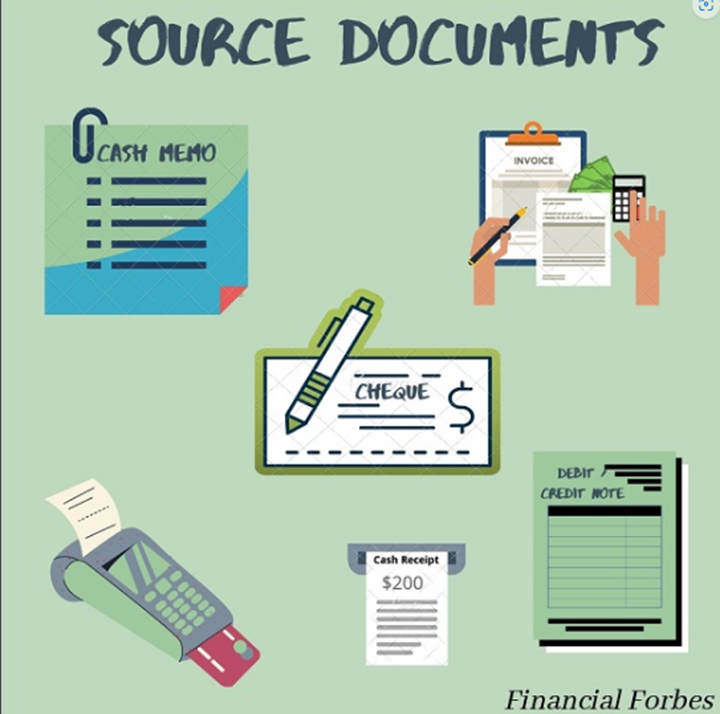

Top 35 Source Documents in Accounting are relevant to help accountant to help accountant in their job. Also, it is a document that serves as proof of transactions that is available in apps that provide such services.

Top 35 Source Documents in Accounting stated below:

The buyer sends this to the vendor. They will then outline exactly what the order should contain and when it should arrive.

2. Sales Invoice

This is a process for managing account receivables. When the seller gives out goods, they will provide a document containing all relevant sale details.

3. Purchase Invoice

This is made for account payables. The seller will enter this as sales invoice while the buyer will enter it as purchase invoice.

4. Debit Note

This is evidence of reduction in purchases and can be useful to support purchases return journal. Furthermore, in customer books, debit note will reduce how much they owe to the seller.

5. Credit Note

This is evidence of reduced sales and support sales return journal. In addition to supplier’s books, credit note reduces the amount owed by the customer.

6. Cheque

This is a special bank note that represents the cash paid by the customer.

7. Revenue receipt

This is used to record the receipt of cash which is a proof that the payment is made.

8. Cash register receipts

This is a business paper that listed the money coming in from customers.

9. Bank or Credit advice

They are debit or credit bank advice. Bank credit advice is bank documents informing the business of an increase made in the business’s bank account. Unlike bank debit advice that is opposite to bank credit advice.

10. Deposit slips

When one receives cheque or cash from customer, the seller will take it to the bank and present.

11. ATM cards

The production of receipt from ATM machine can serve as evidence that money has been taken from the bank account.

12. Bank statements

This is a summary of financial transactions that occurred at a certain institution during a specific time period. For example, a typical bank statement may show your deposits and withdrawals for a certain month.

13. Bill of exchange

This is an unconditional order in writing, addressed by one person to another, signed by the person giving it. It also require the person to whom it is addressed to pay on demand.

14. Payroll report

This can also refer to the list of employees of a business and the amount of compensation due to each of them.

15. Cancelled Cheque

This is a check that has been paid or cleared by the bank

16. Cheque Stubs

This is the check kept by the payee with information such as the check number, date, and amount.

17. Employee Timecard

This is a method for recording and tracking the amount of an employee’s time spent on each job

18. Board minutes or minutes of meetings

The secretary of the board usually takes minutes during meetings.

19. Goods Dispatched Note (GDN)

This a document of the company that lists the goods sent out to a customer. Without a doubt, the company will keep one record of goods dispatched notes.

20. Goods Issues Note (GIN)

This is a physical record of the movement of goods or materials from the warehouse or store to production department.

21. Stock take Records

This is also called stock counting. It is when you manually check and record all the inventory that your business currently has on hand

22. Stock Record

A Bin Card is a card indicating quantitative records of the receipts, issues and balances etc.

23. Goods Received Note (GRN)

This is source document that shows the goods that a business has received from a supplier.

24. Remittance advice

This source document can confirm the amount paid and shows discrepancies that can easily be investigated.

25. Insurance Endorsement Certificates

This is where one party will add the other party as an “additional insured” on their commercial liability insurance policy.

26. Point of Sales Summaries

This can be used to record a number of sales at a cash register.

27. Memorandum

Memo is a written document businesses use to communicate an announcement, policy changes, price increases or notification to take an action, such as attend a meeting, or change a current production procedure.

28. Computer-generated Receipts

This is the kind of receipts is to be generated by the computer.

29. Lease Agreement or Rental Agreement

Lease contracts are formal documents that identify the lessor, lessee, what’s being leased, whether it’s an asset or a property.

