Purchase orders (PO) are essential for an accountant to help achieve financial goals and is one of the key Source Documents in Accounting. The buyer sends these orders to the vendor or sellers or suppliers, outlining what they expect for the order and when it should arrive. In contrast, a sales order generated by the supplier and sent to the buyer. Additionally, the supplier generates an invoice to show the buyer how much they owe for the purchased goods.

Benefits of Purchase Orders (PO)

Controlling the procurement of products and services from external suppliers is easier with purchase order.

The inventory process is more accessible with the help of PO. Once the supplier receives the PO, they will retrieve the items listed in the PO from their inventory.

The Purchase Order acts as a legal document that helps prevent future transaction disputes.

It prevent duplicate orders by keeping track of order and from whom, which can be challenging when a company decides to scale its business.

Overall, a well-organized purchase order system helps simplify the inventory and shipping process by keeping track of incoming orders.

The process of initiating a purchase order should begin with:

When a buyer needs goods, they start by creating a purchase requisition. This document helps to keep track of the items ordered and is sent to the purchasing department within the company. It also helps the company keep track of expenses. The acountant can only create purchase order once an authorized manager has approved the purchase requisition.

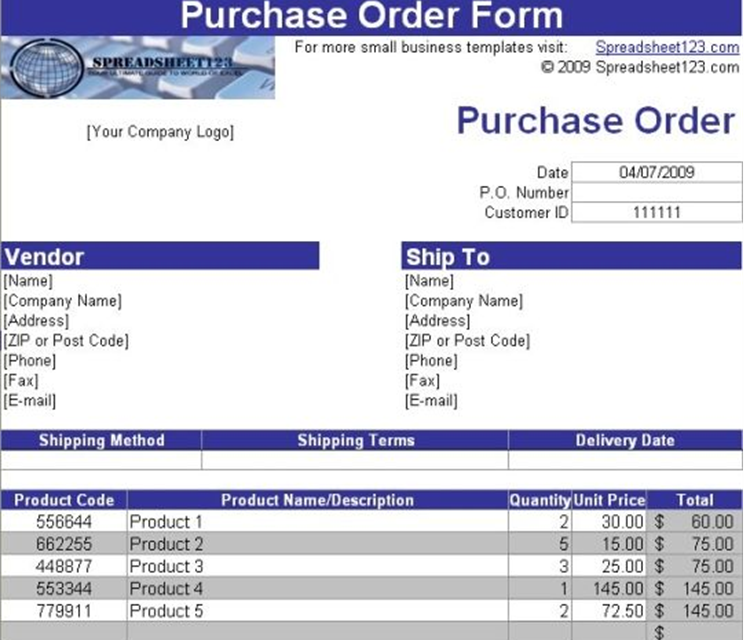

Once the buyer has confirmed the goods they wish to purchase, they will initiate a PO. This document will include the date of the order, FOB shipping information, discount terms, buyer and seller names, a description of the goods under process, item number, price, quantity, and the PO number as shown in the attachment.

The seller can accept or reject a PO with all the transaction and buyer’s requirements. If the seller agrees with the PO, it becomes a legally binding contract.

Keeping a record of the purchase order is crucial for buyers. The demand remains active until the company receive all or part of the goods.

Goods Receive Note (GRN) is issue after successful delivery from suppliers. Each order has an assigned unique number associated with the Purchase order number. The accountant can use this number to ensure that the goods received match those ordered and listed on the GRN.

Before company accountant make payment, they will verify that the Purchase order number matches the invoice. This ensures that the charges to pay by the buyer are the correct amount for the goods before processing the payment.

