Some of the best consultancy services any expert can specialize on are financial and auditing services, tax management services, education services, cloud computing, accounting packages. Also, human resources management and career development, business and marketing development, professional training services, books and journal publication, self-publishing and lot more.

Kind of Consultancy services rendered by Ohimai Consulting

The selected list is among the best consultancy services as discussed below.

Financial and auditing services. The consultancy will ensure that accounting and auditing of all their clients are handled professionally.

Tax management services. The consultant manages all the taxes such as Pay-As-You-Earn (PAYE), company income tax, tax return fillings, creation of Tax Identification Number, VAT management, tax clearance, stamp duty. the consultant will ensure that all their clients don’t default or violate the tax law but ensures full compliance of their civil right and obligation.

Educational Services. The consultant through the consultancy services will render helps to students and non-students in foreign land. Through these services, Ohimai Consulting now mentored students in the foreign universities.

Cloud Computing. The consultant will be able to manage several firms without having to visit them in their various offices. These services can be rendered by the consultant from any location to their clients.

Accounting Packages. The consultant will earn money from these services rendered to their clients. Services like sales a of accounting packages, training on how to manage the software and also the installation as well as the setting up of the book of account.

Human Resources Management. Consultants will make money from rendering of recruitment services, training of company staff as well as professional and career development in all field.

Self-publishing in Amazon. The consultant that can create content in writing and in video are position to make money from just publishing e-books for sales online.

In summary, consultancy is a profitable business where an expert can earn money from several sources. To learn area where an expert can earn more money, then watch the video below for more information.

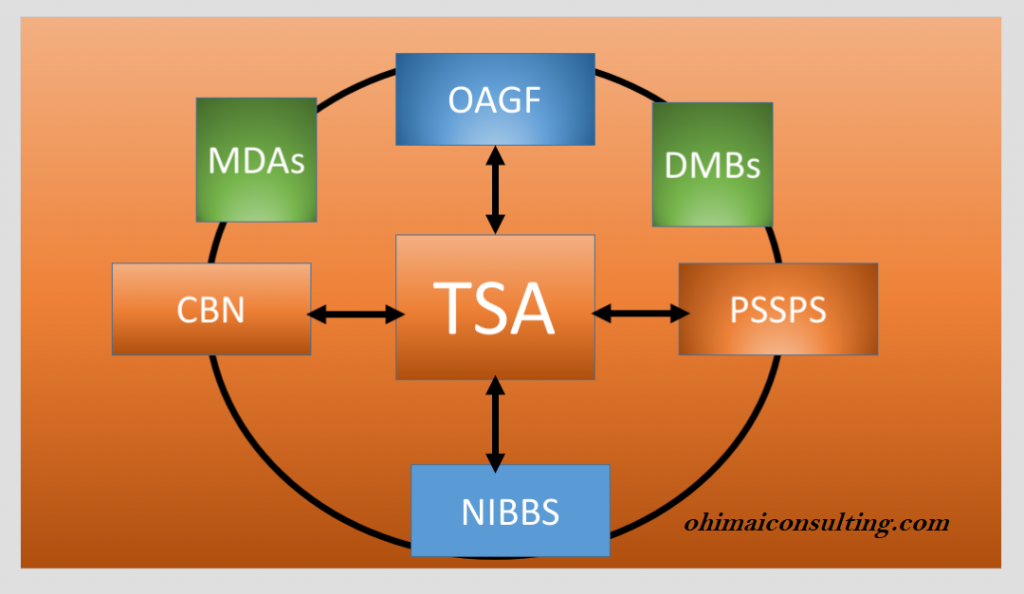

E-Collection is electronic collection of government revenue. Therefore, E-Collection through Treasury Single Account received new development since inception.

However, some of the improvement to e-collection are in line with Central Bank of Nigeria (CBN) circular of 10th December 2020.

New Development of E-Collection/TSA implementation in Nigeria

1. New TSA cost of E-Collections for payer and Ministries, Department and Agencies (MDAs). The charges are grouped into two.

