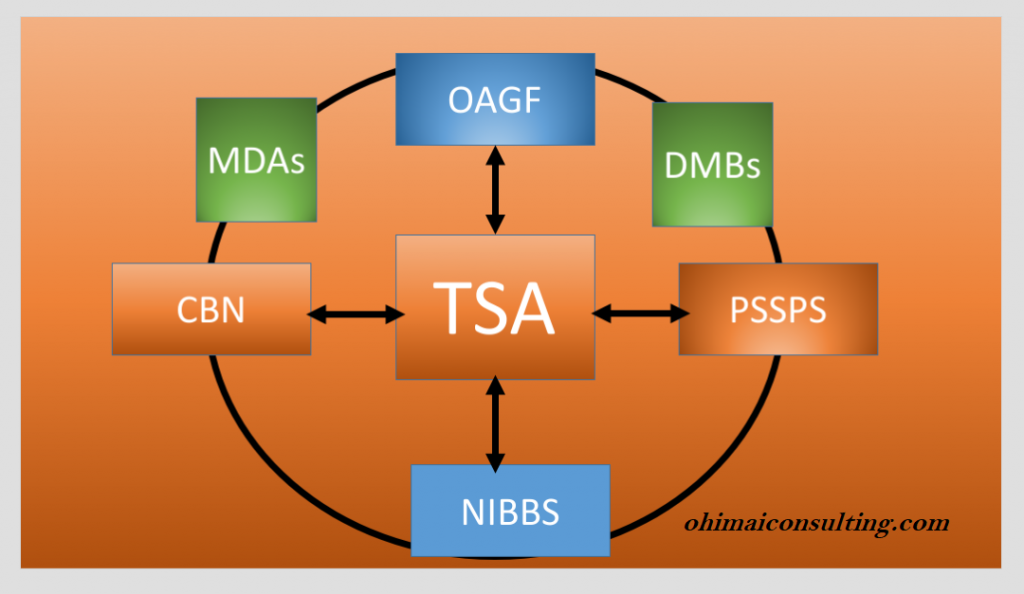

Treasury Single Account (TSA): This is defined as a unified structure of government bank accounts for MDA’s. TSA is a single account in the custody of the Central Bank of Nigeria (CBN). TSA is a bank account or a set of linked accounts through which the government transacts all its receipts and payments. Treasury Single Account is a concluding phase of the E-collection scheme. The Federal Government of Nigeria commenced the implementation of e-collection component of TSA in January 2015. The first Treasury Circular on e-Collection was issued on the 19th of March 2015.

E-collection automates and streamline revenues and other monies payable to MDAs as well as other Institutions and Parastatal directly into the Consolidated Revenue Fund (CRF) or designated accounts of each MDA at CBN using the CBN Payment Gateway.

This is one of the good initiatives of federal government of Nigeria that has help to bring about transparency and accountability. This initiative has given Nigeria government control over the management of fund in the hand of Ministries, Department and Agencies (MDAs).

OBJECTIVES OF FGN E-COLLECTION

Ensure total compliance with the relevant provisions of the 1999 Constitution of the Federal Republic of Nigeria (FRN) (Section 162 & 80).

Collect and remit all revenues due to the Federation Account and Federal Government Consolidated Revenue Fund.

Block all leakages in government revenue generation, collection and remittance

Enthrone a new regime of transparency and accountability in the management of government receipts.

Improve on availability of funds for development programs and projects.

Align with the CBN Cashless policy.

Ease the burden of revenue payers.

BENEFITS OF TSA

Government have oversight of all revenue and other monies collected by MDAs

2. Increase Government receipt by blocking any form of leakages

3. Makes it easier for Nigerians to pay government through introduction of electronic channels like Cards, Internet Banking and POS.