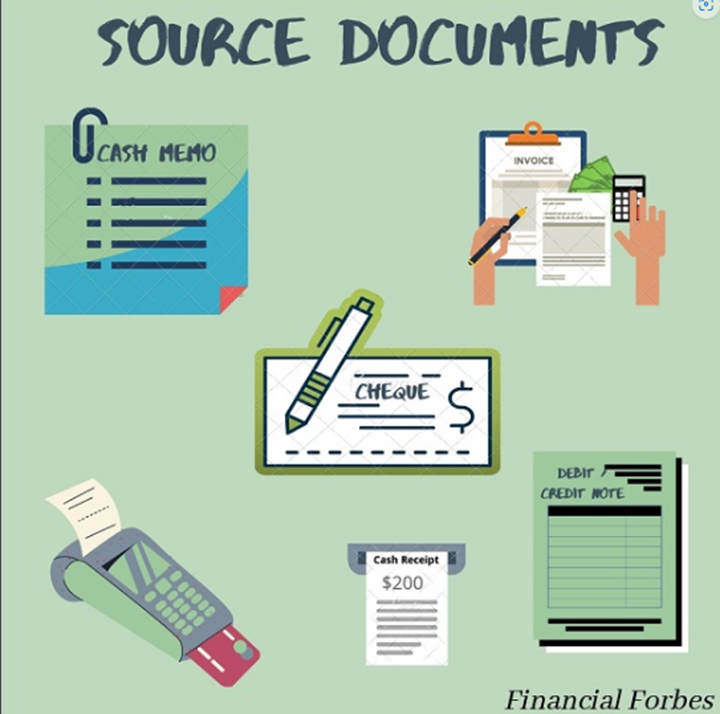

Top 35 Source Documents in Accounting are relevant to help accountant to help accountant in their job. Also, it is a document that serves as proof of transactions that is available in apps that provide such services.

Top 35 Source Documents in Accounting stated below:

The buyer sends this to the vendor. They will then outline exactly what the order should contain and when it should arrive.

2. Sales Invoice

This is a process for managing account receivables. When the seller gives out goods, they will provide a document containing all relevant sale details.

3. Purchase Invoice

This is made for account payables. The seller will enter this as sales invoice while the buyer will enter it as purchase invoice.

4. Debit Note

This is evidence of reduction in purchases and can be useful to support purchases return journal. Furthermore, in customer books, debit note will reduce how much they owe to the seller.

5. Credit Note

This is evidence of reduced sales and support sales return journal. In addition to supplier’s books, credit note reduces the amount owed by the customer.

6. Cheque

This is a special bank note that represents the cash paid by the customer.

7. Revenue receipt

This is used to record the receipt of cash which is a proof that the payment is made.

8. Cash register receipts

This is a business paper that listed the money coming in from customers.

9. Bank or Credit advice

They are debit or credit bank advice. Bank credit advice is bank documents informing the business of an increase made in the business’s bank account. Unlike bank debit advice that is opposite to bank credit advice.

10. Deposit slips

When one receives cheque or cash from customer, the seller will take it to the bank and present.

11. ATM cards

The production of receipt from ATM machine can serve as evidence that money has been taken from the bank account.

12. Bank statements

This is a summary of financial transactions that occurred at a certain institution during a specific time period. For example, a typical bank statement may show your deposits and withdrawals for a certain month.

13. Bill of exchange

This is an unconditional order in writing, addressed by one person to another, signed by the person giving it. It also require the person to whom it is addressed to pay on demand.

14. Payroll report

This can also refer to the list of employees of a business and the amount of compensation due to each of them.

15. Cancelled Cheque

This is a check that has been paid or cleared by the bank

16. Cheque Stubs

This is the check kept by the payee with information such as the check number, date, and amount.

17. Employee Timecard

This is a method for recording and tracking the amount of an employee’s time spent on each job

18. Board minutes or minutes of meetings

The secretary of the board usually takes minutes during meetings.

19. Goods Dispatched Note (GDN)

This a document of the company that lists the goods sent out to a customer. Without a doubt, the company will keep one record of goods dispatched notes.

20. Goods Issues Note (GIN)

This is a physical record of the movement of goods or materials from the warehouse or store to production department.

21. Stock take Records

This is also called stock counting. It is when you manually check and record all the inventory that your business currently has on hand

22. Stock Record

A Bin Card is a card indicating quantitative records of the receipts, issues and balances etc.

23. Goods Received Note (GRN)

This is source document that shows the goods that a business has received from a supplier.

24. Remittance advice

This source document can confirm the amount paid and shows discrepancies that can easily be investigated.

25. Insurance Endorsement Certificates

This is where one party will add the other party as an “additional insured” on their commercial liability insurance policy.

26. Point of Sales Summaries

This can be used to record a number of sales at a cash register.

27. Memorandum

Memo is a written document businesses use to communicate an announcement, policy changes, price increases or notification to take an action, such as attend a meeting, or change a current production procedure.