(A). Transaction charges borne by the payer. i) If the payment is received through Point of Sales (POS), it will attract N150 plus 0.50 per cent of the amount being paid subject to a maximum of N1, 000 per transaction.

ii). If payment is received through other channeled, it attracts N150 exclusive of Value Added Tax (VAT)

(B). Transaction charges borne by the MDAs.

(i) They provide the platform for collection.

(ii) They will process all data about the payment and the payer.

(iii) They transmit the data and replicate them and lastly

(iv) Fund sweeping. For this, stakeholder below is to receive fromPayment Solution Service providers (PSSPs) or Deposit Money Banks (DMBs) fund sweeping. This depends on who is playing the collection role for the MDAs. NIBBS is to receives 10% while Office of the Accountant General of the Federation (OAGF) to receives 2.5%.

2. New TSA sharing formula for collection cost received among the various stakeholders as follows:

PSSPs——————————-43%

Collecting Banks——————33%

CBN———————————11%

NIBBS——————————-10.5%

OAGF——————————–2.5%

3. The government link the revenue generating agencies to TSA portal through (PSSPS). PSSPs are companies appointed by government to collect TSA payments from ministries departments and agencies (MDAs).

As at today, payer has to initiate payment from the receiving agencies portal. The way to initiate is to get register or enrolled in the receiving agencies portal.

Requirement to Sign Up for E-Collection/TSA Platform

For E-Collection platform to be effective, these requirements are essential:

a. Provide Tax Identification Number (TIN) and certificate

c. Wait for account to be approved by the receiving agencies

Then, payer cab initiate payment from payer personal account in the receiving agencies portal

Payer will automatically transfer to TSA portal from the receiving agencies portal, for instance Remita

4. Time to Initiate Payment

Payer can only initiate Payment into TSA only when step 3 is being completed.

5. Stakeholders

The addition of Etranzact, Interswitch to join SystemSpec (the operator of Remita) to collect government revenue.SystemSpec has acted as a sole PSSPS appointed by government to collect TSA payments from MDAs.

6. Electronic Payment Companies

The main electronic payment companies involved in TSA increased to four companies. They are Etranzact, Interswitch, SystemSpec and Nigeria Interbank settlement System (NIBSS).

Therefore, NIBBS ensures that all the relevant stakeholders comply with the framework and also communicate collection codes for remittance to PSSPs.

Conclusion

Ogbonna and Ojeaburu (2015) in their study recommended among others, that the government should strengthen Government Integrated Financial Management Information System (GIFMIS) module. Also, cover other area of interest in the national budget to achieve economic development. Moreover, more need to be done to ensure E-Collection are active in all MDAs.