4. Payment is received promptly, and service can be rendered to the payer

5. Ensure availability of funds for the execution of government policies, programmes and projects. Control aggregate cash flows within fiscal and monetary limits

6. Improve management of domestic borrowing programme

7. Investment of idle funds

8. Improves transparency and accountability of all FGN receipts

9. Consolidated view of government cash position and status

TREASURY SINGLE ACCOUNT STAKEHOLDERS

Ministries, Departments & Agencies (MDAs);

2. Deposit Money Banks (DMBs);

3. Central Bank of Nigeria (CBN);

4. Service Providers.

THE ROLE OF CBN IN TSA

Provide payment gateway platform

2. Development of overall e-collection and e-payment policies for the nation

3. Interfacing with Deposit Money Banks (DMBs) and monitoring them

4. Creation and maintenance of bank accounts including CRF/TSA, FAAC and TSA Sub Accounts

THE ROLE OF DEPOSIT MONEY BANKS (DMB)

Ensures that:

Their duties under the subsisting Payment Gateway MOU are effectively discharged

2. Customers making payment to government are given prompt service

3. All collections in favour of government are promptly remitted

4. Operational and other relevant issues are logged with appropriate authorities (OAGF, CBN and REMITA) without delay

The ROLE OF MDAs

Ensure that their revenue targets are met

2. Provide their payers with details of payment including amount and nature of payment

3. Guide payers on e-collection processes including how to pay at the bank or through other channels of the CBN Payment Gateway (Remita).

4. Where applicable, ensure that appropriate services are rendered upon confirmation of payment

THE ROLE OF OFFICE OF THE ACCOUNTANT-GENERAL OF THE FEDERATION (OAGF)

Ensure effective implementation of e-collection

2. Development of operational guidelines

3. Proper monitoring of the collection gateway

4. Prompt reconciliation of all collections

5. Support MDAs, banks and payers for smooth operation of e-collection

6. Regular monitoring of all collections to ensure that they are promptly remitted and accounted for

7. Issuance as well as continuous review and update of the e-Collection guidelines and processes

8. Abide by the provisions of the Memorandum of Understanding (MOU) with CBN, Service Provider and Banks

THE ROLE OF SERVICE PROVIDER ie Remitta, Interswtich etc

Work with CBN, OAGF and other stakeholders to articulate system requirements

2. Provide a robust, stable and effective integrated processing platform

3. Ensure the optimal availability of all relevant systems and platforms

4. Provide effective and efficient support to users of the platform

5. Provide users with relevant reports

6. Training of users on the use of the payment gateway.

E-PAYMENT

This is an electronic system of payment for all of government funds through the banks either commercial banks or CBN. The Federal Government of Nigeria commenced the implementation of Treasury Single Account (TSA) in April 2012, with the e-Payment component. E-payment covers the following transactions:

All payments to

contracts and consultants.

2. service providers e.g. PHCN.

3. payment to staff.

4. payment to other government agencies e.g. National Health Insurance Scheme (NHIS), Federal Inland Revenue Service (FIRS), National Housing Fund (NHF).

Issuance as well as continuous review and update of the e-Collection guidelines and processes

BENEFITS OF E-PAYMENT

These are some of the E-Payment benefits:

It eliminates the:

1. Unacceptable delay in payments

2. The uses of cheques in payment of all transactions within the Federation Government

3. Interaction between the contractor and government official in the payment of FG contracts

Some forensic accountants choose to specialise in Alternative Dispute Resolution (ADR) due to their familiarity with both finances and the legal system. Business litigation can be a very expensive and costly. Generally, opposing attorneys will fight vigorously for their clients. When forensic accountants are engaged as EXPERT WITNESSES in business litigation, such fighting can drive up the cost of the expert witnesses and drive down the understanding of the forensic accountant’s work and, therefore, the client’s satisfaction with the forensic accountant.

In a typical business litigation scenario, the opposing attorneys may fight against providing information which the forensic accountant has requested in order to calculate damages or to perform a business valuation. Depending on the amount of rancor between the parties and level of antagonistic determination between the attorneys.

There are times he may have to perform the damage calculation or business valuation without all the relevant information he believes is necessary. In the absence of such information, the forensic accountant may have to make reasonable assumptions regarding the missing information. If there are differing assumptions by each side’s expert witness, significant differences in damage calculation or business valuation amounts may result.

