Pay-as-you-earn is a tax deducted from employee salary account. The remittance of this tax is on or before the 10th day of the month following the month in which salaries were paid. See relevant sections of the Personal Income Tax Act (PITA). (S.81 of Personal Income Tax Act Cap P8 LFN 2011). S. for details

Taxable Entitlement (Gross)

This is the total amount your employer pays their employee as salary, including all benefits arising from employment. Another name to call taxable entitlement is Gross Emoluments. These include wages, salaries, allowances including benefits in kind, gratuities, superannuation and any other incomes derived solely because of employment. Regardless, it is essential to note that all allowances are taxable except those reimbursements of employee expenses. However, if such reimbursements are carried out through the employee payslip, they must be subjected to tax in Nigeria. Such reimbursements include training costs, transport to attend training, etc.

Moreover, Section 33(2) of finance-act-2020 defined “gross income” as income from all sources, less non-taxable income, and tax-exempt items.

Table 1 showing the comparison of old PITA and Proposed PITA of an employee who earn N5,775,000 as gross salary.

TAX RELIEF (TAX ALLOWANCE)

This is amounts that can be deducted from a person’s annual income to reduce the amount on which tax is paid. Or the amount of youThese amounts can be deducted from a person’s annual income to reduce the tax paid. In other words, it is the amount of your income exempt from tax aside from other statutory deductions.

Maximum of Personal relief ₦ 800,000.00

Rent Relief of lower of N200,0000 or 20% of actual rent paid.

Table 2 shows that Tax relief of old and proposed method

Tax Exempt

The tax law provides certain payroll deductions as tax exempt or non-taxable deductions. Tax exempt amount has to be removed from Gross taxable Income (earnings) before applying the tax rules to determine tax. The following deductions are not Taxable (.i.e. Tax Exempts):

Union due is 2% of the basic salary.

Pension Deductions (employer 10% and employee 8% of Basic salary, transport and housing allowance).

National Housing Fund Deductions (Employee 2.5% of basic salary).

Life Assurance Payments (this is obtained from the employee life policy document and monthly premium payment receipt is sufficient evidence to earn the tax exempt. Section 33(3) of Finance Act 2020 added that any premium payment. stated that there shall be allowed a deduction of annual amount of any premium paid by the individual during the year preceding the year of assessment to an insurance company in respect of insurance on his life or the life of his spouse or of a contract for a deferred annuity on his own life or the life of his spouse (finance-act-2020). This is addition to the Act.

The National Health Insurance Scheme (Government 10% and employee 5% of basic salary) but employer 5% has not be implemented yet in the federal government MDAs due to Labour objections.

Gratuity.

Table 3 showing the tax exempts for both the old and proposed.

Table 3 shows same amount since the figures are based on same sources

Tax Table

After the relief allowance and tax exemptions have been granted, the income balance shall be taxed as specified in the tax table below. Moreover, the Nigerian Payroll tax table comes in annual gross bands in six rows. Each band has a percentage tax value attached to it. The tax table rates must be applied to the Net Taxable Income to get Tax Payable.

Tax table and Rates from November 2024 tax year (As amended)

First N800, 000 @ 0 per cent

Next N2,200, 000 @ 15 per cent

Next N9,000, 000 @ 18per cent

Next N13,000,000 @ 21 per cent

Next N25,000,000 @ 23 per cent

Above N50, 000,000 @ 25 per cent

Taxable Income (Net)

This is derived after deducting the following from Gross Taxable Income. Some are extracted from payslip.

Gross Entitlement,

Tax Exempts, and

Tax Relief (Tax Allowance).

Apply tax table to the net amount as stated above

Table 4 showing the tax band of the old and the proposed method

Residency Rule

Assuming the Senior Manager who stay in Rivers State but work in Abia State. By residency rule, an employee’s PAYE is payable to the tax authority of the state of his/her residence (Rivers State). It is therefore the duty of the employer to deduct and remit it to the tax authority where the employee is resident. However, if the employee is resident in Rivers State, the tax authority that is entitled to his PAYE is the Rivers State Board of Internal Revenue.