28. Computer-generated Receipts

This is the kind of receipts is to be generated by the computer.

29. Lease Agreement or Rental Agreement

Lease contracts are formal documents that identify the lessor, lessee, what’s being leased, whether it’s an asset or a property.

30. Sales Tax Returns

This is the taxpayer’s document of declaration. This will enable the taxpayer to furnish the transaction details during a tax period and deposits his Sales Tax liability.

31. Cash Register Tapes

This allowed one to keep a record of all customer transactions and/or provide them with a receipt.

32. Adjustment Notes

This are issued to customers due to damaged, returned or undelivered goods

33. Employee Pay Advice

This source document that can helped to provide written evidence concerning employee income.

34. Payroll Advice Report

This payroll reports helped small businesses understand payroll costs and summarize payroll data.

35. Evidence of Sale or Disposal of Assets

This is the removal of a long-term asset from the company’s accounting records.

Conclusion

Indeed, all these top 35 source documents in accounting are integrated in several apps that offer such accounting services. Moreover, this App made it possible to have all these source documents in one place to make the accountant job easier and simple.

Kindly add your own source documents to the Top 35 Source Documents in Accounting listed above. This will help us to update our records accordingly.

Watch several videos of how to prepare financial statements from source documents

Some of the best consultancy services any expert can specialize on are financial and auditing services, tax management services, education services, cloud computing, accounting packages. Also, human resources management and career development, business and marketing development, professional training services, books and journal publication, self-publishing and lot more.

Kind of Consultancy services rendered by Ohimai Consulting

The selected list is among the best consultancy services as discussed below.

Financial and auditing services. The consultancy will ensure that accounting and auditing of all their clients are handled professionally.

Tax management services. The consultant manages all the taxes such as Pay-As-You-Earn (PAYE), company income tax, tax return fillings, creation of Tax Identification Number, VAT management, tax clearance, stamp duty. the consultant will ensure that all their clients don’t default or violate the tax law but ensures full compliance of their civil right and obligation.

Educational Services. The consultant through the consultancy services will render helps to students and non-students in foreign land. Through these services, Ohimai Consulting now mentored students in the foreign universities.

Cloud Computing. The consultant will be able to manage several firms without having to visit them in their various offices. These services can be rendered by the consultant from any location to their clients.

Accounting Packages. The consultant will earn money from these services rendered to their clients. Services like sales a of accounting packages, training on how to manage the software and also the installation as well as the setting up of the book of account.

Human Resources Management. Consultants will make money from rendering of recruitment services, training of company staff as well as professional and career development in all field.

Self-publishing in Amazon. The consultant that can create content in writing and in video are position to make money from just publishing e-books for sales online.

In summary, consultancy is a profitable business where an expert can earn money from several sources. To learn area where an expert can earn more money, then watch the video below for more information.

