors are condition to embrace this new technology and see it as an improvement to their jobs instead of threat.

E-Collection is electronic collection of government revenue. Therefore, E-Collection through Treasury Single Account received new development since inception.

However, some of the improvement to e-collection are in line with Central Bank of Nigeria (CBN) circular of 10th December 2020.

New Development of E-Collection/TSA implementation in Nigeria

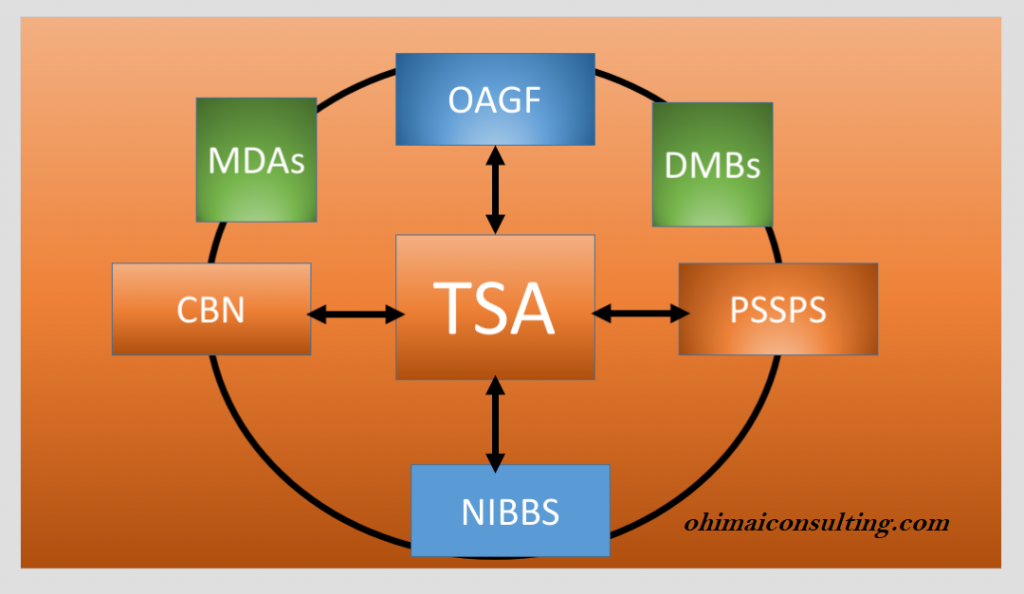

1. New TSA cost of E-Collections for payer and Ministries, Department and Agencies (MDAs). The charges are grouped into two.

(A). Transaction charges borne by the payer. i) If the payment is received through Point of Sales (POS), it will attract N150 plus 0.50 per cent of the amount being paid subject to a maximum of N1, 000 per transaction.

ii). If payment is received through other channeled, it attracts N150 exclusive of Value Added Tax (VAT)

(B). Transaction charges borne by the MDAs.

(i) They provide the platform for collection.

(ii) They will process all data about the payment and the payer.

(iii) They transmit the data and replicate them and lastly

(iv) Fund sweeping. For this, stakeholder below is to receive fromPayment Solution Service providers (PSSPs) or Deposit Money Banks (DMBs) fund sweeping. This depends on who is playing the collection role for the MDAs. NIBBS is to receives 10% while Office of the Accountant General of the Federation (OAGF) to receives 2.5%.

2. New TSA sharing formula for collection cost received among the various stakeholders as follows:

PSSPs——————————-43%

Collecting Banks——————33%

CBN———————————11%

NIBBS——————————-10.5%

OAGF——————————–2.5%

3. The government link the revenue generating agencies to TSA portal through (PSSPS). PSSPs are companies appointed by government to collect TSA payments from ministries departments and agencies (MDAs).

As at today, payer has to initiate payment from the receiving agencies portal. The way to initiate is to get register or enrolled in the receiving agencies portal.

Requirement to Sign Up for E-Collection/TSA Platform

For E-Collection platform to be effective, these requirements are essential:

a. Provide Tax Identification Number (TIN) and certificate

c. Wait for account to be approved by the receiving agencies

Then, payer cab initiate payment from payer personal account in the receiving agencies portal

Payer will automatically transfer to TSA portal from the receiving agencies portal, for instance Remita

4. Time to Initiate Payment

Payer can only initiate Payment into TSA only when step 3 is being completed.

5. Stakeholders

The addition of Etranzact, Interswitch to join SystemSpec (the operator of Remita) to collect government revenue.SystemSpec has acted as a sole PSSPS appointed by government to collect TSA payments from MDAs.

6. Electronic Payment Companies

The main electronic payment companies involved in TSA increased to four companies. They are Etranzact, Interswitch, SystemSpec and Nigeria Interbank settlement System (NIBSS).

Therefore, NIBBS ensures that all the relevant stakeholders comply with the framework and also communicate collection codes for remittance to PSSPs.

Conclusion

Ogbonna and Ojeaburu (2015) in their study recommended among others, that the government should strengthen Government Integrated Financial Management Information System (GIFMIS) module. Also, cover other area of interest in the national budget to achieve economic development. Moreover, more need to be done to ensure E-Collection are active in all MDAs.