Usually, non-residents are not liable to pay taxes in Nigeria. However, an expatriate employee may be liable to tax in Nigeria if;

Penalty for Failure to Deduct PAYE

Section 74(1) of Personal Income Tax Act, 2011 states “ any person or body corporate who fails to deduct, or having deducted, fails to remit such deductions to the relevant tax authority within 30days from the date the amount was deducted or the time the duty to deduct arose, shall be liable to a penalty of an amount of 10% of the tax not deducted or remitted in addition to the amount of tax not deducted or remitted plus interest at the prevailing monetary policy rate of Central Bank of Nigeria.

Exemption of Minimum Wages Earners

Section 37 of Finance Act 2020 “provided that minimum tax under this section or as provided for under the Sixth Schedule to this Act shall not apply to a person in any year of assessment where such person earns the National Minimum Wage or less from an employment (finance-act-2020).

Books of Accounts

Section 12 of PITA 2011 stated that the keeping of bools of accounts is very important but if any taxable person fails or refuses to keep account, such a person shall be liable on conviction to a penalty of N50,000 for individuals and N500,000 for corporate entities.

Employer File Tax Returns on Behalf of Their Staff.

Every employer is to file annual forms on behalf of their employer called Form H1 and Form A. Also, form H1 is an annual employer’s tax return that shows the names, annual gross income and PAYE taxes of employees in the past tax year together with Form G. Meanwhile, Form G gives information of the annual PAYE paid and the corresponding receipts. The tie to fill Form H1 is on the 31 January of the following year. Therefore, Form A is an annual statement of individual income and claims for allowances and reliefs form. Moreover, the right time to submit is on the 31st of March of the current year.

Conclusion

As an employer, you are responsible for ensuring full compliance with the guidelines set forth by the relevant tax authority concerning calculating your employee’s PAYE (Pay As You Earn). This applies accurately choosing the amount of PAYE to be deducted from each employee’s salary based on their earnings and applicable tax rates.

Furthermore, your civic duty is to remit the PAYE amounts deducted from your employee’s wages to the relevant tax authority promptly and within the specified deadlines. This not only sustains government services but also helps in fulfilling your legal obligations as an employer. Additionally, you must pay any other taxes owed to the relevant tax authority on time to avoid penalties and ensure that your business remains in good standing. Maintaining correct records and staying informed concerning tax regulations will enable you uphold these responsibilities effectively.

Alternative Dispute Resolution in Nigeria is practiced within Nigeria at the institutional and individual level with and without the involvement of the court system.

The list of institutions that practiced ADR in Nigeria, namely, The Chambers of Commerce, private enterprises, industry groups etc. In the case of individuals are judges, specially trained practitioners (i.e. arbitrators, mediators, accountants), elders, traditional rulers, chiefs, religious leaders.

The practitioners involved in ADR is industry-specific that have technical expertise in specific areas like environmental disputes, labour disputes, family law, etc.

Furthermore, the current Nigerian laws have sufficient provisions that have addressed Alternative Dispute Resolution in Nigeria and the methods in resolving disputes.

These provisions of the laws are discussed below.

(1) The 1999 Constitution

The Constitution is the supreme law of the land that endorses arbitration. Section 19(d) of the Constitution states that part of Nigeria’s foreign policy objective is respect for international law and treaty obligations. Nigeria also seeks for settlement of international disputes by negotiation, mediation, conciliation, arbitration and adjudication.

(2) Arbitration Laws

Nigeria, like other progressive countries, has subscribed to many international ADR Laws and Rules. The United Nations Commission on International Trade Law (UNCTRAL Model Law of 1985) and UNCITRAL Arbitration Rules domesticated in Nigeria under the Arbitration and Conciliation Act (ACA).