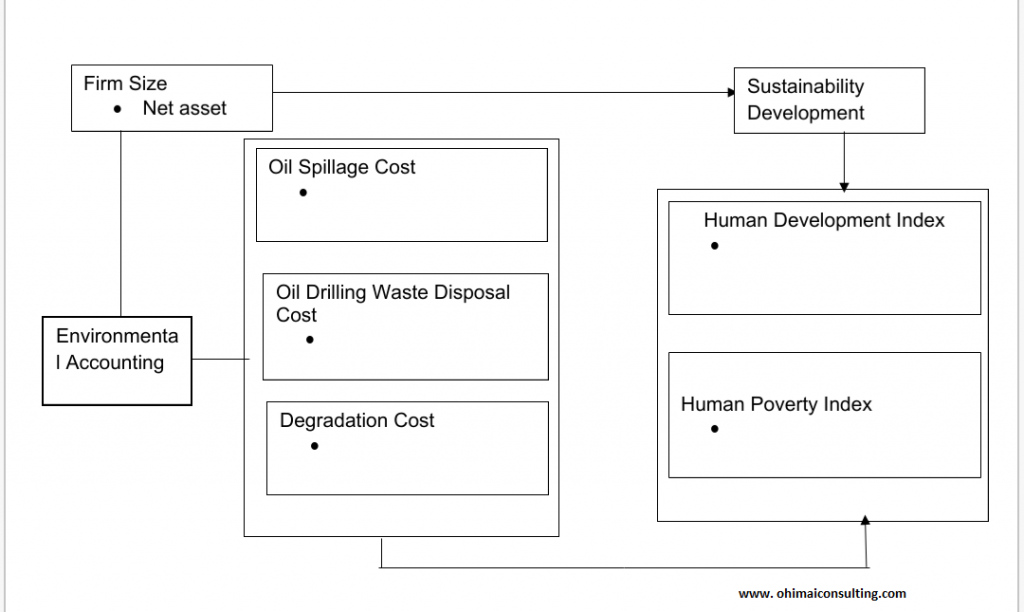

Conceptual framework is dealt with in this post. In line with theoretical foundation and previous research related to this study, a conceptual framework that describes the relationship between environmental accounting and sustainability development in Nigeria. The independent variable (predictor variable) used are oil spillage cost, oil drilling waste disposal cost and degradation as dimensions while the dependent variable (criterion variable) used are human development index and human poverty index as measures.

ohimaiconsulting

Figure 1:1 Conceptual framework of environmental accounting and sustainability development in Nigeria

Sources: (List all your source.)

Note

Indicators

Some school will require you list out the indicators as a bullet under the dimensions of independent variables and measure of dependent variables. Ensure all the indicators are discussed in chapter two (i.e. literature review). One essence of indicator is that it will increase the literature of your work. It will also make it easier for someone to see at glance the direction of your work.

Source of Reference

The essence of the source of reference is because someone may have use one of the dimensions of independent variable and measures of dependent variable before now. So, you have to reference those author accordingly.

