The benefits of ICAN certificate to all area of our lives are enormous. ICAN, whose membership comprises of accountants, auditors, and accounting technicians. It was established in 1965 by Act of Parliament No. 15 of 1st September 1965 (the ICAN Act) (icanig.org). Since then, it has improved the lives of its members and the nation in general.

Being a member of ICAN make you become a professional in accountancy. Opportunities will be available to you when you become a full member of ICAN. A lot of information will be available to you to create wealth.

In the public sector, apart from increase morale and a sense of achievement, there are other things to enjoy. This report looked at two things that are considered benefits of ICAN certificate. If you are a qualified member of ICAN before you got employment cadre of the Federal Government of Nigeria, these are your benefits.

Entry-level with ICAN certificate

This means the moment you are qualified as a chartered accountant before gaining employment in the public sector, you have a chance to start in Grade Level 10.

ICAN members with certificate will still be considered for employment in the public sector in line with the provision of the existing scheme of service even without them having a first degree.

It is only ICAN and other related qualifications prescribed in the scheme of service considered for civil service appointment without a first degree.

The entry point for every ICAN member is GL 10.

Advancement of ICAN qualified members

Advancement means moving an officer up from one rank to a higher one within his class or cadre. It is not the same with conversion.

An officer who is on a Grade Level 08 advanced to Grade Level 10. It is a way, a type of promotion. The officer must possess the qualification, which the scheme of service stipulated for holders of that office.

In the case of ICAN members’ already in service, whose grade is below Grade Level 10 and who obtain ICAN qualification is qualified to be advanced to Grade level 10.

The moment that employee sits for ICAN exams and qualify. He or she is qualified to notify his or her employer of the new qualification for considerations.

Ordinarily, the promotion would have taken a minimum of 6 years if he or she passes the confirmation and promotion exams. The power of the ICAN certificate can make it possible in two years.

Conclusion

Student of accounting in higher institutions and accounting officers in the service of the Federal Government needs to take advantage of this opportunity that is made available. This qualification needs to be presented before attaining grade level 10. I

NOTE:

This post is not a legal advice. You are to carry out due diligent on your own.

Unknowingly, many agricultural programme embarked upon by government, private companies and even individual all help to reduce carbon emission from the atmosphere.

Global Landscapes Forum

Agriculture by-products can cut emission. For example, biomass can be used directly in agriculture as a fertiliser, or it can be used as a source of energy for the power, buildings, industry or transport sectors and also biogas from animal wastes could also be used as an energy source.

A tree can absorb as much as 48 pounds of carbon dioxide per year and can sequester (hide-away or isolate) 1 ton of carbon dioxide by the time it reaches 40 years old. Carbon sequestration is a natural or artificial process by which carbon dioxide is removed from the atmosphere and held in solid or liquid form. CARBON CREDIT AND CARBON TAX: OTHER SOURCES OF REVENUE FOR NIGERIA. |

Wikipedia

Reservoirs is a carbon sink if it retain carbon and keep it from entering Earth’s atmosphere. Deforestation lead to carbon emission into the atmosphere. But when the forest is regrowth that is a form of carbon sequestration, with the forests themselves serving as carbon sinks.

Conclusion

Tree planting is for our benefit. These are some benefit of tree planting to humanity. Trees give off oxygen that we need to breathe. Trees reduce the amount of storm water runoff. Trees reduces erosion and pollution in our waterways and also reduce the effects of flooding. Many species of wildlife depend on trees for habitat. Trees provide food, protection, and homes for many birds and mammals. Tree remove carbon emission from the air. de food, protection, and homes for many birds and mammals.

Carbon credit and carbon tax: Other sources of Revenue for Nigeria

Emissions that aren’t with the production of industrial and consumer goods should be taxed.

A carbon tax is one of the tool government used to check climate change. The two is emission and offset trading system (that encourage carbon credit). Government intervention is a tool to fight climate change. The government uses two methods as discussed below to put climate change in a check (Carbon Emission Accounting and Economic Growth in Nigeria).