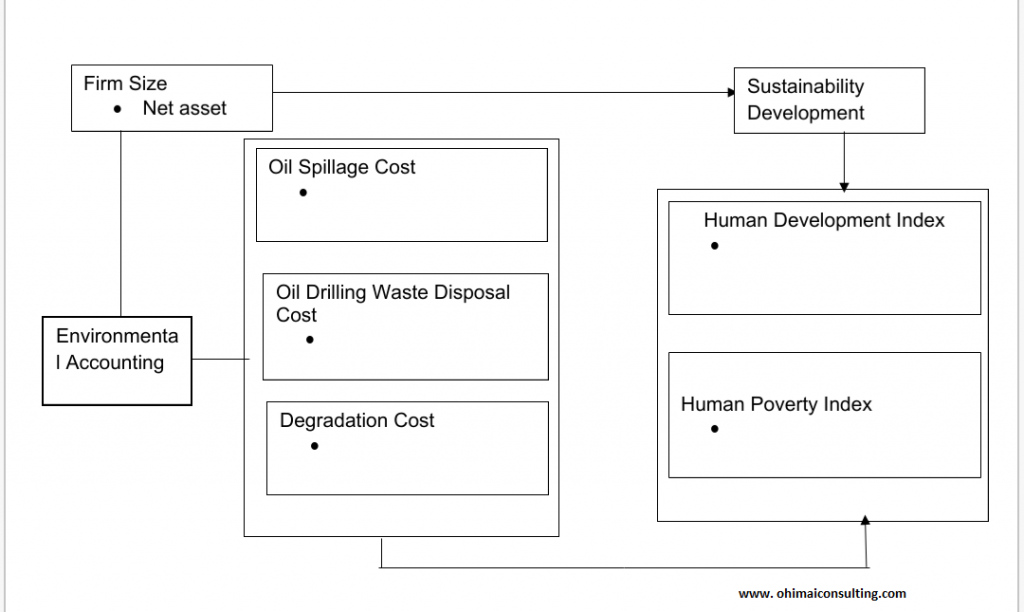

Conceptual framework is dealt with in this post. In line with theoretical foundation and previous research related to this study, a conceptual framework that describes the relationship between environmental accounting and sustainability development in Nigeria. The independent variable (predictor variable) used are oil spillage cost, oil drilling waste disposal cost and degradation as dimensions while the dependent variable (criterion variable) used are human development index and human poverty index as measures.

ohimaiconsulting

Figure 1:1 Conceptual framework of environmental accounting and sustainability development in Nigeria

Sources: (List all your source.)

Note

Indicators

Some school will require you list out the indicators as a bullet under the dimensions of independent variables and measure of dependent variables. Ensure all the indicators are discussed in chapter two (i.e. literature review). One essence of indicator is that it will increase the literature of your work. It will also make it easier for someone to see at glance the direction of your work.

Source of Reference

The essence of the source of reference is because someone may have use one of the dimensions of independent variable and measures of dependent variable before now. So, you have to reference those author accordingly.