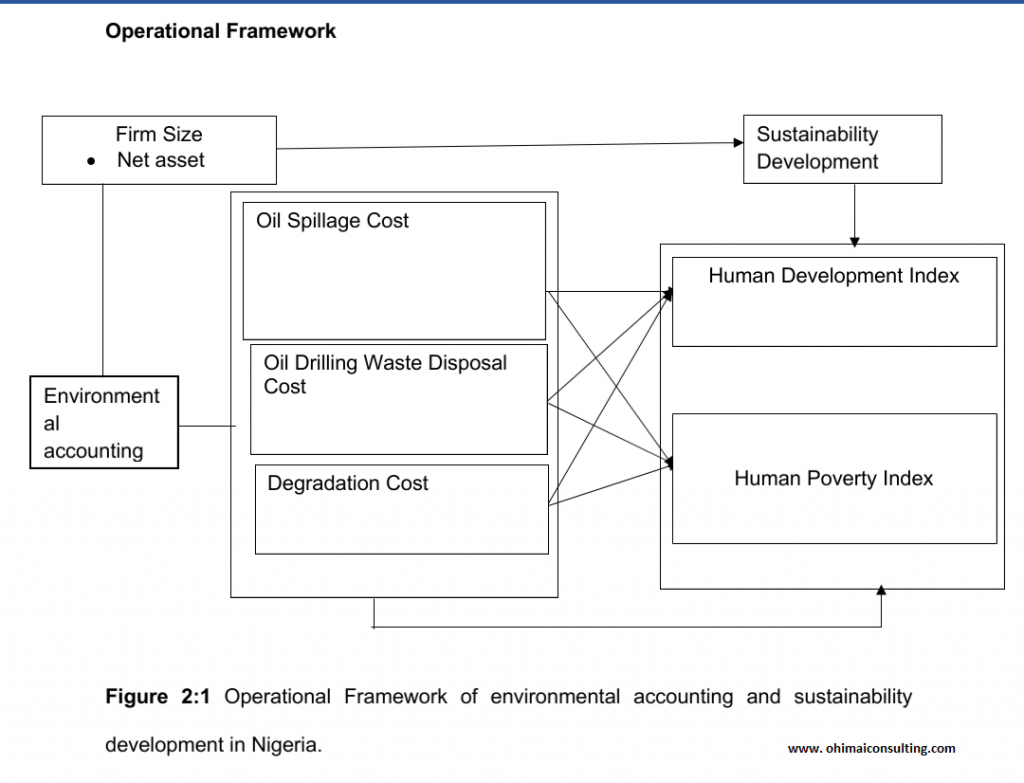

Operational Framework

ohimaiconsulting

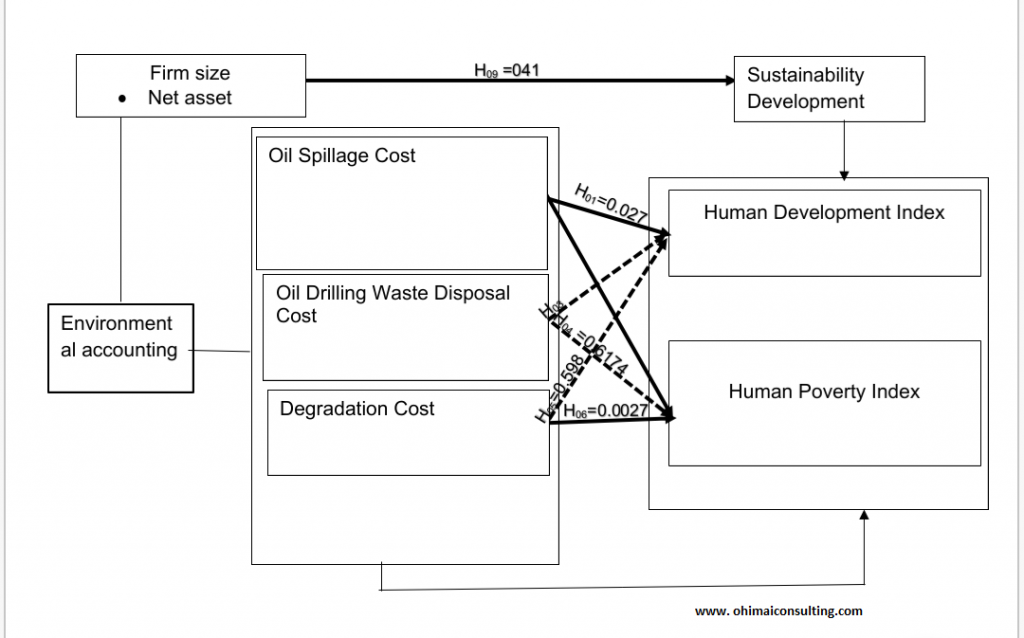

The model in Figure 2:1 above, showed the relationship between environmental accounting and sustainability development in Nigeria. Environmental accounting is the predictor variable with the following dimensions oil spillage cost, oil drilling waste disposal cost and degradation, while sustainability development in Nigeria is the criterion variable with a measure as human development index and human poverty index, whereas the moderating variable is firm size. The directions of the arrows shows the direction of the study relationship. The operational framework thus, illustrates the hypothesised relationship with each arrows representing a study hypothesis. In the operational framework each of the dimensions of environmental accounting are linked to the measures of sustainability development in Nigeria.

Heuristic Model

This Heuristic Model below is showing the result of the test between the dimensions of environmental accounting and measures of sustainability development in Nigeria.

ohimaiconsulting

Figure 5.1: Heuristic model of environmental accounting and sustainability development in Nigeria

Key

Bold line indicates strong positive significant relationship

This heuristic model in figure 5:1 shows the result of this study based on the hypotheses tested. The framework used an arrow to explain the relationship between variables that is significant and insignificant.

Conclusion

The design of conceptual framework, operational framework and heuristic model are dynamic in nature. All the design does not need to follow this pattern.

Always find out from your school the accepted design. This information shared will guide you as a researcher and student of higher institution in producing a better thesis and publications.

Some forensic accountants choose to specialise in Alternative Dispute Resolution (ADR) due to their familiarity with both finances and the legal system. Business litigation can be a very expensive and costly. Generally, opposing attorneys will fight vigorously for their clients. When forensic accountants are engaged as EXPERT WITNESSES in business litigation, such fighting can drive up the cost of the expert witnesses and drive down the understanding of the forensic accountant’s work and, therefore, the client’s satisfaction with the forensic accountant.

In a typical business litigation scenario, the opposing attorneys may fight against providing information which the forensic accountant has requested in order to calculate damages or to perform a business valuation. Depending on the amount of rancor between the parties and level of antagonistic determination between the attorneys.

There are times he may have to perform the damage calculation or business valuation without all the relevant information he believes is necessary. In the absence of such information, the forensic accountant may have to make reasonable assumptions regarding the missing information. If there are differing assumptions by each side’s expert witness, significant differences in damage calculation or business valuation amounts may result.