In such situations, the parties often may expend significant time and incur significant costs in using these forensic accounting experts. Especially when there are significant differences of opinion between the two expert witnesses, the experts’ fees and attorney fees can be even higher. Both parties also may come away with confusion and misunderstanding regarding how the relevant damage amount or business’s value was determined.

This is because they may only speak with the expert retained by their attorney and must rely upon the deposition and/or courtroom testimony of the opposing expert without being able to ask their own questions. The use of alternate dispute resolution – such as mediation, arbitration, and negotiation – not only can reduce the cost of traditional business litigation, but also can help eliminate the uncertainty that comes from leaving the resolution of the dispute up to the Courts (judge or jury).

Examples of disputes that are prime candidates for alternate dispute resolution includes: • Business contract disputes • Shareholder/partner disputes • Employee termination disputes • Insurance claims • Royalty payment disputes • Patent/trademark disputes • Business merger and acquisition • Local disputes, • Global disputes,

How the role of the forensic accounting expert differ in Alternate Dispute Resolution (ADR) • First, the forensic accounting expert can be jointly retained by both parties as opposed to by just one party in traditional business litigation.

• Next, because of the joint retention of the forensic accounting expert, both parties are more cooperative and better able to share all the necessary information needed by the forensic accounting expert. Thus, there is also usually less of a need to make assumptions.

• Finally, the expert witness report can be openly reviewed with both parties. Because this is a joint retention, the forensic accounting expert can be more open and informative with both parties and stand ready to fully answer either party’s questions. This helps to eliminate confusion and lack of understanding regarding the damage calculation or business valuation and the forensic accounting expert’s process.

• Additionally, the cost for the forensic accounting expert will be less, because only one expert is retained instead of two, and because the cost of depositions and/or courtroom testimony can be eliminated.

The Role of the Forensic Accountant In Mediation A forensic accountant has a number of possible roles to play, which are discussed below.

Expert Accountant acting as a Mediator. Accountants may play a role in a dispute by acting as a mediator. For example, disputes involving business valuations, application of technical accounting standards or which require business acumen and experience in a particular industry or sector may benefit from having a mediator with the requisite expertise in these areas.

The Forensic Accountant’s role in calculating damages and attending the Mediation. In complex commercial disputes requiring an expert opinion on the quantum of damages, for example in a case whereby one party may have suffered a loss of profits following a breach of contract by another party, a forensic accountant may be retained as an independent expert to provide an independent assessment of the amount in dispute. In such a case the forensic accountant may be requested to prepare an expert report, attend a meeting of experts with an opposing expert, or advise their client on a range of their potential losses depending on a number of factors or assumptions. In mediation, the forensic accountant can provide a similar role, assisting a mediator in dealing with and understanding complex financial issues.

Forensic accountant role to serve as appointed receiver or monitor

Forensic accountant role as Consulting or testifying expert

Forensic accountant role as impartial neutral with specialized expertise

Forensic accountant role as Advisor to party during mediation

Conclusion The philosophy behind Alternative Dispute Resolution is to ensure that parties involve resolve their dispute without anyone of them feel aggrieved. ADR is a good mechanism to resolve disputes among individual and organisation both local and international level. The presenter believes and suggests to us that all avenues available within ADR be explored fully before approaching the court. Even now that so many cases are queuing in the court without definite date of conclusion, is an issue that need immediate action by the government.

Dispute resolution is the process of resolving a dispute between parties. Dispute resolution is also often referred to as “conflict resolution.” There are a number of processes that can be used to resolve conflicts, claims, and disputes.

Therefore, ADR is the procedure for settling disputes without litigation, such as arbitration, mediation, or negotiation. It is also called external dispute resolution (EDR).

ADR procedures are usually less costly and more expeditious. They are increasingly being utilized in disputes that would otherwise result in litigation, including high-profile labour disputes, divorce actions, and personal injury claims.

One of the primary reasons parties may prefer ADR proceedings is that, unlike adversarial litigation, ADR procedures are often collaborative and allow the parties to understand each other’s positions. ADR also allows the parties to come up with more creative solutions that a court may not be legally allowed to impose.