1). QUANTITY-BASED

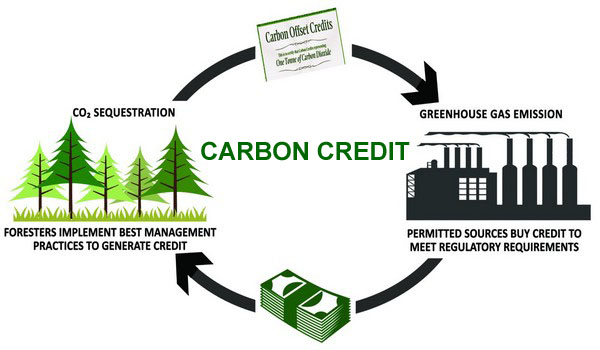

The Quantity-based measures depend on regulations to check climate change. The quantity-based measures are called emission and offset trading systems or cap and trade. Quantity-based measures are the most common interventions by any government.

In quantity-based believes that each country/company is assigned a fixed amount of carbon emissions which is a cap/limit by the government, measured in carbon credits. When a company emits less than permitted emissions, it can sell the rest to companies that are unable to reduce their emissions level. This method can earn companies that are meeting up with a cap limit by the government, huge revenue.

Government through the agency(NESREA ) reduces the emission caps each year to set a new pollution target and allocate new emission limits to industries. This way, companies are forced to seek other ways to meet their energy needs, thereby embracing green technology. The carbon credits of a company are rights for emission. Each unit gives the right to emit one metric tonne of CO2.

A carbon credit is a permit that allows the company that holds it to emit a certain amount of carbon dioxide or other greenhouse gases. On the 9th June 2021, at the 2021 Nigeria International Petroleum Summit (NIPS) held in Abuja, it was reported that Nigeria recorded its first proceed from carbon from the partnership of Nigerian National Petroleum Corporation and TotalEnergies.

2). PRICE-BASED

Price-based talk about carbon taxes. A carbon tax is a levy on the carbon content of fuels used. Carbon tax a tax paid on the emission of carbon (CO2) into the atmosphere by any organisation. It is a form of carbon pricing that offers a double dividend. By double dividend, it means revenue generation and behavioural change. The double dividend in the sense that as government generate revenue at the same time bring about behavioural change among the polluters.

Carbon is present in every hydrocarbon fuel (coal, petroleum and natural gas) and is released as carbon dioxide (CO2) when they are burnt. Hydrocarbons are released into the air when volatile fuels evaporate from storage tanks. They are also found in the exhaust of motor vehicles when fuel is burnt incompletely. If not control they can cause cancer and lead to the formation of photochemical smog (otherwise called Soot “black soot” as we currently experienced around Port Harcourt, Nigeria and its environs). In contrast, non-combustion energy sources—wind, sunlight, hydropower, and nuclear—do not convert hydrocarbons to CO2. CO2 is a heat-trapping “greenhouse” gas.

The reason carbon tax is overdue in Nigeria is that it will internalize the externality. What this means is that the final price of the good should include the social cost and not just the private cost. It is similar to the ‘polluter pays principle.

The ‘polluter pays principle is the commonly accepted practise that those who produce pollution should bear the costs of managing it to prevent damage to human health or the environment. The polluter-pays principle was incorporated into international law at the 1992 Rio Summit.

A number of countries have implemented carbon taxes or energy taxes that are related to carbon content but Nigeria is still lacking behind. South Africa for example has developed a robust carbon tax system since 2016. The aim is to reduce greenhouse gas (GHG) emissions from key sectors such as mining, transportation and agriculture and to achieve sustainable development. Sadly, other African countries have failed in this regard. If a carbon tax is to be successful in your country, then one must embrace the efficiency that follows.

Some countries that have implemented carbon tax or energy tax are:

South Africa;

Columbia;

Denmark;

Japan;

Mexico;

Finland;

Germany;

Chile;

France;

Canada;

Iceland;

Costa Rica;

Ireland;

Italy;

The Netherland;

Norway;

Slovenia;

Sweden;

Switzerland, and the

United Kingdom etc

DIFFERENCE BETWEEN CARBON TAX AND CARBON CREDIT (CAP & TRADE SYSTEM)

Carbon tax does not guarantee decreased carbon emissions but focuses on revenue generation, while carbon credit (cap and trade) system helps to sets emission limits.

An action word is one that does something. Action verb for management skill or leadership skills that will be appropriate in your resume. Once any of these list is introduced into your resume it will signifies that you have management skills or leadership skills.

Adverbs described verb. Be honest, accurate and selective with the numbers of adverbs in your resume. Here is the top 100 list adverbs keyword below of the most frequently used adverbs in resume.