In such situations, the parties often may expend significant time and incur significant costs in using these forensic accounting experts. Especially when there are significant differences of opinion between the two expert witnesses, the experts’ fees and attorney fees can be even higher. Both parties also may come away with confusion and misunderstanding regarding how the relevant damage amount or business’s value was determined.

This is because they may only speak with the expert retained by their attorney and must rely upon the deposition and/or courtroom testimony of the opposing expert without being able to ask their own questions. The use of alternate dispute resolution – such as mediation, arbitration, and negotiation – not only can reduce the cost of traditional business litigation, but also can help eliminate the uncertainty that comes from leaving the resolution of the dispute up to the Courts (judge or jury).

Examples of disputes that are prime candidates for alternate dispute resolution includes: • Business contract disputes • Shareholder/partner disputes • Employee termination disputes • Insurance claims • Royalty payment disputes • Patent/trademark disputes • Business merger and acquisition • Local disputes, • Global disputes,

How the role of the forensic accounting expert differ in Alternate Dispute Resolution (ADR) • First, the forensic accounting expert can be jointly retained by both parties as opposed to by just one party in traditional business litigation.

• Next, because of the joint retention of the forensic accounting expert, both parties are more cooperative and better able to share all the necessary information needed by the forensic accounting expert. Thus, there is also usually less of a need to make assumptions.

• Finally, the expert witness report can be openly reviewed with both parties. Because this is a joint retention, the forensic accounting expert can be more open and informative with both parties and stand ready to fully answer either party’s questions. This helps to eliminate confusion and lack of understanding regarding the damage calculation or business valuation and the forensic accounting expert’s process.

• Additionally, the cost for the forensic accounting expert will be less, because only one expert is retained instead of two, and because the cost of depositions and/or courtroom testimony can be eliminated.

The Role of the Forensic Accountant In Mediation A forensic accountant has a number of possible roles to play, which are discussed below.

Expert Accountant acting as a Mediator. Accountants may play a role in a dispute by acting as a mediator. For example, disputes involving business valuations, application of technical accounting standards or which require business acumen and experience in a particular industry or sector may benefit from having a mediator with the requisite expertise in these areas.

The Forensic Accountant’s role in calculating damages and attending the Mediation. In complex commercial disputes requiring an expert opinion on the quantum of damages, for example in a case whereby one party may have suffered a loss of profits following a breach of contract by another party, a forensic accountant may be retained as an independent expert to provide an independent assessment of the amount in dispute. In such a case the forensic accountant may be requested to prepare an expert report, attend a meeting of experts with an opposing expert, or advise their client on a range of their potential losses depending on a number of factors or assumptions. In mediation, the forensic accountant can provide a similar role, assisting a mediator in dealing with and understanding complex financial issues.

Forensic accountant role to serve as appointed receiver or monitor

Forensic accountant role as Consulting or testifying expert

Forensic accountant role as impartial neutral with specialized expertise

Forensic accountant role as Advisor to party during mediation

Conclusion The philosophy behind Alternative Dispute Resolution is to ensure that parties involve resolve their dispute without anyone of them feel aggrieved. ADR is a good mechanism to resolve disputes among individual and organisation both local and international level. The presenter believes and suggests to us that all avenues available within ADR be explored fully before approaching the court. Even now that so many cases are queuing in the court without definite date of conclusion, is an issue that need immediate action by the government.

Dispute resolution is the process of resolving a dispute between parties. Dispute resolution is also often referred to as “conflict resolution.” There are a number of processes that can be used to resolve conflicts, claims, and disputes.

Therefore, ADR is the procedure for settling disputes without litigation, such as arbitration, mediation, or negotiation. It is also called external dispute resolution (EDR).

ADR procedures are usually less costly and more expeditious. They are increasingly being utilized in disputes that would otherwise result in litigation, including high-profile labour disputes, divorce actions, and personal injury claims.

One of the primary reasons parties may prefer ADR proceedings is that, unlike adversarial litigation, ADR procedures are often collaborative and allow the parties to understand each other’s positions. ADR also allows the parties to come up with more creative solutions that a court may not be legally allowed to impose.

So the philosophy behind ADR is that it offers the parties an opportunity to avoid risks and reduces the likelihood of an unfavorable outcome. It gives the parties in the dispute the opportunity to consider the risks involved in litigation.

