The benefits of ICAN certificate to all area of our lives are enormous. ICAN, whose membership comprises of accountants, auditors, and accounting technicians. It was established in 1965 by Act of Parliament No. 15 of 1st September 1965 (the ICAN Act) (icanig.org). Since then, it has improved the lives of its members and the nation in general.

Being a member of ICAN make you become a professional in accountancy. Opportunities will be available to you when you become a full member of ICAN. A lot of information will be available to you to create wealth.

In the public sector, apart from increase morale and a sense of achievement, there are other things to enjoy. This report looked at two things that are considered benefits of ICAN certificate. If you are a qualified member of ICAN before you got employment cadre of the Federal Government of Nigeria, these are your benefits.

Entry-level with ICAN certificate

This means the moment you are qualified as a chartered accountant before gaining employment in the public sector, you have a chance to start in Grade Level 10.

ICAN members with certificate will still be considered for employment in the public sector in line with the provision of the existing scheme of service even without them having a first degree.

It is only ICAN and other related qualifications prescribed in the scheme of service considered for civil service appointment without a first degree.

The entry point for every ICAN member is GL 10.

Advancement of ICAN qualified members

Advancement means moving an officer up from one rank to a higher one within his class or cadre. It is not the same with conversion.

An officer who is on a Grade Level 08 advanced to Grade Level 10. It is a way, a type of promotion. The officer must possess the qualification, which the scheme of service stipulated for holders of that office.

In the case of ICAN members’ already in service, whose grade is below Grade Level 10 and who obtain ICAN qualification is qualified to be advanced to Grade level 10.

The moment that employee sits for ICAN exams and qualify. He or she is qualified to notify his or her employer of the new qualification for considerations.

Ordinarily, the promotion would have taken a minimum of 6 years if he or she passes the confirmation and promotion exams. The power of the ICAN certificate can make it possible in two years.

Conclusion

Student of accounting in higher institutions and accounting officers in the service of the Federal Government needs to take advantage of this opportunity that is made available. This qualification needs to be presented before attaining grade level 10. I

NOTE:

This post is not a legal advice. You are to carry out due diligent on your own.

Relevance of Source Documents to organizations cannot be over emphasized. It is important to an accountant and organization in the event of fraud.

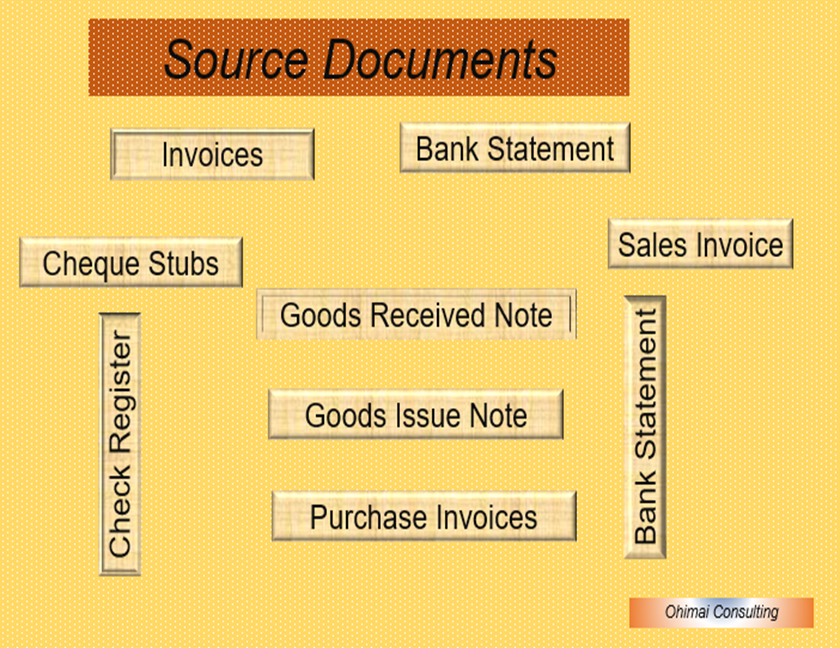

Relevance of Source Documents

1. Audit Trail

Audit trail is a set of accounting documents that authenticate the transactions you record in your accounting books. Furthermore, it provides evidence that transaction has occurred. Also, during audit, source documents serve as back up for accounting journals and ledgers. Every business owner is responsible for recording the company’s transactions. Moreover, the relevance of source document to audit trail is such that it must have to include information about what the event was, who created the event, and the day and time the event happened.

2. Full Details of Transactions

It reveals all the basic fact about the transaction such as the amount of the transaction, to whom the transaction was made, the purpose of the transaction. Also, the date of transaction, serial number of the document, name of document such as Local Purchase Order (LPO), receipt, particular of person issuing the document, particular of person authoring the document, name of company/department issuing the document and name of company/department receiving the document.

3. Internal Control System

Internal controls system are the devices, rules, and measures effected by a company. This internal control ensures the integrity of financial and accounting information, uphold accountability, and prevent fraud. Source document is a good internal control mechanism.

4. Assist Accountants

Source documents assist accountants to prepare financial statement which auditor need for investigation. The movement starts from source documents to journalize transactions. In addition, posting is the process of transferring journal entries to the general ledger or subsidiary ledgers, depending on the needs of a company, by account.