So the philosophy behind ADR is that it offers the parties an opportunity to avoid risks and reduces the likelihood of an unfavorable outcome. It gives the parties in the dispute the opportunity to consider the risks involved in litigation.

Dispute Resolution Processes

Generally, however, most dispute resolution processes are classified as facilitative, advisory or determinative or as ‘mixed’ or ‘blended’, and this article focuses on the more facilitative forms:

(a) Facilitative processes involve a third party, usually with no advisory or determinative role, providing assistance in managing the process of dispute resolution. These processes include mediation and facilitation.

(b) Advisoryprocesses involve a third party who investigates the dispute and provides advice on the facts and possible outcomes. These procedures include investigation, case appraisal and dispute counselling.

(c) Determinative processes involve a third party investigating the dispute, which may include a formal hearing, and the making of a determination that is potentially enforceable. These processes include adjudication and arbitration and may be binding or non-binding.

While there are many reasons why facilitative processes have become more popular in recent years, one critical factor relates to the location of ADR services. Where ADR takes place within the courts or in a court-connected framework, such processes may be more likely to be advisory and be the subject of legal negotiation patterns. Arguably, one reason why facilitative mediation has grown so quickly in Australia is because it is often located outside the court system. While in Australia there has been substantial growth in facilitative ADR both within and outside the court system, in many disputes ADR must be used before court proceedings can be commenced. For example n some cases, court proceedings cannot be filed until a certificate has been lodged indicating that the parties have attended a mediation or in other situations parties must have made a ‘genuine effort’ or made ‘reasonable attempts’ to resolve the dispute before commencing proceedings. Within Australia, the most striking example of an extensive mandatory prelitigation ADR system exists in the family relationships area, and most disputants can expect to attend some form of mandatory ADR before being able to commence proceedings in a court.

.

Modes of Alternative Dispute Resolution (ADR)

Arbitration – This is a method involving one or more neutral third parties who are usually agreed upon by the disputing parties and their decision is final. The decision arrived at by arbitrator(s) is called an award and same is enforceable like a court judgment. The agreement to arbitrate must be in writing, signed, and the agreement is irrevocable except by agreement of the parties or by leave of court (Aduaka & Onnome, 2018). A process similar to an informal trial where an impartial third party hears each side of a dispute and issues a decision; the parties may agree to have the decision be binding or non-binding.

Mediation – This is essentially a non-binding dispute resolution mechanism involving a neutral and impartial third party who tries to help the disputing parties reach a mutually agreeable solution. The third party here is impartial, does not take decisions for the parties rather he helps them in identifying the issues and interests that need to be solved (Aduaka & Onnome, 2018). A collaborative process where a mediator works with the parties to come to a mutually agreeable solution. mediation a form of negotiation with a third-party catalyst who helps the conflicting parties negotiate when they cannot do so by themselves. Mediation is usually non-binding (Khan & Karim, 2017).

Conciliation-The process of conciliation is basically that of mediation. The only difference is that the neutral third party is usually an expert in the field or area of dispute in which he has being called upon to conciliate (Aduaka & Onnome , 2018). This is an ADR process where an independent third party, the conciliator, helps people in a dispute to identify the disputed issues, develop options, consider alternatives and try to reach an agreement. A conciliator may have professional expertise in the subject matter in dispute and will generally provide advice about the issues and options for resolution. However, a conciliator will not make a judgment or decision about the dispute. Conciliation may be voluntary, court ordered or required as part of a contract. It is often part of a court or government agency process.

Negotiation- Negotiation is a process whereby parties discuss and agree to terms or reach certain agreement without the aid or intervention of a third party. Negotiation basically involves some form of „give and take‟ from either parties or some form of compromise by the disputing parties. It is important to note that the law does not prohibit parties to a dispute from engaging in negotiation for the purpose of settling their dispute (Aduaka & Onnome , 2018). This form of ADR is often overlooked because of how obvious it is. In negotiation, there is no impartial third party to assist the parties in their negotiation, so the parties work together to come to a compromise.