(3) Other Federal Acts

Nigerian body of laws is replete with several statutes that provide for arbitration or other ADR mechanisms. However, a fewer list is mentioned below of the law and the applicable sections:

Sections 11 and 30 (4) of the Matrimonial Causes Act (Cap. M7 LFN 2004). This section talks about reconciliation between the husband and wife or parties. As they can get the Marriage conciliator to take an oath of secrecy to settle out of court.

section 2, Consumer Protection Council Act, (Cap C25 LFN 2004),

sections 29 and 33, of the Environmental Impact Assessment (EIA) Act (Cap. E12 LFN 2004),

Sections 4, 8, 9, 20, 22 of the Trade Disputes Act (Cap. T8 LFN 2004),

section 11 of the Petroleum Act(Cap. PI0 LFN 2004),

section 26 of the Nigerian Investment Promotion Commission Act, (Cap. N17 LFN 2004);

section 27 of the Public Enterprises (Privatization and Commercialization) Act, (Cap. P38 LFN 2004),

section 22 of the Nigerian LNG (Fiscal Incentives, Guarantee and Assurance) Act (Cap. N87 LFN 2004),

Section 49 of the Nigerian Co-operative Societies Act (Cap. N98 LFN 2004);

section 5 of the National War College Act (Cap N82 LFN 2004);

sections 3 and 6 of the National Boundary Commission, Etc. Act; (Cap. N10 LFN 2004),

section 3 of the Advisory Council on Religious Affairs Act (Cap. A8 LFN 2004);

section 4 of the National Office for Technology Acquisition and Promotion Act( Cap. N62 LFN 2004),

section 4 of the Nigerian Communications Commission Act (Cap. N97 LFN 2004) etc.

(4) Court Laws and Rules

Lastly, Court laws and rules govern procedures and proceedings for the conduct of business in the court.

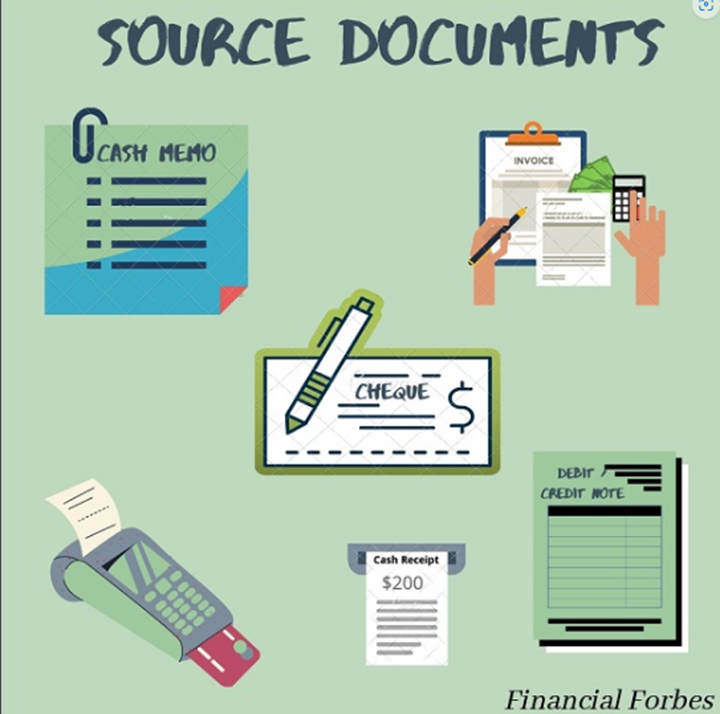

Top 35 Source Documents in Accounting are relevant to help accountant to help accountant in their job. Also, it is a document that serves as proof of transactions that is available in apps that provide such services.

Top 35 Source Documents in Accounting stated below:

The buyer sends this to the vendor. They will then outline exactly what the order should contain and when it should arrive.

2. Sales Invoice

This is a process for managing account receivables. When the seller gives out goods, they will provide a document containing all relevant sale details.

3. Purchase Invoice

This is made for account payables. The seller will enter this as sales invoice while the buyer will enter it as purchase invoice.

4. Debit Note

This is evidence of reduction in purchases and can be useful to support purchases return journal. Furthermore, in customer books, debit note will reduce how much they owe to the seller.

5. Credit Note

This is evidence of reduced sales and support sales return journal. In addition to supplier’s books, credit note reduces the amount owed by the customer.

6. Cheque

This is a special bank note that represents the cash paid by the customer.

7. Revenue receipt

This is used to record the receipt of cash which is a proof that the payment is made.

8. Cash register receipts

This is a business paper that listed the money coming in from customers.

9. Bank or Credit advice

They are debit or credit bank advice. Bank credit advice is bank documents informing the business of an increase made in the business’s bank account. Unlike bank debit advice that is opposite to bank credit advice.