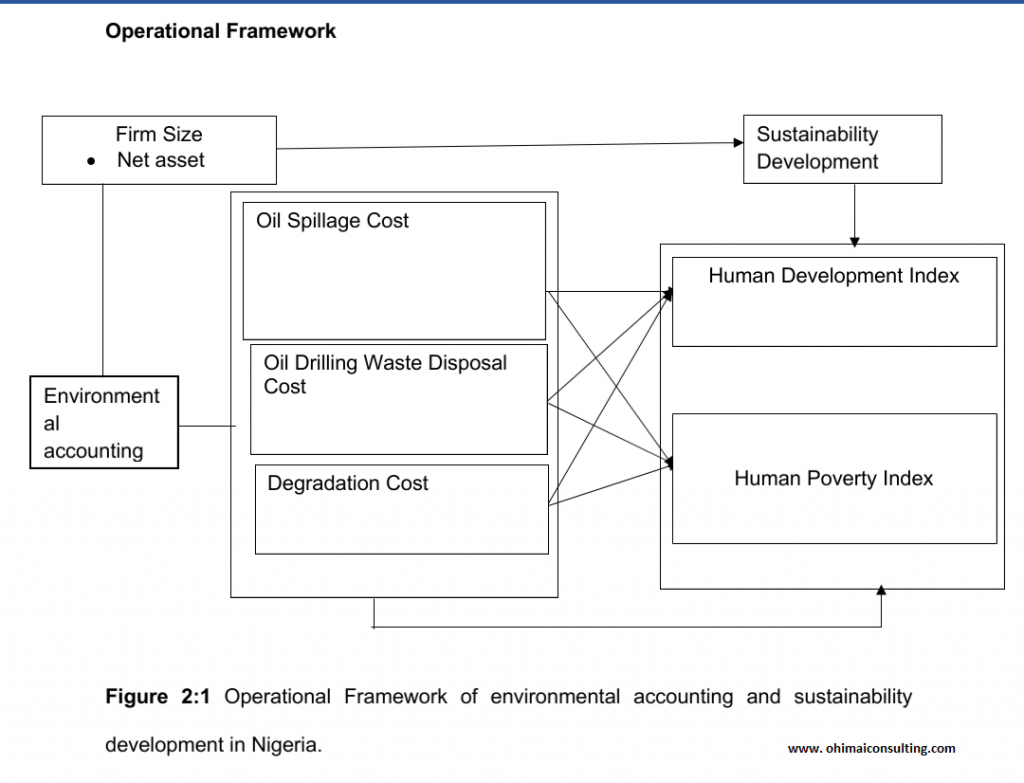

Operational Framework

ohimaiconsulting

The model in Figure 2:1 above, showed the relationship between environmental accounting and sustainability development in Nigeria. Environmental accounting is the predictor variable with the following dimensions oil spillage cost, oil drilling waste disposal cost and degradation, while sustainability development in Nigeria is the criterion variable with a measure as human development index and human poverty index, whereas the moderating variable is firm size. The directions of the arrows shows the direction of the study relationship. The operational framework thus, illustrates the hypothesised relationship with each arrows representing a study hypothesis. In the operational framework each of the dimensions of environmental accounting are linked to the measures of sustainability development in Nigeria.

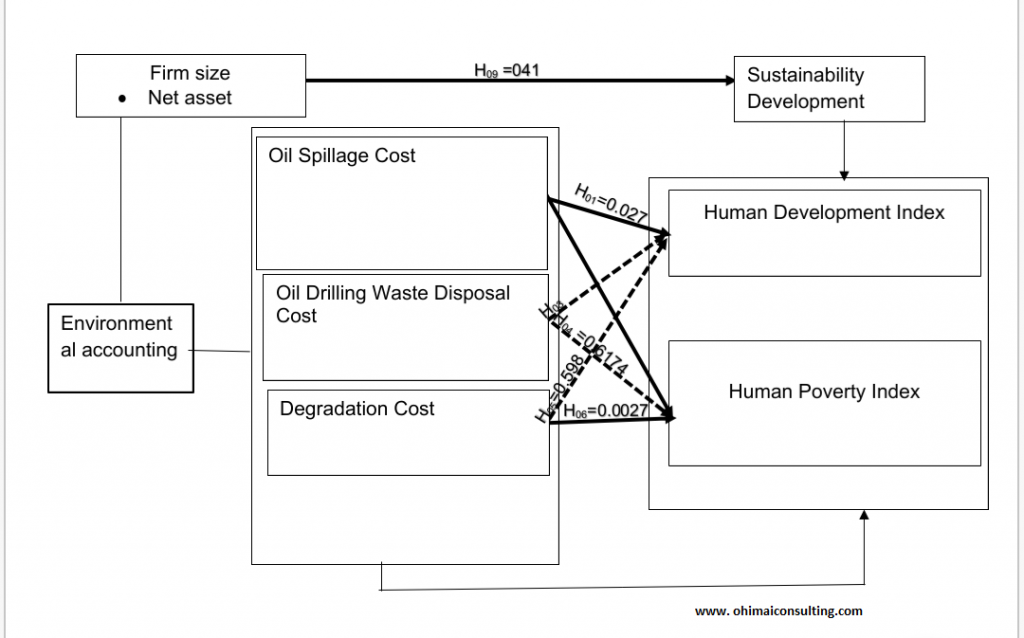

Heuristic Model

This Heuristic Model below is showing the result of the test between the dimensions of environmental accounting and measures of sustainability development in Nigeria.

ohimaiconsulting

Figure 5.1: Heuristic model of environmental accounting and sustainability development in Nigeria

Key

Bold line indicates strong positive significant relationship

This heuristic model in figure 5:1 shows the result of this study based on the hypotheses tested. The framework used an arrow to explain the relationship between variables that is significant and insignificant.

Conclusion

The design of conceptual framework, operational framework and heuristic model are dynamic in nature. All the design does not need to follow this pattern.

Always find out from your school the accepted design. This information shared will guide you as a researcher and student of higher institution in producing a better thesis and publications.

Master program on international finance is for Master student in foreign universities. You are required to prepare/submit an individual report discussing the following:

Choose a Multinational Enterprise (MNE) listed on an internationally recognised Stock Exchange (including for example, London, Dublin, New York or Paris). You are required to:

a. Critically discuss two recent developments in the international financial environment which appear to have impacted on your chosen company’s recent performance and development. Analyse how these two developments are likely to impact on the company in the near future. (14 marks)

b. Discuss the following key elements of the MNE’s international financial and/or risk management strategy (and how they appear to have affected the financial performance of your chosen company): · Sources of finance · Dividend policy (14 marks)

c. With reference to your chosen Multinational Enterprise (and using the most recent annual report published), analyse the financial performance (in terms of profitability, liquidity, efficiency and investment) of the company in the two most recent consecutive financial periods (e.g. 2018/19 or 2019/20, ) using 8 different accounting ratios (prior year comparative figures will be available in the annual report). (32 marks).