Collaborative Law- This is a form of ADR that has grown in popularity, especially in respect of family disputes. In this process, all participants may decide to use a ‘collaborative’ process model whereby lawyers and all experts are trained in interest-based negotiation and are focused on the negotiation process with two-hour meetings and guidelines for gathering and exchanging information (collaborative participation agreements normally require the withdrawal of lawyers and others if the negotiation does not result in an agreed outcome, which means that they cannot be involved in any subsequent litigation). This is common in North America.

The mathematical theory of games was invented by John von Neumann and Oskar Morgenstern (1944). ‘Game theory is the science of rational decision making in interactive situations’ (Dixit & Skeath, 1999). ‘Game theory can be defined as the study of mathematical models of conflict and cooperation between intelligent rational-decision makers.’(Myerson,1991).

Both these definitions focus on the interactive component between the parties. At the heart there are the twin issues of conflict and cooperation. There is the assumption that these decision makers are rational and have specific objectives in mind which in a dispute is to reach a settlement.

Game theory, a mathematical model used in a variety of dispute contexts starts with the premise that the participants, while not knowing fully the position of the other party, are rational and want to achieve the best possible outcomes.

Levine (2019) stated despite the intensity of a dispute, both sides ultimately want to achieve the best possible outcome. Each party has to assume that the other party is rational even though he may not know exactly what the other party wants.

It is in this situation that the third party negotiator’s role becomes increasingly important to help move the parties along in the process of information exchange until they come closer to a common understanding as to what the other person wants.

Game theory provides a new language to think of human behaviour and of parties who are in conflict. Negotiation can be used in the family setting to alter the expectations and preferences of the parties. In game theory, one of the dominant models which has been used to explain the behaviour of individuals is the Nash Equilibrium. In game theory, the Nash equilibrium, named after the mathematician

John Forbes Nash Jr. is a proposed solution of a non-cooperative game involving two or more players in which each player is assumed to know the equilibrium strategies of the other players, and no player has anything to gain by changing only their own strategy (Osborne & Rubinstein, 1994).

The usefulness of the Nash Equilibrium is that it comes to a point where the parties realize that they will need to settle in order to maximize their chance of a positive outcome. According to Levine (2019), the use of game theory is not meant to assume that within it is the solution to real life issues. What it offers is simply a model to understanding conflict situations and analyzing how parties can make decisions that result in positive outcomes.

Conclusion

Game theory shows win-win situation. It can apply in the business environment, to ensure every parties have the reason to smile.

References

Dixit, & Skeath. (1999). Games of strategy. 3

Levine, D. K.(2019). Game theory and the law.(alternative dispute resolution). Retrived on the 25th July, 2019 from the Kmnp Law Website www.Kmnplaw.Com.

Myerson, R. B. (1991). Game theory: Analysis of conflict. Harvard University Press, (1), vii–xi

Osborne, M. J., & Rubinstein, A. (1994). A course in game theory. Cambridge, MA: MIT.,14.

ADR meaning “alternative” to formal court hearings, trials and formal legal proceedings. In fact, many forms of dispute resolution are thousands of years old, dating from Confucian principles of promoting harmony and community, rather than individual, “justice,” in China and then later other Asian countries, or African community dispute resolution processes called “moots” (or in some countries Ubuntuor gacaca), which are mediation like processes in which community elders listen to narratives of the dispute from the parties and either help negotiate a solution with the parties, or, more like arbitration, decide or command some remedy, with the goal of preserving community peace. The goals of such older forms of dispute resolution are to prevent further conflict and escalation of the dispute beyond the parties, to restore the community to peaceful existence.

In the West (Continental Europe and in England), the middle ages saw the movement from “trial by ordeal” (putting disputing parties on a horse to joust, or dropping them into a fire or body of water to see if God would “protect” them and declare the innocent or non-wrongdoer) to trial by evidence. The development of formal rules of evidence was designed to use rational forms of proof and judgement by “peers” (juries) about what had happened to cause the dispute. “Modern” justice meant that judges or juries declared winners and losers (in both civil and criminal cases) so that the guilty would be punished or pay damages and the innocent would be vindicated by using the same rules of procedure and substantive rules of law to everyone (“equal justice under law”).

