The mathematical theory of games was invented by John von Neumann and Oskar Morgenstern (1944). ‘Game theory is the science of rational decision making in interactive situations’ (Dixit & Skeath, 1999). ‘Game theory can be defined as the study of mathematical models of conflict and cooperation between intelligent rational-decision makers.’(Myerson,1991).

Both these definitions focus on the interactive component between the parties. At the heart there are the twin issues of conflict and cooperation. There is the assumption that these decision makers are rational and have specific objectives in mind which in a dispute is to reach a settlement.

Game theory, a mathematical model used in a variety of dispute contexts starts with the premise that the participants, while not knowing fully the position of the other party, are rational and want to achieve the best possible outcomes.

Levine (2019) stated despite the intensity of a dispute, both sides ultimately want to achieve the best possible outcome. Each party has to assume that the other party is rational even though he may not know exactly what the other party wants.

It is in this situation that the third party negotiator’s role becomes increasingly important to help move the parties along in the process of information exchange until they come closer to a common understanding as to what the other person wants.

Game theory provides a new language to think of human behaviour and of parties who are in conflict. Negotiation can be used in the family setting to alter the expectations and preferences of the parties. In game theory, one of the dominant models which has been used to explain the behaviour of individuals is the Nash Equilibrium. In game theory, the Nash equilibrium, named after the mathematician

John Forbes Nash Jr. is a proposed solution of a non-cooperative game involving two or more players in which each player is assumed to know the equilibrium strategies of the other players, and no player has anything to gain by changing only their own strategy (Osborne & Rubinstein, 1994).

The usefulness of the Nash Equilibrium is that it comes to a point where the parties realize that they will need to settle in order to maximize their chance of a positive outcome. According to Levine (2019), the use of game theory is not meant to assume that within it is the solution to real life issues. What it offers is simply a model to understanding conflict situations and analyzing how parties can make decisions that result in positive outcomes.

Conclusion

Game theory shows win-win situation. It can apply in the business environment, to ensure every parties have the reason to smile.

References

Dixit, & Skeath. (1999). Games of strategy. 3

Levine, D. K.(2019). Game theory and the law.(alternative dispute resolution). Retrived on the 25th July, 2019 from the Kmnp Law Website www.Kmnplaw.Com.

Myerson, R. B. (1991). Game theory: Analysis of conflict. Harvard University Press, (1), vii–xi

Osborne, M. J., & Rubinstein, A. (1994). A course in game theory. Cambridge, MA: MIT.,14.

ADR meaning “alternative” to formal court hearings, trials and formal legal proceedings. In fact, many forms of dispute resolution are thousands of years old, dating from Confucian principles of promoting harmony and community, rather than individual, “justice,” in China and then later other Asian countries, or African community dispute resolution processes called “moots” (or in some countries Ubuntuor gacaca), which are mediation like processes in which community elders listen to narratives of the dispute from the parties and either help negotiate a solution with the parties, or, more like arbitration, decide or command some remedy, with the goal of preserving community peace. The goals of such older forms of dispute resolution are to prevent further conflict and escalation of the dispute beyond the parties, to restore the community to peaceful existence.

In the West (Continental Europe and in England), the middle ages saw the movement from “trial by ordeal” (putting disputing parties on a horse to joust, or dropping them into a fire or body of water to see if God would “protect” them and declare the innocent or non-wrongdoer) to trial by evidence. The development of formal rules of evidence was designed to use rational forms of proof and judgement by “peers” (juries) about what had happened to cause the dispute. “Modern” justice meant that judges or juries declared winners and losers (in both civil and criminal cases) so that the guilty would be punished or pay damages and the innocent would be vindicated by using the same rules of procedure and substantive rules of law to everyone (“equal justice under law”).

In the late 20th century this more modern way of achieving “individual” justice caused many court systems to become very crowded (in countries like the US and Italy it could take as much as 5-10 years to get a hearing), and once there, the court and formal trial process became quite expensive, requiring the hiring of lawyers and other professionals (experts) and the paying of high fees.