Notes:

(i) You must advise your tutor of your chosen multinational enterprise to ensure suitability for use and avoid duplication

(ii) It is advisable to choose your multinational enterprise and download the most recent annual report. This will facilitate your preparation and allow you to effectively participate in weekly class activities;

Master program on International finance Guidelines 1)

The assignment may take the form of an individual written word-processed briefing report of not more than 2500 words, including title page, contents page, in-text references and citations, but excluding tables, reference list and appendices

Part of Solution to the Question

1 Introduction

Honda is a Japanese company that specialize in the manufacturing of automobiles, motorcycles and power equipment with headquarter in Tokyo, Japan (Honda, 2021a; Forbes, 2021). Honda made a net profit of ¥509,932 million and ¥695,444 million in 2020 and 2021 years respectively.

Honda is ranked 39 among the top 100 companies in the Fortune Global 500 list (Fortune 500, 2021). The financial performance and developments are analyzed, explained and outlined, including how it copes with the risks linked with its sources of finance and dividend policy.

2 Section A: Current developments

2.1 Development One—Covid-19 Pandemic

The covid-19 pandemic impacts the financial performance of Honda to the extent that its production activities were affected (Honda, 2021a).

2.2 Development Two—Chip Shortage

Honda was affected by the global microchip shortage. This caused Honda and other major brands to slowdown vehicle production and caused sales drop by 50%. This development made Honda to have low inventory and prompted their prices to rise (Hesketh, 2021). Over 100,000 vehicles were affected last years due to this chip shortage (Reuters, 2021).

The benefits of ICAN certificate to all area of our lives are enormous. ICAN, whose membership comprises of accountants, auditors, and accounting technicians. It was established in 1965 by Act of Parliament No. 15 of 1st September 1965 (the ICAN Act) (icanig.org). Since then, it has improved the lives of its members and the nation in general.

Being a member of ICAN make you become a professional in accountancy. Opportunities will be available to you when you become a full member of ICAN. A lot of information will be available to you to create wealth.

In the public sector, apart from increase morale and a sense of achievement, there are other things to enjoy. This report looked at two things that are considered benefits of ICAN certificate. If you are a qualified member of ICAN before you got employment cadre of the Federal Government of Nigeria, these are your benefits.

Entry-level with ICAN certificate

This means the moment you are qualified as a chartered accountant before gaining employment in the public sector, you have a chance to start in Grade Level 10.

ICAN members with certificate will still be considered for employment in the public sector in line with the provision of the existing scheme of service even without them having a first degree.

It is only ICAN and other related qualifications prescribed in the scheme of service considered for civil service appointment without a first degree.

The entry point for every ICAN member is GL 10.

Advancement of ICAN qualified members

Advancement means moving an officer up from one rank to a higher one within his class or cadre. It is not the same with conversion.

An officer who is on a Grade Level 08 advanced to Grade Level 10. It is a way, a type of promotion. The officer must possess the qualification, which the scheme of service stipulated for holders of that office.

In the case of ICAN members’ already in service, whose grade is below Grade Level 10 and who obtain ICAN qualification is qualified to be advanced to Grade level 10.

The moment that employee sits for ICAN exams and qualify. He or she is qualified to notify his or her employer of the new qualification for considerations.

Ordinarily, the promotion would have taken a minimum of 6 years if he or she passes the confirmation and promotion exams. The power of the ICAN certificate can make it possible in two years.

Conclusion

Student of accounting in higher institutions and accounting officers in the service of the Federal Government needs to take advantage of this opportunity that is made available. This qualification needs to be presented before attaining grade level 10. I

NOTE:

This post is not a legal advice. You are to carry out due diligent on your own.