5. Reference

In the accounting world, source documents include purchase order, sales invoice, bank statement, and receipts.

Source documents are created any time a business spends or receives money. However, when there is a report of any investigation into a transaction says fraudulent withdrawal from the bank, the bank statement which is one of the source documents will serve as reference point.

6. Correct Errors

Sources document one will be able to verify whether or not an accounting entry is accurate or correct. It is used to correct errors and omission of transactions. Also, situation where staff will deliberately omit or cause error to occurred will be detected with the investigation of the source documents.

7. Reconciliation

Source documents helps to reconcile with the balances in accounts to see if some documents have not been recorded. Also, if some transactions recorded in the accounts do not appear to have any supporting documents. Frequent reconciliation of account will help to reduce fraudulent activities.

Conclusion.

The relevance of source documents to checkmating fraud is such that organization will need to monitor. That will ensure the right thing is done with the available resources.

There are basic assumptions which underline the preparation of financial statements of business enterprise. There are stated below:

Going concern concept: accounting assumes that the business will continue to operate for a long period of time. In other words, it means continuity in business or Continuity Assumption.

The continue preparation of financial statement in accordance with International Financial Reporting Standard (IFRS) is an evidence of going concern. Even the auditor may also carry out investigation see that the going concern is intact.

Example of going concern is prepayment and accrual of expenses. The company accept these expenses because they believe the business will continue to run. If for example any part or section or department or product line is discontinue, it does not means there is no longer a going concern. Going concern is for the entire company.

During Covid19, a lot of companies had financial issues and were unable to pay their obligation. Various government gives those companies a bailout and a guarantee of all payments to creditors. The companies are a going concern despite of its current weak financial position. But if government imposes a restriction on the manufacture of a certain goods and service for the period say 1 year. Then the company will no longer be a going concern since they might not be able to sell any product.

2. Entity concept: This accounting concept separates the business from its owner. Meaning the business is a legal entity. It can sue and be sued. It also means the owners of a business are limited to how much he has invested not his personal resources. So for example, if the owner brings in additional capital into the business, we will treat this as a liability on the balance sheet of the business.Entity concept ensures that each company is tax separately.

Let look at these examples, Mrs. Ese bought a building having 5 office space for $5000 per month. She uses three office for his business and two for personal purpose. In line with business entity concept, only $3,000 (the rent of two offices) is a valid expense of the business

Another example is when owner of a business lends loan to his company. It would be strictly recorded as a liability and that has to be paid back to the owner.

3. Matching Concept:This concept states that the revenue and the expenses of a transaction should be included in the same accounting period. So to determine the income of a period all the revenues and expenses (whether paid or not) must be included. The matching accounting concept follows the realization concept. First, the revenue is recognized and then we match the costs associated with the revenue. So costs are matched with revenue, the reverse would be an incorrect system.

4. Dual concepts: this says that there are two aspects of accounting. It is represented by the assets of the business and liabilities (i.e. claims against it). Assets =liabilities + capital. So for example. Say the business buys an asset worth N10, 000. So now the Fixed Assets of the company will increase by N10, 000. But at the same time, the bank or cash balance will reduce by N10, 000 and so the transaction will have a dual effect in accounting. And also the Balance Sheet will stay balanced.

5. Realization concepts: in accounting, profit should not be recognized until the goods are passed to the customer.

6. Money measurement concept: Accounting is only concerned with the facts that can be measured in monetary terms with fair degree of objectivity. Accounting does not record that the firm has a bad or good management team, poor morale among staff. So for example, if the company underwent a major management overhaul this would have no effect on the accounting records. This concept is actually one of the major drawbacks of accounting.

7. Accrual concept: Revenue and cost are usually recorded in accounts when they are earned or incurred rather than when the money is received or paid.

8. Full Disclosure Concept: This concept states that all relevant information will be disclosed in the accounting statements. A lot of external users depend on these financial statements for their information to make investing decisions. So no information/transactions etc of relevance to any one of them will be omitted from these statements for the benefit of the company.

9. Cost Concept: This accounting concept states that all assets of the firm are entered into the books of account at their purchase price (cost of acquisition + transport + installation etc). In the subsequent years to, the price remains the same (minus depreciation charged). The market price of the asset is not taken into consideration.

10. Accounting Period Concept:Every organization, according to its needs, chooses a specific period of time to complete an accounting cycle. Generally, the time chosen is a year we call the accounting year. The time period is mentioned in the financial statements.

11. Substance over form: usually transactions are recorded and accounted for by their commercial realities rather than their legal form. Substance over form is an accounting concept which means that the economic substance of transactions and events must be recorded in the financial statements rather than just their legal form in order to present a true and fair view of the affairs of the entity.

12. Faithful representation: For financial report to be useful, the financial information must not only represent relevant phenomena but must faithfully represent the phenomena that it purports to represent.

13. Timeliness: It means having information available to decision makers in time to be capable of influencing their decisions. The older the information the less important it become.

14. Relevance: Relevant information is capable of making a difference in the decisions made by users.

15. Comparability: The information about a firm is more useful if it can be compared with similar information about other enterprise and with similar information about the same enterprise for another period or date.