So in the 1970s two different groups of reformers proposed different solutions to the court delay problem. Some American judges and scholars proposed “alternatives” to court (mediation, arbitration, negotiation, mandatory settlement conference,) to encourage parties to settle their differences quicker and cheaper with out-of-court processes. This was called the “Multi-Door Courthouse,” an idea that people would choose a process and reduce their costs and time in resolving disputes. The US government actually funded a few local court systems to create such multi-door courthouses and many people (lawyers, psychologists and community leaders and social workers) were trained as mediators .

In the last few decades different forms of ADR have gone global—a new field of transitional justice has developed to provide both punishment and reconciliation in post-apartheid, post-civil-war and other post-conflict zones. So although there is now an International Criminal Court for state violations of human and civil rights and criminal prosecutions, in some settings, a form of ADR has been used to create Truth and Reconciliation Commissions (e.g. South Africa, Bolivia, Argentina, Liberia) which are often hybrid institutions that seek the “truth” about what atrocities have occurred, but also try to use various forms of narrative, apologies, forgiveness ceremonies and rituals to attempt to “heal” the past, so newly constituted countries can move forward.

Ironically, or in a return to earlier history, some countries have used older indigenous processes like community moots (gacaca in Rwanda) to attempt to combine justice of the past with peace for the future. These new forms of institutions are hybrid because they draw on both public international law concepts (international criminal law) and national or indigenous processes.

ADR is now widely used around the world to deal with disputes and conflicts as well as agreement-making and planning. At the international level, negotiation (between and among different countries, states and communities are as old as humankind) and is a process now used by the 200 countries in the world to negotiate treaties (which are state commitments to not engage in war or other bad acts, or to positively collaborate on other activities, like poverty amelioration, environmental protection, anti-discrimination, health, education and cultural cooperation).

Modern international legal activity is often conducted in informal networks of negotiation and new forms of international administrative actions, rather than by formal courts or executive diplomacy. Mediation by international officials is now commonly used to try to resolve interstate conflicts before they escalate to war. Mediation and arbitration are both used in both public law and private, commercial law settings. Arbitration is used on an international level to resolve border and boundary disputes, private commercial cross-border disputes, and now disputes involving private investors in foreign countries.

Formal institutions like the World Trade Organization use arbitral processes and investment arbitration now represents a controversial hybrid, using arbitral processes, but relying on more public law principles and demands for transparency. Most informal dispute processes ultimately rely on the enforcement powers of national courts under international treaties, such as the New York Convention for the Recognition and Enforcement of Foreign Arbitral Awards or the Washington Convention for dispute processes for foreign investment disputes with states.

At the level of everyday disputing, the European Union and some national court systems are now promoting various forms of ADR, such as those described here, to reduce long court delays and to provide consumer and even businesses different ways to resolve their disputes, including the promotion of Online Dispute Resolution (computer platforms for trans border and national consumer disputes or disputes between citizens and states).

The expansion of different forms of dispute resolution has led to interesting issues and policy differences about whether conflicts and disputes belong to the parties, so they can privately choose their form of resolution, or whether conflict resolution should remain a public and transparent state function when the impact or precedent of a conflict resolution might be greater than just on the interested parties. This is were the concept of Game theory is necessary in ADR.

References

Andrew, J. P. (2000). Alternative dispute resolution: skills, science, and the law. Toronto, Ontario: Irwin Law, 5.

-Meadow, C.(2016). The history and development of “A” DR (alternative/appropriate dispute resolution)”, Völkerrechtsblog, doi: 10.17176/20180220-230945.

Sourdin, T. (2014). Alternative dispute resolution principles: From negotiation to mediation (4th ed), Thomson Reuters, 179-193.