In the late 20th century this more modern way of achieving “individual” justice caused many court systems to become very crowded (in countries like the US and Italy it could take as much as 5-10 years to get a hearing), and once there, the court and formal trial process became quite expensive, requiring the hiring of lawyers and other professionals (experts) and the paying of high fees.

So in the 1970s two different groups of reformers proposed different solutions to the court delay problem. Some American judges and scholars proposed “alternatives” to court (mediation, arbitration, negotiation, mandatory settlement conference,) to encourage parties to settle their differences quicker and cheaper with out-of-court processes. This was called the “Multi-Door Courthouse,” an idea that people would choose a process and reduce their costs and time in resolving disputes. The US government actually funded a few local court systems to create such multi-door courthouses and many people (lawyers, psychologists and community leaders and social workers) were trained as mediators .

In the last few decades different forms of ADR have gone global—a new field of transitional justice has developed to provide both punishment and reconciliation in post-apartheid, post-civil-war and other post-conflict zones. So although there is now an International Criminal Court for state violations of human and civil rights and criminal prosecutions, in some settings, a form of ADR has been used to create Truth and Reconciliation Commissions (e.g. South Africa, Bolivia, Argentina, Liberia) which are often hybrid institutions that seek the “truth” about what atrocities have occurred, but also try to use various forms of narrative, apologies, forgiveness ceremonies and rituals to attempt to “heal” the past, so newly constituted countries can move forward.

Ironically, or in a return to earlier history, some countries have used older indigenous processes like community moots (gacaca in Rwanda) to attempt to combine justice of the past with peace for the future. These new forms of institutions are hybrid because they draw on both public international law concepts (international criminal law) and national or indigenous processes.

ADR is now widely used around the world to deal with disputes and conflicts as well as agreement-making and planning. At the international level, negotiation (between and among different countries, states and communities are as old as humankind) and is a process now used by the 200 countries in the world to negotiate treaties (which are state commitments to not engage in war or other bad acts, or to positively collaborate on other activities, like poverty amelioration, environmental protection, anti-discrimination, health, education and cultural cooperation).

Modern international legal activity is often conducted in informal networks of negotiation and new forms of international administrative actions, rather than by formal courts or executive diplomacy. Mediation by international officials is now commonly used to try to resolve interstate conflicts before they escalate to war. Mediation and arbitration are both used in both public law and private, commercial law settings. Arbitration is used on an international level to resolve border and boundary disputes, private commercial cross-border disputes, and now disputes involving private investors in foreign countries.

Formal institutions like the World Trade Organization use arbitral processes and investment arbitration now represents a controversial hybrid, using arbitral processes, but relying on more public law principles and demands for transparency. Most informal dispute processes ultimately rely on the enforcement powers of national courts under international treaties, such as the New York Convention for the Recognition and Enforcement of Foreign Arbitral Awards or the Washington Convention for dispute processes for foreign investment disputes with states.

At the level of everyday disputing, the European Union and some national court systems are now promoting various forms of ADR, such as those described here, to reduce long court delays and to provide consumer and even businesses different ways to resolve their disputes, including the promotion of Online Dispute Resolution (computer platforms for trans border and national consumer disputes or disputes between citizens and states).

The expansion of different forms of dispute resolution has led to interesting issues and policy differences about whether conflicts and disputes belong to the parties, so they can privately choose their form of resolution, or whether conflict resolution should remain a public and transparent state function when the impact or precedent of a conflict resolution might be greater than just on the interested parties. This is were the concept of Game theory is necessary in ADR.

References

Andrew, J. P. (2000). Alternative dispute resolution: skills, science, and the law. Toronto, Ontario: Irwin Law, 5.

-Meadow, C.(2016). The history and development of “A” DR (alternative/appropriate dispute resolution)”, Völkerrechtsblog, doi: 10.17176/20180220-230945.

Sourdin, T. (2014). Alternative dispute resolution principles: From negotiation to mediation (4th ed), Thomson Reuters, 179-193.