30. Sales Tax Returns

This is the taxpayer’s document of declaration. This will enable the taxpayer to furnish the transaction details during a tax period and deposits his Sales Tax liability.

31. Cash Register Tapes

This allowed one to keep a record of all customer transactions and/or provide them with a receipt.

32. Adjustment Notes

This are issued to customers due to damaged, returned or undelivered goods

33. Employee Pay Advice

This source document that can helped to provide written evidence concerning employee income.

34. Payroll Advice Report

This payroll reports helped small businesses understand payroll costs and summarize payroll data.

35. Evidence of Sale or Disposal of Assets

This is the removal of a long-term asset from the company’s accounting records.

Conclusion

Indeed, all these top 35 source documents in accounting are integrated in several apps that offer such accounting services. Moreover, this App made it possible to have all these source documents in one place to make the accountant job easier and simple.

Kindly add your own source documents to the Top 35 Source Documents in Accounting listed above. This will help us to update our records accordingly.

Watch several videos of how to prepare financial statements from source documents

There are basic assumptions which underline the preparation of financial statements of business enterprise. There are stated below:

Going concern concept: accounting assumes that the business will continue to operate for a long period of time. In other words, it means continuity in business or Continuity Assumption.

The continue preparation of financial statement in accordance with International Financial Reporting Standard (IFRS) is an evidence of going concern. Even the auditor may also carry out investigation see that the going concern is intact.

Example of going concern is prepayment and accrual of expenses. The company accept these expenses because they believe the business will continue to run. If for example any part or section or department or product line is discontinue, it does not means there is no longer a going concern. Going concern is for the entire company.

During Covid19, a lot of companies had financial issues and were unable to pay their obligation. Various government gives those companies a bailout and a guarantee of all payments to creditors. The companies are a going concern despite of its current weak financial position. But if government imposes a restriction on the manufacture of a certain goods and service for the period say 1 year. Then the company will no longer be a going concern since they might not be able to sell any product.

2. Entity concept: This accounting concept separates the business from its owner. Meaning the business is a legal entity. It can sue and be sued. It also means the owners of a business are limited to how much he has invested not his personal resources. So for example, if the owner brings in additional capital into the business, we will treat this as a liability on the balance sheet of the business.Entity concept ensures that each company is tax separately.

Let look at these examples, Mrs. Ese bought a building having 5 office space for $5000 per month. She uses three office for his business and two for personal purpose. In line with business entity concept, only $3,000 (the rent of two offices) is a valid expense of the business

Another example is when owner of a business lends loan to his company. It would be strictly recorded as a liability and that has to be paid back to the owner.

3. Matching Concept:This concept states that the revenue and the expenses of a transaction should be included in the same accounting period. So to determine the income of a period all the revenues and expenses (whether paid or not) must be included. The matching accounting concept follows the realization concept. First, the revenue is recognized and then we match the costs associated with the revenue. So costs are matched with revenue, the reverse would be an incorrect system.

4. Dual concepts: this says that there are two aspects of accounting. It is represented by the assets of the business and liabilities (i.e. claims against it). Assets =liabilities + capital. So for example. Say the business buys an asset worth N10, 000. So now the Fixed Assets of the company will increase by N10, 000. But at the same time, the bank or cash balance will reduce by N10, 000 and so the transaction will have a dual effect in accounting. And also the Balance Sheet will stay balanced.

5. Realization concepts: in accounting, profit should not be recognized until the goods are passed to the customer.

6. Money measurement concept: Accounting is only concerned with the facts that can be measured in monetary terms with fair degree of objectivity. Accounting does not record that the firm has a bad or good management team, poor morale among staff. So for example, if the company underwent a major management overhaul this would have no effect on the accounting records. This concept is actually one of the major drawbacks of accounting.

7. Accrual concept: Revenue and cost are usually recorded in accounts when they are earned or incurred rather than when the money is received or paid.

8. Full Disclosure Concept: This concept states that all relevant information will be disclosed in the accounting statements. A lot of external users depend on these financial statements for their information to make investing decisions. So no information/transactions etc of relevance to any one of them will be omitted from these statements for the benefit of the company.

9. Cost Concept: This accounting concept states that all assets of the firm are entered into the books of account at their purchase price (cost of acquisition + transport + installation etc). In the subsequent years to, the price remains the same (minus depreciation charged). The market price of the asset is not taken into consideration.

10. Accounting Period Concept:Every organization, according to its needs, chooses a specific period of time to complete an accounting cycle. Generally, the time chosen is a year we call the accounting year. The time period is mentioned in the financial statements.

11. Substance over form: usually transactions are recorded and accounted for by their commercial realities rather than their legal form. Substance over form is an accounting concept which means that the economic substance of transactions and events must be recorded in the financial statements rather than just their legal form in order to present a true and fair view of the affairs of the entity.

12. Faithful representation: For financial report to be useful, the financial information must not only represent relevant phenomena but must faithfully represent the phenomena that it purports to represent.

13. Timeliness: It means having information available to decision makers in time to be capable of influencing their decisions. The older the information the less important it become.

14. Relevance: Relevant information is capable of making a difference in the decisions made by users.

15. Comparability: The information about a firm is more useful if it can be compared with similar information about other enterprise and with similar information about the same enterprise for another period or date.