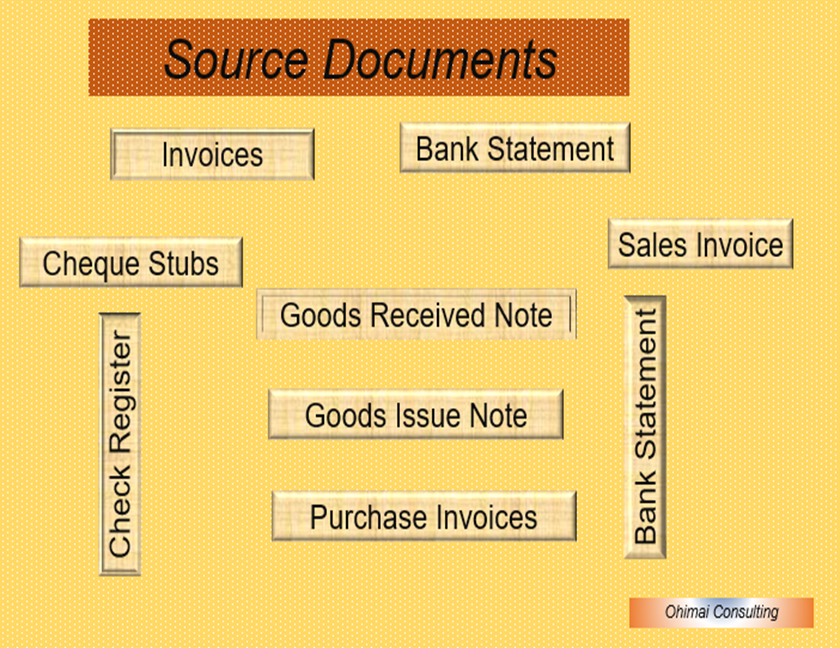

Relevance of Source Documents to organizations cannot be over emphasized. It is important to an accountant and organization in the event of fraud.

Relevance of Source Documents

1. Audit Trail

Audit trail is a set of accounting documents that authenticate the transactions you record in your accounting books. Furthermore, it provides evidence that transaction has occurred. Also, during audit, source documents serve as back up for accounting journals and ledgers. Every business owner is responsible for recording the company’s transactions. Moreover, the relevance of source document to audit trail is such that it must have to include information about what the event was, who created the event, and the day and time the event happened.

2. Full Details of Transactions

It reveals all the basic fact about the transaction such as the amount of the transaction, to whom the transaction was made, the purpose of the transaction. Also, the date of transaction, serial number of the document, name of document such as Local Purchase Order (LPO), receipt, particular of person issuing the document, particular of person authoring the document, name of company/department issuing the document and name of company/department receiving the document.

3. Internal Control System

Internal controls system are the devices, rules, and measures effected by a company. This internal control ensures the integrity of financial and accounting information, uphold accountability, and prevent fraud. Source document is a good internal control mechanism.

4. Assist Accountants

Source documents assist accountants to prepare financial statement which auditor need for investigation. The movement starts from source documents to journalize transactions. In addition, posting is the process of transferring journal entries to the general ledger or subsidiary ledgers, depending on the needs of a company, by account.

5. Reference

In the accounting world, source documents include purchase order, sales invoice, bank statement, and receipts.

Source documents are created any time a business spends or receives money. However, when there is a report of any investigation into a transaction says fraudulent withdrawal from the bank, the bank statement which is one of the source documents will serve as reference point.

6. Correct Errors

Sources document one will be able to verify whether or not an accounting entry is accurate or correct. It is used to correct errors and omission of transactions. Also, situation where staff will deliberately omit or cause error to occurred will be detected with the investigation of the source documents.

7. Reconciliation

Source documents helps to reconcile with the balances in accounts to see if some documents have not been recorded. Also, if some transactions recorded in the accounts do not appear to have any supporting documents. Frequent reconciliation of account will help to reduce fraudulent activities.

Conclusion.

The relevance of source documents to checkmating fraud is such that organization will need to monitor. That will ensure the right thing is done with the available resources.

There are basic assumptions which underline the preparation of financial statements of business enterprise. There are stated below:

Going concern concept: accounting assumes that the business will continue to operate for a long period of time. In other words, it means continuity in business or Continuity Assumption.