Dispute Resolution Processes

Generally, however, most dispute resolution processes are classified as facilitative, advisory or determinative or as ‘mixed’ or ‘blended’, and this article focuses on the more facilitative forms:

(a) Facilitative processes involve a third party, usually with no advisory or determinative role, providing assistance in managing the process of dispute resolution. These processes include mediation and facilitation.

(b) Advisoryprocesses involve a third party who investigates the dispute and provides advice on the facts and possible outcomes. These procedures include investigation, case appraisal and dispute counselling.

(c) Determinative processes involve a third party investigating the dispute, which may include a formal hearing, and the making of a determination that is potentially enforceable. These processes include adjudication and arbitration and may be binding or non-binding.

While there are many reasons why facilitative processes have become more popular in recent years, one critical factor relates to the location of ADR services. Where ADR takes place within the courts or in a court-connected framework, such processes may be more likely to be advisory and be the subject of legal negotiation patterns. Arguably, one reason why facilitative mediation has grown so quickly in Australia is because it is often located outside the court system. While in Australia there has been substantial growth in facilitative ADR both within and outside the court system, in many disputes ADR must be used before court proceedings can be commenced. For example n some cases, court proceedings cannot be filed until a certificate has been lodged indicating that the parties have attended a mediation or in other situations parties must have made a ‘genuine effort’ or made ‘reasonable attempts’ to resolve the dispute before commencing proceedings. Within Australia, the most striking example of an extensive mandatory prelitigation ADR system exists in the family relationships area, and most disputants can expect to attend some form of mandatory ADR before being able to commence proceedings in a court.

.

Modes of Alternative Dispute Resolution (ADR)

Arbitration – This is a method involving one or more neutral third parties who are usually agreed upon by the disputing parties and their decision is final. The decision arrived at by arbitrator(s) is called an award and same is enforceable like a court judgment. The agreement to arbitrate must be in writing, signed, and the agreement is irrevocable except by agreement of the parties or by leave of court (Aduaka & Onnome, 2018). A process similar to an informal trial where an impartial third party hears each side of a dispute and issues a decision; the parties may agree to have the decision be binding or non-binding.

Mediation – This is essentially a non-binding dispute resolution mechanism involving a neutral and impartial third party who tries to help the disputing parties reach a mutually agreeable solution. The third party here is impartial, does not take decisions for the parties rather he helps them in identifying the issues and interests that need to be solved (Aduaka & Onnome, 2018). A collaborative process where a mediator works with the parties to come to a mutually agreeable solution. mediation a form of negotiation with a third-party catalyst who helps the conflicting parties negotiate when they cannot do so by themselves. Mediation is usually non-binding (Khan & Karim, 2017).

Conciliation-The process of conciliation is basically that of mediation. The only difference is that the neutral third party is usually an expert in the field or area of dispute in which he has being called upon to conciliate (Aduaka & Onnome , 2018). This is an ADR process where an independent third party, the conciliator, helps people in a dispute to identify the disputed issues, develop options, consider alternatives and try to reach an agreement. A conciliator may have professional expertise in the subject matter in dispute and will generally provide advice about the issues and options for resolution. However, a conciliator will not make a judgment or decision about the dispute. Conciliation may be voluntary, court ordered or required as part of a contract. It is often part of a court or government agency process.

Negotiation- Negotiation is a process whereby parties discuss and agree to terms or reach certain agreement without the aid or intervention of a third party. Negotiation basically involves some form of „give and take‟ from either parties or some form of compromise by the disputing parties. It is important to note that the law does not prohibit parties to a dispute from engaging in negotiation for the purpose of settling their dispute (Aduaka & Onnome , 2018). This form of ADR is often overlooked because of how obvious it is. In negotiation, there is no impartial third party to assist the parties in their negotiation, so the parties work together to come to a compromise.

Collaborative Law- This is a form of ADR that has grown in popularity, especially in respect of family disputes. In this process, all participants may decide to use a ‘collaborative’ process model whereby lawyers and all experts are trained in interest-based negotiation and are focused on the negotiation process with two-hour meetings and guidelines for gathering and exchanging information (collaborative participation agreements normally require the withdrawal of lawyers and others if the negotiation does not result in an agreed outcome, which means that they cannot be involved in any subsequent litigation). This is common in North America.