10. Deposit slips

When one receives cheque or cash from customer, the seller will take it to the bank and present.

11. ATM cards

The production of receipt from ATM machine can serve as evidence that money has been taken from the bank account.

12. Bank statements

This is a summary of financial transactions that occurred at a certain institution during a specific time period. For example, a typical bank statement may show your deposits and withdrawals for a certain month.

13. Bill of exchange

This is an unconditional order in writing, addressed by one person to another, signed by the person giving it. It also require the person to whom it is addressed to pay on demand.

14. Payroll report

This can also refer to the list of employees of a business and the amount of compensation due to each of them.

15. Cancelled Cheque

This is a check that has been paid or cleared by the bank

16. Cheque Stubs

This is the check kept by the payee with information such as the check number, date, and amount.

17. Employee Timecard

This is a method for recording and tracking the amount of an employee’s time spent on each job

18. Board minutes or minutes of meetings

The secretary of the board usually takes minutes during meetings.

19. Goods Dispatched Note (GDN)

This a document of the company that lists the goods sent out to a customer. Without a doubt, the company will keep one record of goods dispatched notes.

20. Goods Issues Note (GIN)

This is a physical record of the movement of goods or materials from the warehouse or store to production department.

21. Stock take Records

This is also called stock counting. It is when you manually check and record all the inventory that your business currently has on hand

22. Stock Record

A Bin Card is a card indicating quantitative records of the receipts, issues and balances etc.

23. Goods Received Note (GRN)

This is source document that shows the goods that a business has received from a supplier.

24. Remittance advice

This source document can confirm the amount paid and shows discrepancies that can easily be investigated.

25. Insurance Endorsement Certificates

This is where one party will add the other party as an “additional insured” on their commercial liability insurance policy.

26. Point of Sales Summaries

This can be used to record a number of sales at a cash register.

27. Memorandum

Memo is a written document businesses use to communicate an announcement, policy changes, price increases or notification to take an action, such as attend a meeting, or change a current production procedure.

28. Computer-generated Receipts

This is the kind of receipts is to be generated by the computer.

29. Lease Agreement or Rental Agreement

Lease contracts are formal documents that identify the lessor, lessee, what’s being leased, whether it’s an asset or a property.

30. Sales Tax Returns

This is the taxpayer’s document of declaration. This will enable the taxpayer to furnish the transaction details during a tax period and deposits his Sales Tax liability.

31. Cash Register Tapes

This allowed one to keep a record of all customer transactions and/or provide them with a receipt.

32. Adjustment Notes

This are issued to customers due to damaged, returned or undelivered goods

33. Employee Pay Advice

This source document that can helped to provide written evidence concerning employee income.

34. Payroll Advice Report

This payroll reports helped small businesses understand payroll costs and summarize payroll data.

35. Evidence of Sale or Disposal of Assets

This is the removal of a long-term asset from the company’s accounting records.

Conclusion

Indeed, all these top 35 source documents in accounting are integrated in several apps that offer such accounting services. Moreover, this App made it possible to have all these source documents in one place to make the accountant job easier and simple.

Kindly add your own source documents to the Top 35 Source Documents in Accounting listed above. This will help us to update our records accordingly.

Watch several videos of how to prepare financial statements from source documents