The continue preparation of financial statement in accordance with International Financial Reporting Standard (IFRS) is an evidence of going concern. Even the auditor may also carry out investigation see that the going concern is intact.

Example of going concern is prepayment and accrual of expenses. The company accept these expenses because they believe the business will continue to run. If for example any part or section or department or product line is discontinue, it does not means there is no longer a going concern. Going concern is for the entire company.

During Covid19, a lot of companies had financial issues and were unable to pay their obligation. Various government gives those companies a bailout and a guarantee of all payments to creditors. The companies are a going concern despite of its current weak financial position. But if government imposes a restriction on the manufacture of a certain goods and service for the period say 1 year. Then the company will no longer be a going concern since they might not be able to sell any product.

2. Entity concept: This accounting concept separates the business from its owner. Meaning the business is a legal entity. It can sue and be sued. It also means the owners of a business are limited to how much he has invested not his personal resources. So for example, if the owner brings in additional capital into the business, we will treat this as a liability on the balance sheet of the business.Entity concept ensures that each company is tax separately.

Let look at these examples, Mrs. Ese bought a building having 5 office space for $5000 per month. She uses three office for his business and two for personal purpose. In line with business entity concept, only $3,000 (the rent of two offices) is a valid expense of the business

Another example is when owner of a business lends loan to his company. It would be strictly recorded as a liability and that has to be paid back to the owner.

3. Matching Concept:This concept states that the revenue and the expenses of a transaction should be included in the same accounting period. So to determine the income of a period all the revenues and expenses (whether paid or not) must be included. The matching accounting concept follows the realization concept. First, the revenue is recognized and then we match the costs associated with the revenue. So costs are matched with revenue, the reverse would be an incorrect system.

4. Dual concepts: this says that there are two aspects of accounting. It is represented by the assets of the business and liabilities (i.e. claims against it). Assets =liabilities + capital. So for example. Say the business buys an asset worth N10, 000. So now the Fixed Assets of the company will increase by N10, 000. But at the same time, the bank or cash balance will reduce by N10, 000 and so the transaction will have a dual effect in accounting. And also the Balance Sheet will stay balanced.

5. Realization concepts: in accounting, profit should not be recognized until the goods are passed to the customer.

6. Money measurement concept: Accounting is only concerned with the facts that can be measured in monetary terms with fair degree of objectivity. Accounting does not record that the firm has a bad or good management team, poor morale among staff. So for example, if the company underwent a major management overhaul this would have no effect on the accounting records. This concept is actually one of the major drawbacks of accounting.

7. Accrual concept: Revenue and cost are usually recorded in accounts when they are earned or incurred rather than when the money is received or paid.

8. Full Disclosure Concept: This concept states that all relevant information will be disclosed in the accounting statements. A lot of external users depend on these financial statements for their information to make investing decisions. So no information/transactions etc of relevance to any one of them will be omitted from these statements for the benefit of the company.

9. Cost Concept: This accounting concept states that all assets of the firm are entered into the books of account at their purchase price (cost of acquisition + transport + installation etc). In the subsequent years to, the price remains the same (minus depreciation charged). The market price of the asset is not taken into consideration.

10. Accounting Period Concept:Every organization, according to its needs, chooses a specific period of time to complete an accounting cycle. Generally, the time chosen is a year we call the accounting year. The time period is mentioned in the financial statements.

11. Substance over form: usually transactions are recorded and accounted for by their commercial realities rather than their legal form. Substance over form is an accounting concept which means that the economic substance of transactions and events must be recorded in the financial statements rather than just their legal form in order to present a true and fair view of the affairs of the entity.

12. Faithful representation: For financial report to be useful, the financial information must not only represent relevant phenomena but must faithfully represent the phenomena that it purports to represent.

13. Timeliness: It means having information available to decision makers in time to be capable of influencing their decisions. The older the information the less important it become.

14. Relevance: Relevant information is capable of making a difference in the decisions made by users.

15. Comparability: The information about a firm is more useful if it can be compared with similar information about other enterprise and with similar information about the same enterprise for another period or date.