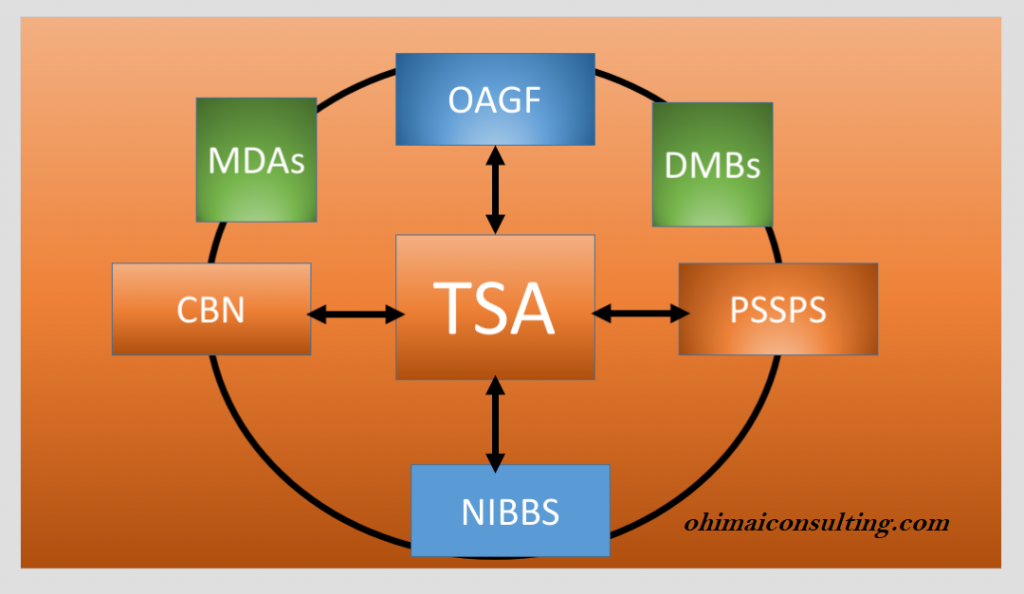

E-Collection is electronic collection of government revenue. Therefore, E-Collection through Treasury Single Account received new development since inception.

However, some of the improvement to e-collection are in line with Central Bank of Nigeria (CBN) circular of 10th December 2020.

New Development of E-Collection/TSA implementation in Nigeria

1. New TSA cost of E-Collections for payer and Ministries, Department and Agencies (MDAs). The charges are grouped into two.

(A). Transaction charges borne by the payer. i) If the payment is received through Point of Sales (POS), it will attract N150 plus 0.50 per cent of the amount being paid subject to a maximum of N1, 000 per transaction.

ii). If payment is received through other channeled, it attracts N150 exclusive of Value Added Tax (VAT)

(B). Transaction charges borne by the MDAs.

(i) They provide the platform for collection.

(ii) They will process all data about the payment and the payer.

(iii) They transmit the data and replicate them and lastly

(iv) Fund sweeping. For this, stakeholder below is to receive fromPayment Solution Service providers (PSSPs) or Deposit Money Banks (DMBs) fund sweeping. This depends on who is playing the collection role for the MDAs. NIBBS is to receives 10% while Office of the Accountant General of the Federation (OAGF) to receives 2.5%.

2. New TSA sharing formula for collection cost received among the various stakeholders as follows:

PSSPs——————————-43%

Collecting Banks——————33%

CBN———————————11%

NIBBS——————————-10.5%

OAGF——————————–2.5%

3. The government link the revenue generating agencies to TSA portal through (PSSPS). PSSPs are companies appointed by government to collect TSA payments from ministries departments and agencies (MDAs).

As at today, payer has to initiate payment from the receiving agencies portal. The way to initiate is to get register or enrolled in the receiving agencies portal.

Requirement to Sign Up for E-Collection/TSA Platform

For E-Collection platform to be effective, these requirements are essential:

a. Provide Tax Identification Number (TIN) and certificate

c. Wait for account to be approved by the receiving agencies

Then, payer cab initiate payment from payer personal account in the receiving agencies portal

Payer will automatically transfer to TSA portal from the receiving agencies portal, for instance Remita

4. Time to Initiate Payment

Payer can only initiate Payment into TSA only when step 3 is being completed.

5. Stakeholders

The addition of Etranzact, Interswitch to join SystemSpec (the operator of Remita) to collect government revenue.SystemSpec has acted as a sole PSSPS appointed by government to collect TSA payments from MDAs.

6. Electronic Payment Companies

The main electronic payment companies involved in TSA increased to four companies. They are Etranzact, Interswitch, SystemSpec and Nigeria Interbank settlement System (NIBSS).

Therefore, NIBBS ensures that all the relevant stakeholders comply with the framework and also communicate collection codes for remittance to PSSPs.

Conclusion

Ogbonna and Ojeaburu (2015) in their study recommended among others, that the government should strengthen Government Integrated Financial Management Information System (GIFMIS) module. Also, cover other area of interest in the national budget to achieve economic development. Moreover, more need to be done to ensure E-Collection are active in all MDAs.